On July 30, 2020 Brookfield Renewable Partners L.P. (BEP.UN) completed a unit split corporate event resulting in each unitholder of BEP.UN on record as of July 27, 2020 receiving 0.25 shares of Brookfield Renewable Corporation (BEPC) for every unit of BEP.UN. In addition, a cash payment was made in lieu of fractional shares.

https://bep.brookfield.com/press-releases/2020/07-16-2020-220045986

On July 30, 2020, the holders of BEP’s limited partnership units (“BEPunits”) of record as of July 27, 2020 will receive one (1) Share of BEPC for every four (4) BEP units held, or 0.25 Shares for each BEP unit.

Brookfield has provided some details on the tax treatment of this corporate event for Canadian investors on their web site:

https://bep.brookfield.com/bepc/stock-and-dividends/tax-information

I owned units of Brookfield Renewable Partners L.P. prior to the formation of Brookfield Renewable Corporation. As a result of the special distribution from Brookfield Renewable Partners L.P. in 2020, I received class A shares of Brookfield Renewable Corporation. Is this special distribution taxable for Canadian federal income tax purposes?

The special distribution should not be taxable to a Canadian resident shareholder for Canadian income tax purposes provided the adjusted cost base of the Brookfield Renewable Partners L.P. units held by the Canadian resident holder is positive after the special distribution.

In general, this special distribution will reduce the adjusted cost base of your interest in the partnership units of Brookfield Renewable Partners L.P. by an amount equal to the fair market value at the time of the special distribution of the class A shares of Brookfield Renewable Corporation (“BEPC Shares”) you have received. The same fair market value at the time of the special distribution of the BEPC Shares is your adjusted cost basis in your BEPC Shares. The closing price of a share of Brookfield Renewable Corporation on the New York Stock Exchange on July 30, 2020 (the date of the special distribution) was US$40.72. The Bank of Canada daily exchange rate for July 30th, 2020 for USD/CAD was 1.3432.

This information is somewhat misleading because the entire value of the special distribution is not allocated as return of capital. Rather only a portion of the value reduces the ACB because it is offset by an allocation of partnership income. There are in fact taxable components associated with the special distribution.

The ACB of a limited partnership such as BEP.UN needs to be adjusted by reducing the ACB by an amount equal to the distributions received. Normally this would involve cash distributions, but in the case of the special distribution of BEPC shares, the fair market value of the shares received should be used. Next, the ACB should be increased by the net tax allocation corresponding to the distribution. This process should be performed for each distribution.

Brookfield has provided the following spreadsheet as a guide for calculating the ACB for BEP.UN:

On a per share basis the value of the BEPC special distribution is equal to CAD$13.6738. This is based on the value of 0.25 shares for the market price and exchange rate noted above (0.25 x USD$40.72 x CAD$1.3432/USD$).

Based on data posted on the CDS Innovations web site, Brookfield has reported a net return of capital amount of CAD$11.24817/share. The ACB should therefore be reduced by a net value of CAD$11.24817/share after factoring both the value of the special distribution and the net tax allocation associated with this distribution.

This is the case regardless of whether or not cash was received in lieu of fractional shares.

There is also a capital gain value equal to $0.44445 associated with the special distribution. This does not impact ACB but results in an immediate capital gain for the 2020 tax year.

Based on the above, the tax treatment of the BEPC unit split in terms of the impact on ACB is as follows:

- The ACB of BEP.UN will be reduced by CAD$11.24817/share.

- The initial ACB of the BEPC shares is equal to $54.70 per share multiplied by the number of shares received. The total amount of the initial ACB for BEPC excludes any cash received in lieu of fractional shares.

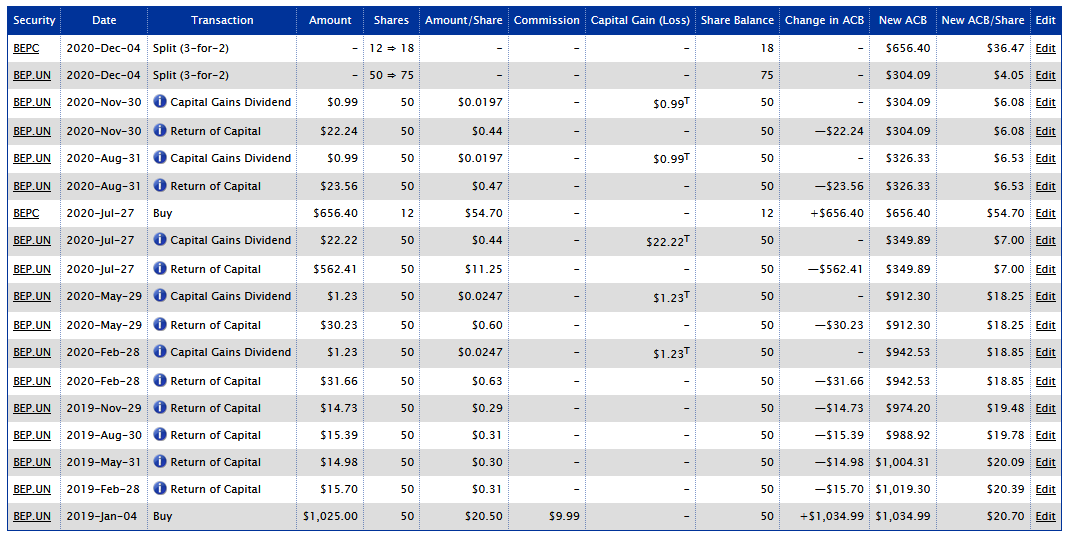

Let’s look at the following example:

- You purchase 50 shares of BEP.UN on January 4, 2019 for $20.50 per share with a commission of $9.99.

- On the record date of July 27, 2020 you receive 1 share of BEPC for every 4 shares of BEP.UN. In this case you would be entitled to 12.5 shares of BEPC.

- Since cash is issued in lieu of fractional shares, you would receive 12 shares of BEPC plus $27.35 in cash (0.5 shares of BEPC x $54.70 per share).

The ACB can be calculated on AdjustedCostBase.ca using the following transactions:

- Buy 50 shares of BEP.UN on January 4, 2019 for $20.50 per share with a commission of $9.99.

- Buy 12 shares of BEPC on July 20, 2020 for $54.70 per share (with no commission) (for a total amount of $656.40).

- Return of Capital for BEP.UN on July 20, 2020 of $11.24817/share.

There are also additional return of capital transactions for 2020 that need to be factored in as a result of the 4 regular cash distributions for BEP.UN for 2020. In particular the values are:

- $0.63327/share for Feb. 28, 2020

- $0.60463/share for May 29, 2020

- $0.47117/share for Aug. 31, 2020

- $0.44483/share for Nov. 30, 2020

In addition there were capital gains allocated for each distribution (including the special distribution) that do not impact ACB but result in immediate capital gains for the 2020 tax year:

- $0.02468/share for Feb. 28, 2020

- $0.02468/share for May 29, 2020

- $0.44445/share for Jul. 27, 2020

- $0.01974/share for Aug. 31, 2020

- $0.01974/share for Nov. 30, 2020

In addition, there would be return of capital and capital gains dividend transactions for 2019 (and any prior years that the units were owned).

There was also a 3-for-2 split for both BEP.UN and BEPC effective with record date Dec. 4, 2020. This should be accounted for via a split transaction.

The ACBs of BEP.UN and BEPC are calculated as follows:

All of the return of capital and capital gains dividend transactions (including the one associated with the special distribution) were imported using the Streamlined Import of Tax Information feature available to AdjustedCostBase.ca Premium subscribers. The initial purchase of the BEPC shares and split transactions for BEP.UN and BEPC must be specified manually.

If the market value of the share received as larger than the ACB of BEP.UN just immediately prior to July 27, 2020 then your ACB will be reduced to $0 and you will incur an immediate capital gain on the residual amount. Your adjusted cost base cannot be negative.

Thank you for your helpful explanation of the special distribution of Brookfield shares. I wasted a lot of time trying to figure out why my investment statement showed a book value of 3060 for 51 shares of BEPC, and see now that this is incorrect. Why, however, does one need to record the capital gains dividend amounts, if they do not affect the ACB? This amount shows up on the T5013 tax slip.

Hans,

You’re correct that capital gains distributions do not impact ACB, but rather result in an immediate capital gain for the year of the distribution. These amounts should appear on your T-slip. You are therefore not obligated to input such transactions on AdjustedCostBase.ca. Doing so, however, will allow you to see your amount of capital gains for the year, including gains resulting from dispositions as well as gains reported on T-slips. Total amounts from these two categories are shown separately on AdjustedCostBase.ca.

Thank you for the helpful write up. You mentioned that data posted CDS Innovations site states that Brookfield reported a net return of capital amount of CAD$11.24817/share. I was looking at the spreadsheet from CDS Innovations and can’t seem to figure out how you came with that number, as the return of capital for July 27, 2020 is listed as 10.69744. I suspect I need to add more values in that column, but I’m not sure which ones.

Additionally, I recall the Brookfield website previously mentioned that the “ACB per share of the BEPC shares is $58.28, as determined by the volume-weighted average price of BEPC on its first five trading days on the Toronto Stock Exchange”, and this is also referenced in a Globe & Mail article (https://www.theglobeandmail.com/investing/markets/inside-the-market/article-your-brookfield-renewable-questions-answered/). Do you know why Brookfield changed this wording?

Kevin,

Brookfield revised the reported value for return of capital for the special distribution. The value reported on March 1, 2021 was $10.69744, but the revised value reported on March 3, 2021 is $11.24817. The revised value should be used. You’re looking in the right place, but the most recent reporting should be used.

You’re correct that Brookfield’s web site used to state a price of $58.28. This was changed to $54.70 (US$40.72 with an exchange rate of CAD$1.3432/US$):

https://bep.brookfield.com/bepc/stock-and-dividends/tax-information

Thank you for your assistance. First-time trader here! I’m experiencing an issue as I try to figure out the ACB for the Livongo (LVGO) and Teladoc (TDOC) merger. I purchased 5 shares of LVGO which resulted in receiving 2 shares of TDOC and a return of capital of $34.95. I then sold the TDOC share in 2020. How do I accurately track and report this transaction?

Great website and I truly appreciate all the posts.

Any chance you could do a post about how to calculate ACB of new tickers BN and BAM split from BAM.A?

Much appreciated!

Dan,

There is some information on the tax treatment of the BAM.A / BAM / BN distribution available here:

https://bam.brookfield.com/sites/brookfield-bam/files/brookfield-corp/overview/tax-qa-canadian-and-us-shareholders-dec2022.pdf

“The distribution should be tax-deferred, and no capital gain or loss will be realized in respect of your Brookfield shares.”

“The tax basis of your Brookfield shares will be allocated to the shares of the Corporation and Manager on the basis that (i) a proportion of the original tax basis equal to the Butterfly Proportion (as defined in the Circular) will be allocated to shares of Manager, and (ii) the balance of the original tax basis will be allocated to shares of the Corporation. The Butterfly Proportion will be 0.12, therefore, the tax basis of your Brookfield shares should be allocated 88% to the Corporation shares, and 12% to the Manager shares that you receive on the distribution.”

This can be inputted into AdjustedCostBase.ca as follows:

1. Sell all shares of BAM.A for a total amount equal to the total ACB of your BAM.A shares immediately before the distribution. This should result in a capital gain of $0.

2. Buy new BN shares for a total amount equal to 88% of the total ACB of your BAM.A shares immediately before the distribution.

3. Buy new BAM shares for a total amount equal to 12% of the total ACB of your BAM.A shares immediately before the distribution.

Referring to the comment above, I assume in #3 you mean 12% to BAM shares?

Also, does the remaining cash distribution (if your BAM.A holding before the spinoff was not divisibile by 4) have any impact on ACB? Should I book that as a distribution / dividend anyhow?

Thanks very much for your help!

Henry,

Thank you, the mistake has been corrected.

For cash received in lieu of fractional shares, the CRA’s administrative practices allow you to reduce the ACB of the shares received by the cash received in lieu of fractional shares, provided that amount is less than $200:

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/it115r2/archived-fractional-interest-shares.html

Therefore you can add a Return of Capital transaction for the new BAM shares (immediately following the Buy) for a total amount equal to the cash received in lieu of fractional shares.