Canadian investors holding specified foreign property with an aggregate adjusted cost base (ACB) of more than CAD$100,000 at any point during a tax year are required to complete Form T1135 (Foreign Income Verification Statement). The T1135 is filed along with your personal (T1) or corporate (T2) tax return.

The CAD$100,000 threshold is based on the maximum total ACB of all specified foreign property during the tax year. This is a Canadian dollar amount (ACB must always be calculated in Canadian dollars). It is not based on the fair market value of the foreign property. It is based on the maximum total ACB throughout the tax year, and therefore you may be required to file Form T1135 even if your ACB at the end of the tax year is below the threshold. The CRA allows you to use either the maximum month-end total ACB of all specified foreign property, or the maximum total ACB at any point of the year.

Specified foreign property includes the following:

- funds or intangible property (patents, copyrights, etc.) situated, deposited or held outside Canada

- tangible property situated outside of Canada;

a share of the capital stock of a non-resident corporation held by the taxpayer or by an agent on behalf of the taxpayer - an interest in a non-resident trust that was acquired for consideration, other than an interest in a non-resident trust that is a foreign affiliate for the purposes of section 233.4 of the Act

- shares of corporations resident in Canada held by you or for you outside Canada;

an interest in a partnership that holds a specified foreign property unless the partnership is required to file Form T1135 - an interest in, or right with respect to, an entity that is a non-resident

- a property that is convertible into, exchangeable for, or confers a right to acquire a property that is specified foreign property

- a debt owed by a non-resident, including government and corporate bonds, debentures, mortgages, and notes receivable

- an interest in a foreign insurance policy

- precious metals, gold certificates, and futures contracts held outside Canada

Common examples of specified foreign property include shares of US corporations (e.g., Microsoft or Berkshire Hathaway) and US-based ETFs and funds (e.g., SPY or VTI).

Canadian ETFs and mutual funds holding foreign property are not considered specified foreign property. Foreign property held in an RRSP or TFSA (or another registered account) or personal use property such as a vacation home are also not considered to be specified foreign property.

The penalties for failing to file Form T1135 can be steep, starting at $25 per day and escalating up to thousands of dollars.

Investors with specified foreign property with a maximum cost greater than CAD$100,000 but below CAD$250,000 have the option of using either the simplified reporting method (Part A) or the detailed reporting method (Part B). Investors with specified foreign property with a maximum cost greater than or equal to CAD$250,000 are required to complete the detailed reporting method (Part B).

| Range of Maximum ACB | Form T1135 Required? | Reporting Requirements |

| CAD$0 – CAD$100,000 | No | N/A |

| CAD$100,000 – CAD$250,000 | Yes | Complete either Part A or Part B |

| More than CAD$250,000 | Yes | Complete Part B |

Part A – Simplified Reporting Method

The simplified reporting method requires only the following details to be provided:

- The types of specified foreign property held during the tax year

- The country codes of the top three countries based on maximum cost

- Gross income from all specified foreign property

- Capital gains (losses) for dispositions of specified foreign property

No details on individual properties need to be provided.

Part B – Detailed Reporting Method

The detailed reporting method generally requires separate reporting for each property. The specific data points required depend on the type of property. A few of the common examples are detailed below.

Category 1: Funds held outside Canada

- Country code

- Maximum funds held during the year

- Funds held at year-end

- Gross income

Please note that foreign currency held in a Canadian financial institution does not need to be included for T1135 reporting purposes.

Category 2: Shares of non-resident corporations:

- Country code

- Maximum cost amount during the year

- Cost amount at year-end

- Gross income

- Gain (loss on disposition)

Category 7: Property held in an account with a Canadian registered securities dealer or a Canadian trust company:

- Country code

- Maximum fair market value during the year

- Fair market at year-end

- Gross income

- Gain (loss) on disposition

Property held at a Canadian registered securities dealer (e.g., a Canadian brokerage) can either be reported in aggregate in Category 7, or individually in the other categories. If reporting property in Category 7, it should be reported in aggregate on a per-country and per-security dealer basis. This method requires reporting of maximum fair market value (rather than maximum ACB) during the year and can be based on the maximum month-end fair market value.

Form T1135 Assistant on AdjustedCostBase.ca

This feature is only available to AdjustedCostBase.ca Premium subscribers. The cost of the enhanced service is $49/year. The basic features of AdjustedCostBase.ca remain completely free for Canadian investors.

AdjustedCostBase.ca provides a tool to help with determining your reporting requirements for Form T1135. The tool also generates much of the required data for completing the form. Accurately computing the maximum ACB of your specified foreign property throughout a tax year can be a headache, particularly if you own many foreign properties that were bought and sold throughout the year. Our tool can help to greatly simplify this process.

In order to use this tool effectively, you’ll need to ensure you’ve marked your applicable securities as “Specified Foreign Property.”

Correctly marking securities as “Specified Foreign Property” is essential for ensuring the accurate calculation of your maximum total ACB throughout the tax year. If you’ve already added securities corresponding to specified foreign property then you can edit these securities in order to set this flag.

The Form T1135 Assistant can be accessed via the “Tools” menu.

In addition to specifying the tax year end date, you can optionally enable the option to “Calculate Maximum ACB Using Month-End Values.” With this option, the maximum ACB values (the aggregate total as well as per-security totals) are calculated based on month-end values, rather than using the maximum day-end values. In some instances the enablement of this rule can drastically impact the calculated maximum ACB. The CRA permits either method to be used.

The generated report instantly provides you with the maximum total cost for a given tax year, and indicates your T1135 filing requirements (whether or not you’re required to complete Form T1135, and if so, whether Part B is required). The reported filing requirement is based solely on the transactions you’ve inputted into AdjustedCostBase.ca. If you own specified foreign property that hasn’t been inputted into AdjustedCostBase.ca, and it places you above either the $100,000 or $250,000 threshold, your filing requirement will be different that what is indicated in the report.

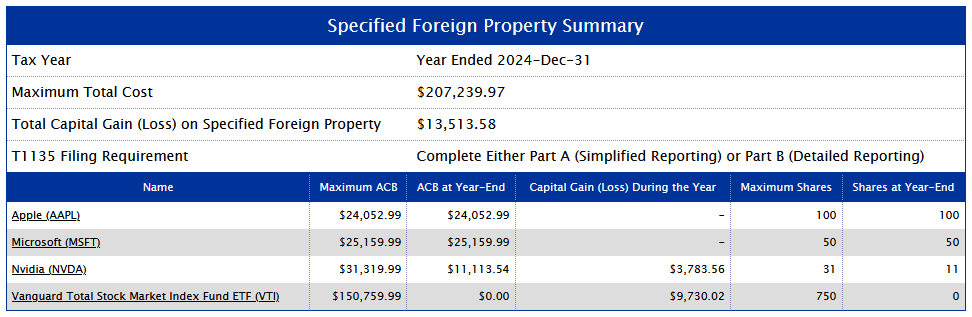

The total capital gain or loss on specified foreign property is also provided (useful for completed Part A).

The report also includes a breakdown of each specified foreign property owned throughout the year. The maximum ACB (calculated based on the maximum month-end value if the “Calculate Maximum ACB Using Month-End Values” option is enabled), the year-end ACB, total capital gain/loss, maximum shares and share balance at year end are also provided on a per-security basis. This information is useful for completing the details for individual specifing foreign properties, if you are required to complete Part B. If you choose to aggregate foreign property held at a Canadian securities dealer in Category 7, you’ll need to separately determine the aggregate fair market values on a per-country basis.

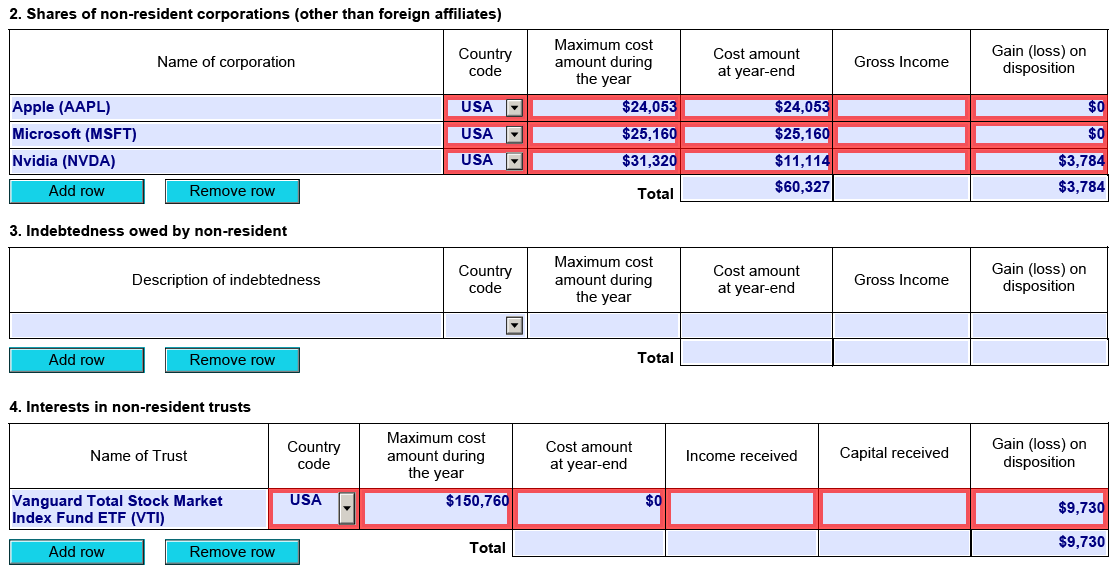

Here is how the information from the above example would be transferred into Form T1135 in Categories 2 and 4, if completing Part B:

Note that the information related to income is not provided by the Form T1135 Assistant report (this information cannot be derived from data inputted into AdjustedCostBase.ca). You should rely on your brokerage statements to obtain this information.

Since the definition for specified foreign property includes the right to acquire property, the cost of call options purchased to open are included when computing the maximum total ACB and the maximum ACB for particular securities. The capital gains or losses for a security includes gains or losses from options transactions, if applicable.

Is Vanguard FTSE Emerging Markets ETF (VWO) considered specified foreign property?

Dale,

VWO would be considered specified foreign property because it is a US-domiciled ETF.

Thank you!

Do you use trade date or settlement date for foreign securities calculation for ACB calculation? Is there no official stand from CRA yet in 2024?

Ajis,

Please see the following regarding the use of settlement dates:

https://www.adjustedcostbase.ca/blog/understanding-trade-dates-and-settlement-dates/

Settlement dates should still be used for foreign securities, but the delta between the trade date and settlement date may differ.

its quite confusing, i see in some comment from ACB that trade date should be used for foreign security and foreign cash calculation since its the price you paid on the trade date. The rate on settlement date would be different, but the actual transaction took place on the trade date.

Ajis,

It sounds like you are referring in particular to the date to use when converting amounts in foreign currency to Canadian dollars. The only communication from the CRA I’m aware of regarding use of the exchange rate from the settlement or trade date is the following:

http://web.archive.org/web/20201129104252/https://taxinterpretations.com/cra/severed-letters/2015-0588981c6

This suggests using the exchange rate from the settlement date. In any case, I would recommend being consistent with whichever method you choose.

Would Fidelity Advantage Bitcoin ETF (FBTC) be considered foreign property?

Mark,

No, FBTC is not be considered specified foreign property (it is a Canadian-domiciled ETF).

How does one determine where a security is domiciled for the purpose of T1135? I thought the 2-character prefix (country code) in the ISIN would indicate the domicile. The ISIN for Brookfield Renewable Partners L.P. units is BMG162581083 (Bermuda) but their website states “For the purpose of reporting foreign property by Canadian investors, pursuant to section 233.3 of the Canadian Income Tax Act, Brookfield Renewable Partners is not a specified foreign property and therefore does not need to be reported on Form T1135 Foreign Income Verification Statement.” Is the domicile not Bermuda in this case? Or is Bermuda somehow exempt?

Karim,

Section 233.3 of the ITA referenced in Brookfield’s FAQ states that the definition of specified foreign property does not include “an interest in a partnership that is a specified Canadian entity”. The definition of a specified Canadian entity (for a taxation year or fiscal period means) includes the following:

It may be that BEP meets these criteria, though I am not entirely sure.

Also note the following:

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/information-been-moved/foreign-reporting/foreign-income-verification-statement.html

This could be another reason why a partnership holding would not need to be considered as specified foreign property, though this isn’t likely to be the reason here since Brookfield makes no mention of this in their explanation.

I’m not that clear on what type of property to choose for the common examples of SFP mentioned (shares of US corporations, shares of US-based ETFs) when held with a Canadian brokerage. It seems like “Shares of non-resident corporations” is the obvious pick for US/foreign shares, and the example given on this page chooses “Interests in non-resident trusts” for US ETFs like VTI. But doesn’t the “Property held in an account with a Canadian registered securities dealer or a Canadian trust company” suit those properties as well?

Preet,

If you are required to complete Part B, you can choose to report shares of US corporations or ETFs are held in a Canadian brokerage in either Category 2 or Category 7.

HI. so vbal.to and xbal.to and things like xuu.to xec, xef.to and their vanguard counterparts all listed on tsx do not need to be reported on t1135?

Divi,

Yes, that’s correct.

For the foreign stock holding (e.g. Microsoft, AAPL), would the “income from specified foreign property” mean the dividend received by holding these foreign stocks and converted in CAD?

AK,

Yes that’s correct.

What is your reasoning for only including call options purchased to open out of all the option transaction types? My Interactive Brokers T1135 worksheets also include put options purchased to open (but not call/puts sold to open). Taxtips.ca’s interpretation is that put options are ambiguous. The ITA’s 233.3(1)(i) wording is “convertible into, is exchangeable for or confers a right to acquire, property”. If there is ambiguity, shouldn’t we err on the side of caution and include more transaction types rather than less?

Simon,

233.3(1)(i) is the following:

When you purchase a put option to open, you are acquiring the right to sell an underlying asset at a set price. Because the legislation specifically targets the “right to acquire” property, purchased puts do not appear to meet the definition of SFP. You hold the power to divest, not the power to obtain.

I don’t see any commentary on TaxTips.ca about put options purchased to open. They provide the following commentary on put options that are sold to open:

https://www.taxtips.ca/filing/foreign-asset-reporting.htm

This is a solid argument against including put options that are sold to open as specified foreign property.

Including put options sold to open would also raise some questions about how to report this. Put options do not have a cost amount associated with them for the seller, so it’s not clear how this would factor into determining your reporting requirements. And since there is no cost or income associated with the put options, there wouldn’t be much to report on either Part A or Part B of the T1135 (though if specified foreign property does not produce any income, that alone does not exempt it from the reporting requirements).

if I own a property in USA for personal use (never rented or having any form of income in USA do I have to report this in T1135 ???? I did asked numerous time the CRA agents they say NO report , but I told them , than why The CRA are penalizing for not reporting , and I did look on form T1135 part B ( it is over 250000 )there is no line to be reported vacation home no income , so what to do

Mariana,

Property that is primarily for personal use does not qualify as specified foreign property:

https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/information-been-moved/foreign-reporting/questions-answers-about-form-t1135.html

If you are being penalized for not completed Form T1135 it may be that you checked the “Did you own or hold specified foreign property at any time in the year with a total cost of more than CAN$100,000?” box on your T1 but didn’t complete Form T1135.

I reveived free shares from the company I worked at in previous years, at the time they were taxed as acquisition gain, with a sell to cover process.

Now I have those foreign shares in a foreign institution, so they should be declare in category 2.

My question is what is the maximum cost and cost at year end since they were free ? Is it the fair market value at the time I received them ?

Jo,

Normally when you are granted stock/RSUs as an employee, you are deemed to have acquired the shares for an amount equal to their fair market value at the time the shares are vested. The fair market value should be included as part of your employment income reported on your T4.

Your ACB of the shares would increase by the total fair market value. This is the value that should be factored into the maximum cost value for the purposes of your T1135 reporting requirements.