For tax purposes, it’s important to understand the distinction between the trade date and the settlement date:

- The trade date is the date on which you purchase or sell shares/units.

- The settlement date is the date on which you begin to legally begin own the shares (in the case of purchase) or cease to own the shares (in the case of a sale).

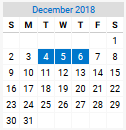

For Canadian and U.S. equities, the settlement date is 2 business days after the trade date. For example, if a trade is placed on Tuesday, December 4th, 2018 (the trade date), the settlement date would be 2 business days later: Thursday, December 6th, 2018:

Holidays when the stock markets are closed do not count as business days.

For other kinds of investments, including foreign equities, options, mutual funds, money market funds, bonds, commodities, and GIC’s, the gap between the trade and settlement dates can vary (the settlement date is usually between 0 and 3 days following the trade date). The settlement date should be provided by your bank or brokerage on your trade confirmation notice (or a similar document) so it’s always best to check there.

Note: the settlement date for most securities in North America changed to T + 2 as of September 5, 2017. Prior to this date, the settlement for most North American securities was T + 3 (a trade settled 3 days following the trade date).

Why Is the Settlement Date Important?

When selling a security towards the end of December, it’s possible for the transaction to settle in the next year. This means that any capital gain or loss incurred may apply to the next year even if the trade occurs in the current year. Deferring a sale into the next year can be advantageous in the case where a capital gain occurs, or disadvantageous for a sale involving a capital loss. In any case, the capital gain or loss must be reported in the correct year.

Determining the final date on which stock trades can occur and settle before the end of the year can be tricky. Markets in Canada are closed on Christmas Day and Boxing Day, so these days do not count for the 2-day period between the trade and settlement dates (see the TSX holiday calendar). Also, holiday schedules can be different between the U.S. and Canada as Boxing Day isn’t a holiday in the U.S.

For 2018, for Canadian equities, the last trading date resulting in settlement in 2018 was Thursday, December 27th, 2018 (December 25th and 26th were holidays). Any trade placed on Thursday, December 27th would settle on Monday, December 31st. Any trade placed after this date would settle in 2019.

For 2018, for U.S. equities, the last trading date resulting in settlement in 2018 was Thursday, December 27th, 2018 (only December 25th is a holiday since Boxing day isn’t observed in the U.S.). Any trade placed on Thursday, December 27th, 2018 would settle on Monday, December 31st, 2018. Any trade placed after this date would settle in 2019.

For 2019, for Canadian equities, the last trading date resulting in settlement in 2019 will be Thursday, December 27th, 2019.

For 2019, for U.S. equities, the last trading date resulting in settlement in 2019 will be Thursday, December 27th, 2019.

For 2020, for Canadian equities, the last trading date resulting in settlement in 2020 will be Tuesday, December 29th, 2020.

For 2020, for U.S. equities, the last trading date resulting in settlement in 2020 will be Tuesday, December 29th, 2020.

The Settlement Date and Collecting Dividends

In order to collect a dividend, the shares must be owned on the record date. Note that the record date is distinct from the payment date. Typically the record date can be between a few days and a month before the payment date.

Another related date is the ex-dividend date, which occurs 1 business day before the record date. The ex-dividend date can be used to determine whether you’ll receive a dividend by comparing it to the trade date. If you purchase shares before the ex-dividend date, you’ll receive the dividend. On the other hand, if you purchase shares on or after the ex-dividend date, you won’t receive that dividend. Similarly, if you sell shares before the ex-dividend date, you won’t receive the dividend.

The Settlement Date on AdjustedCostBase.ca

When using AdjustedCostBase.ca to track your adjusted cost base and capital gains, your transactions should always use the settlement date for buy and sell transactions. This ensures that capital gains and losses will appear in the correct years.

Also, any transactions involving distributions for ETF’s / funds / trusts (such as Return of Capital, Capital Gains Dividends, and Reinvested Capital Gains Distributions) should use the record date that applies for the distribution. Again, this ensures that any applicable capital gains and losses are reported for the correct year. Even more importantly, when using per share amounts for a distribution, using the record date is necessary to ensure that the distribution is applied to the correct number of shares.

We can illustrate this with an example. Suppose you purchased 400 units of VVV on the Toronto Stock Exchange for $100/unit traded on Thursday, January 3rd, 2019, with a commission of $10. Then trading on Monday, December 30th, 2019, you sell all 400 units for $80/unit with a commission of $10.

Before entering the transactions into AdjustedCostBase.ca, the trade dates should be converted into settlement dates. Since the settlement date for Canadian equities occurs 2 business days after the trade date, the transaction details are as follows:

- Buy 400 units of VVV for $100/unit with a $10 commission, settling on Monday, January 7th, 2019.

- Sell 400 units of VVV for $80/unit with a $10 commission, settling on Thursday, January 2nd, 2020.

The sale transaction’s settlement date occurs 3 days after the trade date because January 1st is a holiday. After entering these transactions into AdjustedCostBase.ca you should see the following:

Since the settlement date of the sell transaction is in 2020, the capital loss cannot be claimed for 2019 (even though the trade happened in 2019).

As explained above, another situation where special attention needs to be paid is when distributions occur around the same time as a purchase or sale. Let’s look at the following example:

- Purchase 100 units of ACB traded on Friday, December 27th, 2019 on a Canadian exchange for $100/unit and a $10 commission.

- A dividend is declared for ACB with a record date Tuesday, December 31st, 2019 for an amount of $0.50/unit, which is entirely return of capital.

The trade date needs to be converted into a settlement date. In this particular case, the settlement date is Tuesday, December 31st, 2019 (2 business days later). These transactions appear on AdjustedCostBase.ca as follows:

In this case the shares are owned starting December 31st, so the return of capital does indeed apply. Note that since the settlement date is the same as the record date in this case, the order of the transactions must be correctly set.

Note that the default date for new transactions on AdjustedCostBase.ca is today’s date. If you’re in the habit of inputting transactions on the very same day they occur, you should remember to adjust the date when necessary so that it corresponds to the settlement date.

There are many cases where you can get away with being sloppy and mix up the settlement and trade dates. When trades don’t occur at the end of December and when trades don’t coincide with dividend record dates or ex-dividend dates, the transaction dates being off by a few days without any noticeable affect. But this can lead to problems down the road. For example, suppose you enter a purchase transaction without being careful about the date. Then later on you enter a distribution transaction as a per share amount with a date around the same time as the purchase transaction. If you’ve forgotten that you need to carefully check the date of the purchase transaction, you may end up incorrectly applying the distribution to too many or too few units.

Hi – I have been tracking ACB for US$Cash in my US$stock account. While I understand the necessity of using settlement date over transaction date for records, but I am not sure which date to use for the C$/US$ exchange rate. Intuitively I think I should use the transaction date exchange rate. Is this correct.

Tom,

I’m not aware of any source that confirms the CRA’s stance on this, but it makes more sense to me to to use the exchange rate on the purchase/trade date as opposed to the settlement date. The share price for a transaction (with or without foreign currency involved) is of course based on the market price on the trade date, not the settlement date, so it seems logical to extend this to the foreign exchange rate. And in cases where Canadian dollars are actually converted when purchasing stocks, the actual exchange rate is based on the exchange value on the trade date.

When I am trading in USD and do not exchange to CAD in between, should I not use the Trade date to establish the cost base in CAD? It is easier to get the exchange rate at the time of trade from the broker than having to look up the BOC rate 3 days later on settlement date. I am talking about figuring out the capital gains on the income tax form. Thanks for your reply

Gary,

Please see the comment above.

Also note that many markets including the major Canadian and US stock markets are switching to a settlement of T+2 days instead of T+3 days as of September 5, 2017.

Hi there, if one is to use the TRANSACTION date when changing USD to CAD in trading foreign currency securities, does one still use the SETTLEMENT date to determine the proper tax year the capital gain or loss is applied.

Femi,

A capital gain or loss should be applied according to the year of the settlement date.

Hi there, when using Simpletax capital gains or losses table section, it does NOT ask for the settlement date, just the proceeds, ACB, and outlays. So, how does one add the settlement date. Thanks.

Femi,

The settlement date does not need to be included on Schedule 3. You just need to ensure that each disposition is included in the correct year’s tax return.

Hi there, when using a brokerage’s currency conversion spread (75- 199 basis points), should we include the basis point or subtract it. example Bank of Canada exchange rate on March 16, 2017 is 1CAD = 0.7508, but my brokerage firm is 1CAD = 0.7399 (196 basis points). Which is acceptable to use. Thanks.

As far as I can see, CRA’s “Capital Gains” guide doesn’t distinguish between trade date and settlement date, let alone say which to use. So how do you know that (e.g.) capital gains/losses should be ascribed to the year of the settlement date and not that of the trade date?

Femi,

If currency has actually been converted then you should use the actual exchange rate paid, which factors in the conversion spread. This reflects your actual costs, and including the spread is to your benefit as it will reduce gains. If, on the other hand, no actual exchange took place (such as selling US stocks with the proceeds remaining in US dollars) then you should not include the spread.

Michael,

This is one of many rules that the CRA is not very clear on. The CRA stated In Interpretation Bulletin IT-133 that the settlement date should be used as opposed to the trade date. The CRA cancelled this interpretation bulletin, however. But then the CRA has apparently clarified that the portion of IT-133 that stated that the settlement date should be used is still valid.

https://taxinterpretations.com/cra/severed-letters/2012-0468931c6

“We confirm that, notwithstanding the cancellation of IT-133 Stock Exchange Transactions Date of Disposition of Shares, the CRA considers the settlement date to be the date of disposition of shares for income tax purposes.”

Thanks!

Is it safe to assume that for Canadian taxes on USD dividends (paid in USD and not exchanged for Canadian dollars) one should use the Bank of Canada rates for the settlement date (on which they were actually paid), not the record date?

Thanks for your help in this.

M,

The CRA doesn’t seem to very clear on whether to use the exchange rate from the payment date or the record date for dividends you receive in foreign currency. It seems more reasonable to me to use the exchange rate from the payment date, since that closer to the rate that would be used if the funds were actually converted.

On January 4, 2018, I asked my financial advisor to sell part of a mutual fund I owned and transfer the sale money to my TFSA and then use the sale money to purchase units in a different mutual fund to be held in my TFSA. The sale money from the original mutual fund was not transferred to my TFSA account until two business days after the sale of the original fund and then the new fund was not purchased in my TFSA account until the next business day. So, it took a total of four business days for the sale to finally be completed. I was irked by this delay because the NAV of the new fund had increased in each of the days since I made my initial request for the trade on January 4th. When I questioned by financial advisor about it he mumbled something about the trade needed to “settle” which I really didn’t understand. In particular, what I don’t understand was why it took two business days to transfer the money from sale of the original mutual fund to my TFSA before purchasing the new fund. I would appreciate your thoughts on the matter. Thanks.

D,

It’s normal for mutual funds to take a couple days to settle. And there could be cut-off times for both buying and selling that may extend this time. During this time, the cash isn’t yet available in your account.

Hi,

You’ve suggested that the exchange rate on the purchase/trade date (as opposed to the settlement date) should be used when tracking the ACB of foreign currency. A problem with this approach, however, is that the transaction date that ultimately appears in bank statements usually does not match the actual purchase date, e.g. I placed three different orders on eBay.com on February 11, 2018 (Sunday), all of them paid in USD using a US PayPal account linked to a US bank. When I check my account statement, I see two transactions posted the following day (Monday) and the other one posted two days later (Tuesday). So in the case of deemed dispositions of foreign currency, I guess the recommendation would be to use the “post date” (sort of “settlement date”) instead of the actual “purchase/trade date”?

Thanks in advance.

Daniel,

The above information relates to the purchase of securities such as stocks and bonds. This is not related to the posting date you might see for credit card purchases or other payments.

Yes, I’m aware the above article relates to securities, I was actually referring to the comment you made on December 1, 2016 in response to Tom’s question about which date to use for the exchange rate when you are tracking the ACB of foreign currency. In my US bank statements, posted dates for debit transactions usually do not match the actual purchase/order dates found on the seller invoices. Sometimes this is deliberate (e.g. Amazon.com policy is to charge the payment method once the order ships), but more often than not the bank will post transactions with some delay even if the purchase/order was processed on the same day by the seller. Would it make more sense then to base all exchange rates on the posted dates reported by the bank? Thanks.

Daniel,

I’m uncertain which exchange rate should be used in that case. Most likely any should be acceptable if you’re consistent.

Hello there,

Just want to mention this to you. CRA is actually very clear that settlement date not trade date should be used for not just capital gain/loss calculations but also for converting transactions from foreign funds to CAD. According to this APPF roundtable discussion with CRA on Financial Instruments that took place on Oct. 9, 2015, CRA answered specifically that for converting proceeds & ACB’s from foreign funds to CAD to calculate capital gains/losses for capital account, one is to use the daily noon rate published by Bank of Canada on the settlement date. Here is the website link: https://taxinterpretations.com/cra/severed-letters/2015-0588981c6. It’s in French but the summary is in English.

There is a lot of confusion regarding this so I thought I put in this. Hopefully this would clear things a bit and make tax time a little bit easier for all of us. Personally I feel using trade date makes more sense but CRA wants to use settlement date because it believes that’s the time when money actually changes hands. So far I haven’t seen any publication that says CRA has changed their mind on this so I have been using settlement date for the conversion purposes to calculate the capital gains/losses. It’s a major royal pain in the ***.

Daniel,

For any other transactions such as credit card transactions, other than stock market securities transactions, CRA’s position is one should use the exchange rate when the transaction occurs. For example, if you bought a diamond using credit card and on that date, the USD/CAD exchange rate is 1.3380 but when the transaction actually posted to your credit card, 3 days later, the exchange rate becomes 1.3000, CRA states that it should be the rate 1.3380 that is used, not 1.3000.

Hope this helps.

Catherine,

Thanks for sharing. While that roundtable document seemingly answers some important questions, I don’t place much value on it. It’s a transcription of a verbal statement made by one particular CRA employee. It’s not published on the CRA’s web site, nor is it officially available in English. Much of the content isn’t backed up by either the CRA’s web site or the Income Tax Act, and some content even contradicts clear statements on the CRA’s web site.

That being said, exchange rates don’t usually fluctuate much over a couple days, so using one date versus the other will not usually make much difference. It is probably best to pick one way and be consistent with it. Whenever an actual currency exchange occurs, then I would suggest using the actual exchange rate.

So if I have a security that has distributions, the buy and sell transactions should use settlement date, but the distribution transactions should use record date (which is typically well before settlement date)?

Are there any other kinds of transaction where I shouldn’t use the settlement date?

M,

Yes, ACB should be calculated based on purchase and sale transactions occurring on the settlement date. Distributions should be based on the record date as far as I know. Note that the date when cash is received from a distribution is generally referred to as the payment date.

“Note that the date when cash is received from a distribution is generally referred to as the payment date.”

Yes, I should have been clearer about that. It’s just that my brokerage puts the payment date in the “Settlement Date” column, so I tend to think of it that way.

So do you know of any other kinds of transactions (besides distributions) where one shouldn’t use the settlement/payment date?

M,

Splits and other corporate actions such as mergers and spin-offs do not have a settlement/payment date.

Hi,

I need a little clarification if possible.

In the case of a Dividend payout : I received a dividend distribution on 100 shares received 12/31/18 and payed out the 01/04/19.

I made a separate purchase of 25 units of the same share that was placed the 31 Dec 2018 and settled the 3 Jan 2019.

The problem that arises is that by using the settlement date of both, the dividend distribution is being shown as received on 125 units instead of the 100 that it should be because the settlement date for the dividend distribution is on the 4th, a day after the settlement date for my new purchase.

I know that the value of the NEW ACB is unaffected but wanting to indicate the accurate information, how would you suggest that I input the data?

Should I input the Dividend distribution date as being received the 31 Dec 2018 instead of on the payment date?

Should I push my settlement date of my new purchase to the 4th of January?

Thanks

S,

While the trade date and settlement date for a transaction and the record date and payment date for a distribution are similar concepts in some ways, they are not exactly the same thing.

I would suggest that you use the record date for the distribution rather than the payment date, in particular if these are units of an ETF or other fund/trust. I’m assuming that these are in fact fund/ETF units as distributions that affect ACB including return of capital or phantom distributions are typically from funds or ETF’s. The settlement date should be used for the purchase.

According to the following:

https://www.theglobeandmail.com/investing/education/article-your-year-end-investing-questions-answered/

“If an ETF declares a distribution in December but pays it in January, in what year is the distribution taxable?

For ETF’s, it is the record date that matters. If the record date is in 2018 but the payment date is in 2019, the distribution will be taxable in 2018. With stock dividends, on the other hand, the payment date determines when the dividend is taxable. A dividend with a payment date in 2019 will be taxable in 2019, even if the record date was in 2018.”

Assuming this to be the case then indeed it would indeed make sense to use to record date for any distributions affecting ACB.

Curious what date you use for original purchase date on a tax form – if you are buying and selling portions throughout the year – do you stick with the original first day of purchase?

Say you buy 1000 shares in Jan, sell 300 in March, buy 200 in June, sell 600 in October, etc.

That sort of thing

Adrian,

Schedule 3 asks for the year of acquisition for each disposition, not the exact date. So if the shares were acquired on different days of the same year then there isn’t anything to worry about regarding this.

The form is not adequately designed for cases where the purchases spanned different years, however. I have not seen any instructions from the CRA to deal with this case, but I always put the first year of acquisition. The capital gains reports generated by AdjustedCostBase.ca include all years of acquisition associated with each disposition.

Maybe I missed this, but what happens when it’s a stat holiday in one country but not the other. Which dates are then used to calculate the settlement dates?

David,

The settlement date depends only on the stock exchange where the shares are purchased, not on your location. If there is a holiday on the stock exchange where the shares are purchase immediately after the purchase then the settlement date will likely be delayed.

Sorry. Perhaps I didn’t give enough information. In my case, I live in Canada, and I sold a US stock listed on the NYSE on Thursday, May 14th, 2020. The settlement date should be Monday, May 18th, which is two days later. Normally, I would look up the CRA-related website that gives the tax-accepted exchange rate for May 18th. However, because May the 18th is Victoria Day in Canada, the website puts no exchange number at all, as if it were Saturday or Sunday. I suppose my question is, should I use the exchange figure posted on Friday, May 15th, or the exchange figure posted on Tuesday, May 19th? Thank you.

David,

In such cases I think it is fine to use the exchange rate from either the previous or next Canadian business day.

Thank you.

Today is June 13, 2020

I have a transaction date on June 11, 2020 and settlement date on June 15, 2020 (two days from now). Problem is this is a USD currency and the exchange rate is not yet posted obviously… So I guess I have to wait until the 15th to enter the transaction?

Also, I was told that Norberts Gambit is also taxable. Is this correct? Im basically entering the transactions as if… But how about normal curreny exchange? Im new to the investing scene just a month old so I wasnt aware of Norbets gambit at that time.

BTW HUGE THANKS TO THIS WEBSITE! It definitely saved me some headache!

Chess,

Yes, you would need to wait until the settlement date to know the exchange rate for that date. However, it is debatable whether the exchange rate on the trade date or the settlement date should be used. I prefer to use the exchange rate on the trade date as that is when the trade price is established and if an actual currency exchange had occurred the exchange rate would have been based on the prevailing rate on the trade date, not the settlement date. In most cases there’s minimal fluctuation in currency rates between the trade date and settlement date so it should not have a huge impact. I would suggest selecting one method and sticking with it.

Capital gains or losses can potentially apply when using Norbert’s Gambit.

How would someone apply on your website a regular foreign exchange from questrade? I supposed I would:

1. Add New Security and say CAD to USD as name

2. New Transaction as a BUY and Price (?), Shares (?)

Then…?

Sorry Im completely new to investing, only been a month. And Ive never dont this taxes before.

CHESS,

Here are some resources that should hopefully cover this:

https://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-foreign-currency-transactions/

https://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-for-foreign-currency-cash/

hi there, ACB.ca,

many thanks for this great resource. I’ve been reading through your site and comments and other sites as well and still cannot find the preferred rate to use for foreign transactions wrt to trade vs settlement date. It seems like TD, RBC, taxtips.ca, and others want to use the settlement date, but I feel like your conclusion in this thread seems spot on absent any official CRA reference: pick a method and stick to it.

For dividends it doesn’t seem as straightforward. you mention in an OCT2017 comment that:

“The CRA doesn’t seem to very clear on whether to use the exchange rate from the payment date or the record date for dividends you receive in foreign currency. It seems more reasonable to me to use the exchange rate from the payment date, since that closer to the rate that would be used if the funds were actually converted.”

but later in 2018 and beginning of 2019 you say that the record date should be used. I think I may be mixing up Canadian ETFs issuing distributions that affect ACB and foreign US stocks paying dividends on a date which affect income. I’ve been using the settlement date for all dividends issued by foreign held stock/funds/ETFs as they all seem to count as income to the CRA and foreign ROC does nothing to ACB from what I understand.

If you have a page that details the latest and most up to date CRA/CPA opinions on which dates to use for what transactions broken down by Canadian vs. Foreign sources please point me in the right direction, thanks!

HI,

I received dividends/distributions in USD. These dividends are treated as cash to purchase US-listed ETFs. Should I use the exchange rate on the date I use the dividend to “settle” a purchase? For example, I received $11.96 USD dividends on March 31,2020. On June 2, 2020, I sold shares of an ETF for USD $151.48 and bought shares in REET for USD $163.44 that same day as well. Is it correct to use the exchange rate in effect on June 2?

@ Clare,

As I understand it, there are two transactions for you to record here with respect to taxation:

1) payment of a USD dividend which is subject to taxation in CDN at the exchange rate on the date of record (though it might be settlement so be sure to check this further, or just use the annual average rates if the dates fall within the same year);

2) a later purchase in USD , for which the ACB will be determined in CDN using the exchange rates on the date of purchase.

Just because you held the dividend in USD doesn’t mean a taxable event didn’t occur.

Hope that helps somewhat.

If you need to compute the settlement date for hundreds of transactions on various exchanges, is there a spreadsheet-friendly way to do that? More to the point, I need a chart listing all business days for the given tax year, over which I can use a LOOKUP function.

The best I can think of are historical charts of a benchmark index for each exchange I am trading on (e.g. DJIA for the NYSE) and to use their date column. Any other idea?

Which raises another interesting question: If a stock exchange is closed due to unforeseen circumstances (https://www.dividend.com/dividend-education/7-events-that-closed-the-nyse/), does that affect settlement dates?

I’ve done this using a look up function with downloaded BoC and US treasury historical rates. Once you manage to align the date formats it goes smoothly, but to do that you might learn all sorts of new text formulas!

Depending how far you have to go back you’ll hit your limit with BoC data, and should search for academic databases (the one that did it for me was from a UBC site). CRA reps will tell you that they are looking for sound methodology, as they can’t actually verify historical fx more than 10 years old.

Settlement date is the next open business day I think…

Can someone help me, If i converted say 50000 Canadian to us and have this money in cash at my broker. Say in a month I buy us stocks do I use the exchange rate on the day I buy the stock or Can i use the original conversation rate when i first converted Canadian to us

Raz,

This would be equivalent to the following:

1. Purchase of US dollars on the date of the currency conversion.

2. Sale of US dollars on the date the stocks are purchased.

3. Purchase of stocks.

The exchange rate for 1. can be based on the actual rate applied for the currency conversion. The exchange rate for 2. and 3. should be based on the prevailing rate at the time of the stock purchase.

Raz: If it’s for tax purposes, I would have thought that neither the date that you gave your broker the money nor the date that you purchased the stock would be relevant. I would think that the settlement date is the only day that would matter, which would typically be two business days after the purchase date.

David

Hi there,

Would you know what’s CRA’s position on whether to use transaction date or settlement date to convert transactions in options (puts and calls) denominated in foreign currency to CAD? I am aware that CRA has confirmed to use the exchange rate on settlement dates to convert transactions on foreign stocks but I can’t find any information on CRA’s positions with regards to foreign options. Would appreciate it if you can advise.

Thanks

I purchased and sold DKNG throughout 2021 but I had 400 stocks left which I held until Aug 2022 and sold at a deep loss, but how do I do the ACB for this sale as it is the only one fr 2022 for the stock

many thanks

Bruno,

ACB should be calculated on an ongoing basis, and does not reset at the beginning of a tax year. You should input your “Buy” and “Sell” transactions on AdjustedCostBase.ca based on the settlement dates of each purchase and sale.

I may have found a possible glitch in the system, though I am hoping it is just my own misunderstanding.

So far, every time I’m using the ‘Exchange Rate Lookup’ and have gotten the error “Sorry, the exchange rate is unavailable for that date. Exchange rates are only available on business days.” – it turns out that it was indeed my own fault, by accidentally putting in the wrong settlement date.

However, I finally found a situation I can not explain, despite re-checking for my errors.

In this case, my broker “IBKR” shows a settlement date of 2024-August-05 for the security name ‘GREE’.

When I check my actual calendar, it comes up as a Monday, and I can’t see any holiday that should have happened then. So this is puzzling.

Was there anything I am unaware of?

By the way, this blog maybe could be updated a tad because settlement dates have been upgraded to just T+1 this year. Which, also makes me wonder if somehow THAT may have something to do with this?

T,

We obtain our exchange rate data from the Bank of Canada, which does not provide daily exchange rates for Canadian bank holidays. Exchange rate data is not available for August 5, 2024 on account of it being Civic Holiday.

GREE trades on the NASDAQ and August 5, 2024 was not a US holiday. Trades placed on Friday, August 2, 2024 on US exchanges would have settled on Monday, August 5, 2024.

I would suggest applying the exchange rate for the next nearest Canadian business day (either Friday, August 2 or Tuesday, August 6). You can temporarily change the transaction date to one of these dates, perform the lookup, then change the transaction date back to August 5.

Yes, settlement changed from T+3 to T+2 in September, 2017 for major US and Canadian exchanges, and then changed from T+2 to T+1 in May, 2024.