Charitable donations can be made not only in the form of cash, but can also be made as in-kind contributions of property. When an in-kind contribution consists of publicly traded shares, mutual funds or bonds, any capital gains realized are eligible for an inclusion rate of zero. This means that a donor can avoid playing tax on capital gains in addition to receiving a tax credit for the fair market value of the securities . This can make the in-kind donation of shares highly beneficial from a tax standpoint compared to making a cash donation of equivalent value.

To qualify for this special treatment, you must donate the qualifying shares, units, or bonds directly to a recognized Canadian charity. The charity should then issue a tax receipt for the fair market value of the securities. If you first sell the securities and then make a cash donation using the proceeds from the sale, you’ll qualify for the tax credit but you won’t qualify for the capital gains exemption.

When you’ve made a qualifying in-kind donation, you’ll need to complete Form T1170 – Capital Gains on Gifts of Certain Capital Property along with your tax return (form T1170 must be included with your return when filing on paper). Provided that no benefit was derived from the donation and the in-kind donation consists of publicly traded shares, mutual funds, bonds or some other forms of property including segregated funds and ecologically sensitive land, you’ll be able to fully exclude any realized capital gain from your income, in addition to claiming a tax credit for the donation.

Although you’re eligible to exclude any gains from qualifying in-kind donations, you can still claim losses in cases where a capital loss occurs. Form T1170 is only used for lowering the exclusion rate on capital gains, but capital losses can still be claimed on Schedule 3 for in-kind donations.

Here’s an example of an in-kind contribution to a charity:

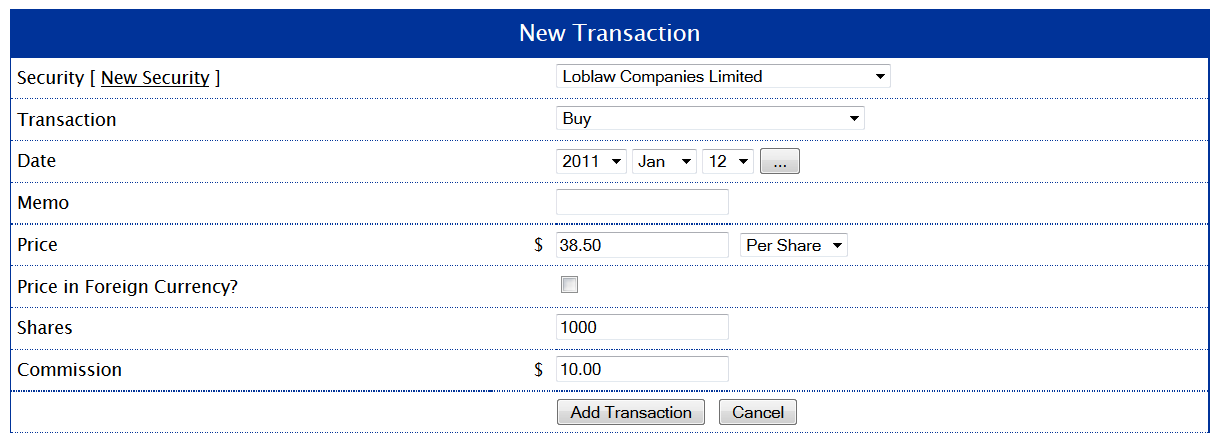

- You purchase 1,000 shares of Loblaw Companies Limited for $38.50/share settling on January 12, 2011 with a $10 commission.

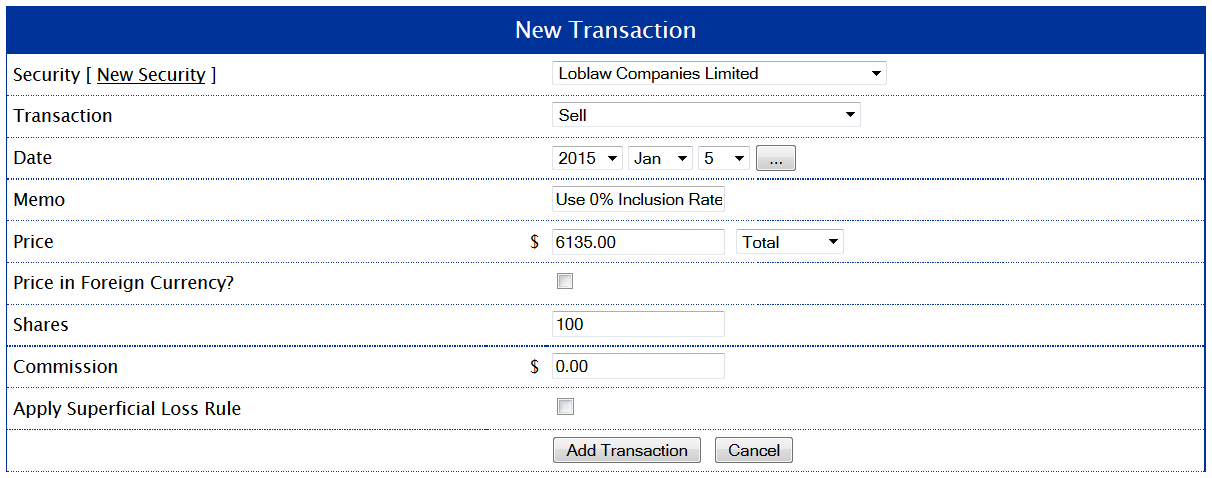

- On January, 5 2015 you donate 100 shares to a registered charity.

- You receive a tax receipt in the amount of $6,135 (for 100 shares at a fair market value of $6,135 on the date of the donation).

AdjustedCostBase.ca is a free tool that can help you calculate capital gains. In particular, it can also be used for calculations in cases where securities are donated in-kind to charities. In this example, the initial purchase would be inputted into AdjustedCostBase.ca as a “Buy” transaction as follows:

The resulting total ACB is calculated to be $38,510 (or $38.51/share):

Next, the donation of the shares is inputted as a “Sell” transaction. Even though the shares have been donated and not sold, a deemed disposition has occurred, hence a “Sell” transaction type should be used. The transaction details would be entered as follows:

The details are inputted as a sale for a total fair market value of $6,135 for 100 shares. A memo was added as a reminder that a 0% inclusion rate should be used for any resulting capital gain. Now, the transactions for Loblaw appear as follows:

Indeed, this results in a capital gain of $2,284. The details of this donation should be entered in Form T1170. The capital gain is excluded, though the transaction is still inputted as a sale for the full fair market value. The disposition should also be reported on Schedule 3, but with the reduced capital gain calculated from Form T1170 carried over into the gain or loss column in Schedule 3 (corresponding to line 13200).

Let’s now compare the advantage received from donating the shares in-kind against the case where 100 shares are sold first and then a cash donation is made of $6,135, equal to the proceeds. Assuming the following:

- A marginal tax rate of 46.41% and a charitable tax credit of 46.41%.

- Charitable tax credits for at least $200 in other donations are already being claimed.

- Total donations do not exceed 75% of net income.

When donating the shares in-kind, total taxes payable would decrease by the following amount as a result of the donation:

Decrease in Taxes Payable = $6,135 x 46.41%

= $2,847.35

On the other hand, when the shares are first sold and then the proceeds are donated, taxes payable would increase due to the capital gain (50% of the capital gain would be included in taxable income). The total decrease in taxes payable resulting from the disposition of the shares and subsequent donation would be as follows:

Decrease in Taxes Payable = ($6,135 x 46.41%) – ($2,284 x 50% x 46.41%)

= $2,847.35 – $530.00

= $2,317.35

Since taxes are payable on the capital gain, the decrease in taxes payable is reduced by the amount of capital gains taxes. Therefore, in this example, donating the shares in-kind results in a benefit of $530 compared to first selling the shares and subsequently making a cash donation. This illustrates the advantage of making in-kind donations of qualifying securities as opposed to cash. This advantage can be particularly big when donating securities in-kind with significant unrealized capital gains.

In addition to the advantage of avoiding capital gains, you can also potentially avoid the hassle of calculating capital gains and adjusted cost base. This is particularly beneficial when you have not kept all your transaction records. When you’ve donated all shares/units that you own in-kind (so that you have no share balance remaining) and have not received any benefit from the donation, the capital gain will be fully excluded no matter what the ACB might be.

Hi,

Let’s say that you have shares of a publicly traded company with a significant capital appreciation that you wish to gift, but that you still believe there is a lot of upside. Can you effectively “reset” your ACB through share gifting and further assuming that you have the money in the first place to donate to charity?

So for example:

I hold one share in Company ABC (TSX:ABC) now worth $1,000 purchased for $100, I have a capital gains of $900

I have $1,000 in cash to donate to charity and I believe that TSX:ABC is going to $2,000 over time

I gift the shares for $1,000, avoid the $900 capital gains, obtain my tax credit, etc.

I take my cash and immediately purchase new shares at $1,000. Now my ACB is $1,000

When the shares are now worth $2,000, I only have a capital gains tax of $1,000 instead of $1,900.

Are there any rules preventing this ?

Thanks!

Jay,

Yes, your ACB of the reacquired shares would be $1,000.

Is there a way on this site to indicate the gain should be excluded when doing yearly gain/loss reports?

David,

Capital gains on donated property still need to be calculated and reported on form T1170. The gain is reportable, but the capital gains inclusion rate will be 0%.

Is there any way to designate the shares as donated so they don’t show up on the capital gains reports?

Jack,

Gains on donated shares still need to be reported on your tax return. The gain will be reported on form T1170.