AdjustedCostBase.ca has released a new feature that provides a fast and easy way for Canadian investors to import the tax information that impacts adjusted cost base and capital gains for many securities including Exchange Traded Funds (ETFs), Publicly Traded Mutual Funds and Trusts.

This feature is only available to AdjustedCostBase.ca Premium subscribers. The cost of the enhanced service is $49/year. The basic features of AdjustedCostBase.ca remain completely free for Canadian investors.

This feature saves Canadian investors a great amount of time and hassle. It works by automatically importing the capital gains, return of capital, and non-cash distribution information reported by public funds. In a few quick and easy steps, these transactions can be applied to a security in your account.

A vast number of funds are covered by this service. The coverage includes exchange traded funds (including ETFs from iShares, Vanguard, BMO, Horizons, PowerShares, First Asset, Purpose and others) as well as publicly traded mutual funds, income trusts and real estate investment trusts (REITs).

While this information can be imported manually, it’s a very tedious and error-prone process to research and interpret the tax information, input the transaction one by one, and ensure accuracy.

Let’s look at a real-world example involving the iShares Core S&P/TSX Capped Composite Index ETF (ticker symbol XIC). XIC is one of Canada’s largest and most widely-held ETF’s, with over $2 billion in assets.

Suppose you purchased 1,000 units of XIC settling on January 8th, 2015 at a price of $22.75/share with a $10 commission. After adding the security and purchase transaction in your account, the list of transactions would appear as follows:

![]()

The ACB for XIC is initially $22,760. Let’s assume that no other purchases and sales occurred for XIC in 2015 and that all the distributions were deposited into your account as cash. Even in this case, the ACB can still change as a result of return of capital or non-cash (reinvested) distributions, and indeed that’s what happened with XIC and 2015 (this is a very common occurrence with ETF’s).

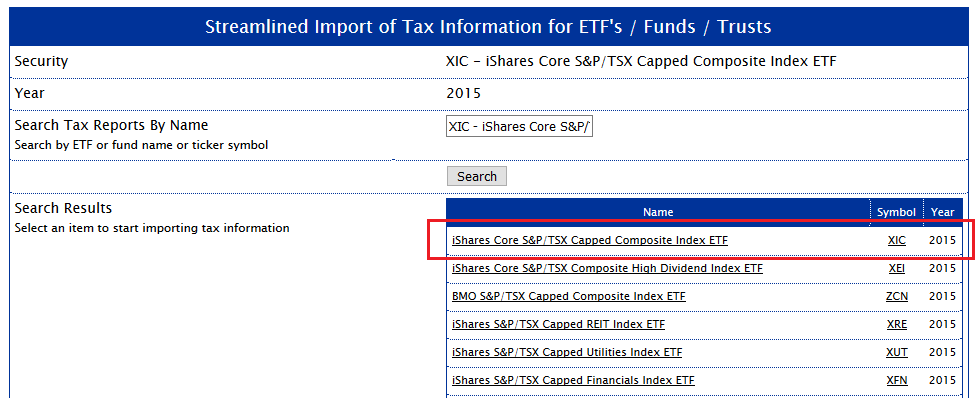

One option is to manually collect all the necessary information and enter the transactions, as described here. To save time and aggravation, AdjustedCostBase.ca provides a streamlined approach, allowing you to avoid this very cumbersome process. To access this functionality, follow the “Import Data” links in the “Streamlined Import of Tax Information” section on any security’s page. You’ll be brought to a form allowing you to search for the ETF in our database:

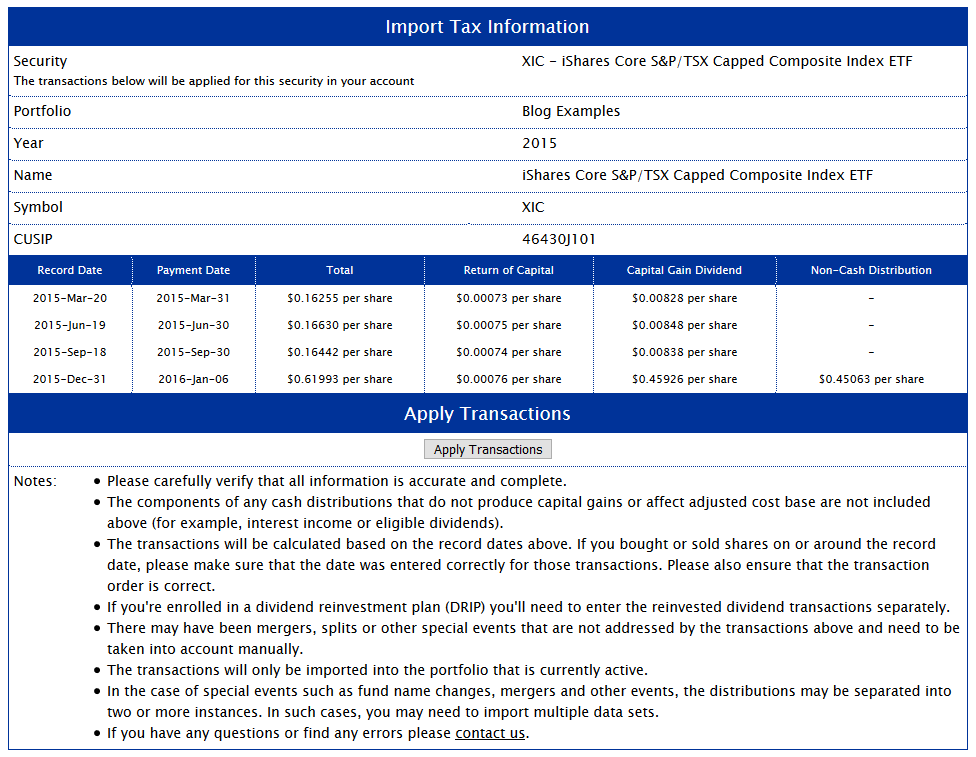

By searching for the name or ticker symbol for the year in question you can find the ETF. Note that you must still perform a search even if you’ve given your security the correct name. After following the link for the correct security, you’ll be brought to a page that shows all the return of capital, capital gain dividend, and non-cash distributions for XIC for the year.

Note: An AdjustedCostBase.ca Premium subscription is required to access the functionality below. However, AdjustedCostBase.ca Basic subscribers can still search for funds, as described above, in order to preview the list of available funds in our datatbase.

Only return of capital, capital gain dividends, and non-cash distributions are listed. Your fund may (and in fact most likely did) pay out cash distributions in other forms such as interest income or dividends.

After confirming that the details are correct, you can then click on “Apply Transactions”:

![]()

The transactions highlighted in yellow are the ones that were added. They include “Return of Capital”, “Capital Gains Dividend” and “Reinvested Capital Gains Distribution” transactions.

The most significant transaction is the Reinvested Capital Gains Distribution on December 31st. A Reinvested Capital Gains Distribution (also known as a Phantom Distribution or Non-Cash Distribution) is a reinvestment in a fund that’s usually coupled with a capital gain. The $450.63 in capital gains would be reported in box 21 of you T3 slip that your brokerage sends you.

The most interesting aspect of this transaction is the reinvestment component. This amount will typically not be included on your T-slip and as a result many investors fail to factor these transactions into the capital gain calculations. But it’s very much in your best interest not to overlook this. In this example, the reinvestment increases adjusted cost base by the same amount: $450.63.

If you were to fail to include the reinvested amount then your calculated capital gain (when you eventually sell the shares) would be $450.63 higher than it should be (effectively, you would be double-paying the taxes on this non-cash distribution). Assuming a marginal tax rate of 50%, you would end up paying an extra $112.66 in taxes ($450.63 x 50% x 50%). And that’s simply from forgetting to factor in non-cash distributions for just a single year and for just 1,000 shares of a single ETF. By taking advantage of this feature, an AdjustedCostBase.ca Premium subscription can easily pay for itself.

You will need to initiate the above process for each year you have a share balance for each ETF / fund / trust that you own. This step is necessary to allow you to review the details for correctness.

Tax information is added to our database very shortly after each fund reports its tax information for the past year, which typically occurs between early February and mid-March of the following year. If you don’t find tax information for a fund while searching towards the beginning of the year, please check back soon.

In your highlighted example, the capital gains dividend should be 0.45926 per share. Also, a general question, why does tracking capital gains dividends matter? It does not affect ACB.

Thanks!

Sorry, I meant the capital gains dividend should be 0.45926 per share for December 31, 2015.

Nevermind. I realize what the error was now. Please ignore my previous posts. However, I would still appreciate an answer to my question of why tracking capital gains dividends matters. Thanks and sorry for the confusion.

Bob,

You’re correct that capital gains dividends do not affect ACB. They’re taxable immediately and should be reported on your T-slip. You do not necessarily need to enter these transactions on AdjustedCostBase.ca (although reinvested distributions should at least be inputted as a “Reinvested Dividend” transaction if not a “Reinvested Capital Gains Distribution” transaction). However, this feature is offered for those who would like to see a complete total of all capital gains. AdjustedCostBase.ca will indicate whether or not each capital gain is reportable on a T-slip.

I just tried the premium service and I love it!! Thanks!!

Jasmin,

I’m glad to hear! Thank you for your feedback.

This is a great addition to your free service. My question is whether this fee can be deducted as a carrying charge. I understand CRA states you can deduct fees if your income is from business or property. I assume “property” includes investments and since calculating and tracking ACB requires (in my opinion) a great deal of regular accounting, it should be deductible.

Skube,

I would say yes, the fees can be deducted as a carrying charge (line 221), although I’m not completely sure.

As you’ve mentioned, fees can be deducted if you have income from property:

http://www.cra-arc.gc.ca/tx/ndvdls/tpcs/ncm-tx/rtrn/cmpltng/ddctns/lns206-236/221/menu-eng.html

The Income Tax Act defines “property” in section 248(1) to include investments such as shares:

And in this case the fees are very clearly dedicated towards your investments, whereas more general accounting and tax preparation fees can apply to a wide variety of things.

I just signed up for the premium service which looks great! I have used the free service for 2013, 2014 and 2015. I’m thinking about downloading the data for those years, just in case I made an error entering the data manually. If I do that, I guess i should delete all those manual entries first, or would it work to just download the data on top of the manual entries? Thanks.

Grant,

If you automatically import the data for past years, then you would need to delete the manually entered transactions in order to prevent them from being double counted.

This is a great service

Is there a similar service for US based ETFs ?

Ian,

For Canadian investors, all distributions from foreign listed stocks are considered to be foreign income. This is the case even if the distribution is considered to be the equivalent of return of capital in the foreign jurisdiction, for example. As a result, only Canadian listed funds are included in the database.

Good stuff! I’ve been using your Free service for years, entering my own RoC. Just upgraded to your Premium service, removed my old RoC transactions, and then imported for XIC, since 2009, using the new feature, just as described above. My ACB went up $0.35 as I hadn’t accounted for the reinvested capital gains distributions.

I then corrected my handful of other ETFs and saved future capital gains taxes far exceeding the $50 annual fee for the service, even if T2 leaves the inclusion rate at 50%… unlikely. Keep up the great work!

Guy,

Thanks for your feedback.

We’ll see what happens on Wednesday 🙂

Hi, This is a wonderful site and after trying out the free version (recommended by Canadian Couch Potato site) , I had no hesitation to upgrade to the premium version for the extras like the Capital gains PDF report and the ability to import the ROC and other amounts automatically. One question though, I have 2 ETF funds starting from 2016 that are on a DRIP plan and pay monthly Should I enter the DRIP reinvestments per month first before automatically using the streamlined import for ROC and other amounts, or does it matter.

Joe T

Joseph,

The ROC and phantom distribution transactions will be imported as per share amounts, so it won’t matter if you input any other transactions before or after. One thing to watch out for is to ensure that a reinvested distribution transaction occurs after any ROC or phantom distribution transactions that correspond to that same distribution.

Further to my question above, and having just tried the service for the first time, I think the best way for checking whether prior years that were done manually are accurate, is to download the data on top of the old manually entered data. Then, as the auto downloaded data is clearly indicated, after checking the two sets of data side by side, delete one set. Thanks, great service!

It says above

“Only return of capital, capital gain dividends, and non-cash distributions are listed. Your fund may (and in fact most likely did) pay out cash distributions in other forms such as interest income or dividends.”

Why are these other cash distributions not included? Is it because they don’t alter the ACB? Easier to track? Reported on T5?

I’m considering buying the premium, just want to see if it is really worth it.

Thanks

Ryan,

Components of a distribution that are not return of capital and not phantom/non-cash distributions will not directly effect ACB. The only exception is when a cash distribution is reinvested as a DRIP.

Thanks. I have the Vanguard ETF VTI. It is not available in your database. Any chance this may change in the future? Is there another source where I might get this information and manually input it?

Ryan,

VIT is unavailable because it’s a US-listed ETF. US-listed ETF’s should not generally make distributions that involve return of capital or phantom distributions, and thus your ACB will be unaffected by distributions. The distributions are normally taxable as foreign income no matter how the distribution might be categorized by US tax law.

Pingback: Easier than ACB – Canadian Portfolio Manager Blog

Hello,

I’m not sure what post to place this in.

How would the ACB be conducted for this US ETF when I’m based in Canada?

https://image.prntscr.com/image/-XVjForvTBWpV40NOSp1PQ.jpeg

Can I deduct the “premium” fee just like the trade commission?

Edit above – Haven’t purchased ETF in USD funds before and realized that”s just the conversion rate on the CDN dollar to US with a small premium (official at 1.298 for Sept 14th) plus TD’s take.

So the ACB would be calculated as normal but just also adding in the factor of currency exchange. Or another way of saying it – a column in a spreadsheet for the exchange rate is added to the buy/sell price when calculating proceeds.

Adrian,

Some further information about that topic is available here:

https://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-foreign-currency-transactions/

I’m totally new to this site, and haven’t yet inputted any information to the basic site, or signed up for the premium service. My question concerns DRIP’s for common Stocks; does the premium service allow for the input of DRIP data and calculate the new ACB. If so, does it do this for both Canadian and US listed Stocks?

John,

Yes, AdjustedCostBase.ca supports the input of DRIP transactions. This information must be supplied by you, so it does not matter whether your stocks are Canadian or US-listed. For further information about DRIP transactions on AdjustedCostBase.ca, please see the following:

https://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-reinvested-distributions-dividend-reinvestment-plans-drips/

Pingback: Podcast 4: Charles Ellis and the Index Revolution | Canadian Couch Potato

How far back does your database of tax information go? I’m considering signing up for the premium service but have ETF purchases going back to 2008. Will the premium service be able to populate all of the ROC and Phantom Distributions from that period?

James,

Data is available going back to 2007.

After just upgrading to Premium, and applying the 2019 expedited insert of tax parameters, I have a question on distribution reinvestment dates. My broker delays credit to the account for synthetic DRIPs, and I’ve always used the date it was credited when posted to the ACB website account.

The taxable items seem to be based on the record date, and this probably affects the per share attribution made to the ACB adjustment for ROC and special capital gains transactions.

Should I now re-date the DRIPs to the record date, and trust the system to adjust automatically, or edit the transaction order manually to whatever is proper? And what is the right sequence, from earliest to latest: DRIP, ROC, Capital Gains Reinvestment, Other Special Taxable Event?

Please note that BMO has just posted a correction to NCD for ZLB from $0.27/unit to $1.35/unit. If I process 2019 now, will this autocorrect on my account, when you’ve allowed for the change, or should I just keep doing a trial processing until I see the new data?

Thanx, as always…

David,

Any return of capital amount will apply to the existing shares only, and not to the shares that were newly acquired as a result of the distribution. As a result, DRIP reinvestment transactions should occur after the other transactions corresponding to the distribution (either on a subsequent date or ordered last on the record date). In particular, return of capital should occur before phantom distributions, which should occur before the DRIP transactions. The tax treatment for special events such as splits and mergers will depend on a case by case basis, but normally they shouldn’t occur very close to a distribution record date.

If you use a date for the reinvestment that’s later than the record date of the corresponding distribution, it should not matter, unless:

– The date is much later and it falls after the record date for the next distribution

– You sold shares between the record date and the reinvestment date (although in this case, if you’re not considered to have owned the shares until the reinvestment date then using the reinvestment date seems like the correct approach)

BMO’s reinvested distribution for ZLB for 2019 seems to still be officially listed as $0.27/unit and their web site reports the same thing. Where did you see that it was updated to $1.35/unit?

If a fund ever updates their data in a way that could impact ACB calculations, your imported transactions will be automatically updated and you’ll receive a notification of the change.

I’m a bit confused by the information here.

So, for US listed ETF, what happens when I import the data downloaded from my brokerage account in the US? Will you be able to process the data properly?

Thanks.

James,

Tax breakdown data for US-based ETFs is not available for import because their distributions are generally taxable as foreign income for Canadians. This is the case even if the distribution is considered to be the equivalent of return of capital or capital gains in the US. Distributions from US-based ETFs should therefore not impact your ACB (unless the distributions are reinvested via a DRIP). The following article explains this well:

http://www.moneysense.ca/etfs/adjusted-cost-base-with-us-listed-etfs/

Thanks for your advice.

Just to clarify two points:

(1) For US-based ETFs, we can still use ““Import Transactions from Spreadsheet”, just like a stock, but don’t use “Auto Import Tax Information for ETFs/Funds/Trusts” – is my understanding correct?

(2) I read the Money Sense article, and my understanding from the reading is that capital gains distributions from US ETFs are fully (100%) taxable, but the capital gain from buying & selling an ETF itself is still only 50% taxable – is my understanding correct?

Thanks again!

James,

Yes, you can import transactions from a spreadsheet for any type of security, but there shouldn’t be a need to use the streamlined import feature. However, you will need to apply exchange rates to the buy and sell transactions to ensure that ACB is calculated correctly.

And yes, income from US ETFs should be fully taxable but capital gains (and losses) from dispositions are 50% taxable.

I was searching for a new holding HOT.un (American Hotel Properties REIT on TSE). It does not show in the search results, no matter how I enter ticker symbol or REIT Income trust name.

Any advice?

Ron,

The data for Limited Partnerships are not available by default, but can be added by request.

We have gone ahead and added the data for American Hotel Income Properties REIT LP from 2013 to the present.

Hello, I tried to look for the available list of ETFs for this feature, but at the moment it is showing the message: “No applicable securities and transactions found.”

Could you advise when the list will be made available? Thanks!

Henry,

Date for the vast majority of ETFs is now available for the 2020 tax year. Which ETF(s) in particular are you looking for?

Hi, I was looking for quite a few of them (iShares XIU, XUU, XEF, XEC etc, TEC, the ARK ETFs etc as well). I tried again just now to click on the view available data button, but it is still showing up as “No applicable securities and transactions found” unfortunately.

Henry,

You will need to first add a security and then add your buy and sell transactions. You’ll be able import data only for years where you’ve owned some shares.

Hi, when I enter transactions, should I put the date as the trade date or the date of settlement? Also, I imported the tax information for an ETF that I purchased in August, and on the next page, it listed all the return of capitals for the entire year – do I manually delete all the ones that were before my date of purchase? Thanks

Usually, my buy/sell transactions at my brokerage show up as two transactions even though I only made one transaction. For example, if I bought 105 shares of an ETF, it’ll show up as 100 shares purchased, plus another 5 shares purchased, even though I actually bought 105 shares all at once. So when I input this buy transaction, can I combine them as 105 shares?

SD,

You should use the settlement date for your purchase and sale transactions.

When you import data for an ETF, data corresponding to all distributions throughout the year will be applied (even distributions that occurred while you didn’t own any units). This won’t make any difference in terms of the calculations, because these are specified as per unit values. If you like you can manually delete any imported transactions that occurred while you didn’t own any units, but leaving them there will not be harmful.

It sounds like your brokerage is reporting separate transactions when multiple order fills occur. It’s fine to either join them together into a single transaction on AdjustedCostBase.ca or keep them separate. If you use separate transactions, you should ensure that the commission isn’t double-counted. You could either separate the commission in proportion to the number of units purchased, or apply the entire commission to one purchase and specify a commission of zero for the other purchase(s).

Hi ACB,

Thanks for your answer. After I apply the calculations, is the “Annual Capital Gains PDF Report” what I would give to my accountant so that my capital gains can be reported accurately?

SD,

Yes, that report is intended to be a summary of all capital gains/losses for the year and would be suitable for that purpose. It is designed to resemble Schedule 3, where capital gains and losses are reported on a tax return.

If I transferred some of my ETFs to a TFSA in-kind, so technically I didn’t sell, but for the purpose of calculating ACB, do I input the transaction as a sell?

Why is it that the numbers in the return of capital and capital gains dividend columns don’t add up to the totals per share?

Lastly, on the annual capital gains report, what is the difference between “total capital gains from T-slips” and the number in the gain (or loss) column? Why are these two numbers different?

Sorry for all the questions. I’m glad I paid for premium, otherwise I will be even more confused!

SD,

Yes, you should input an in-kind transfer to a registered account as a sell transaction. If there’s a capital gain then the gain will need to be reported, but if there is a loss then it will be denied according to the superficial loss rule.

The total distribution amounts usually include amount other than return of capital or capital gains including interest income, eligible dividends, foreign income, etc. These other amounts are reported on your T3 slips and are taxable in the year of the distributions, but they do not impact your ACB.

The “Total (from T-Slips)” value shows the total of all capital gain amounts that should appear on your T3/T5 slips. Inputting the T3/T5 slips into your tax software is sufficient to account for these amounts. The “Total (from Dispositions)” value is the total of all capital gains/losses occurring from dispositions. These values do not appear on your T3/T5 slips and should be inputted into Schedule 3 of your tax return, or the equivalent that your tax software provides.

Recently signed up for Premium Service to test if it fits my need. Unfortunately, it seems like American ETF are not supported? More specifically SCHD, QYLD, NUSI and JEPI.

Are there plans to support American ETFs soon?

XS,

Data is only available for Canadian ETFs. Distributions from US-domiciled funds are generally taxable as foreign income for Canadians and therefore the distributions should not impact your ACB. This is the case even if the distribution is considered to be the equivalent of return of capital or capital gains in the US. The following article explains this well:

http://www.moneysense.ca/etfs/adjusted-cost-base-with-us-listed-etfs/

Does your premium database include distribution information for Canadian split share funds (Class A and Preferred shares) like those offered by Brompton (e.g. GDV), Middlefield (e.g. ENS), and Quadravest (e.g. DFN)?

Thanks

WSC,

Yes – data for split share funds including the ones you’ve mentioned is available. You can try searching for these funds before upgrading (you just won’t be able to complete the final step of applying the data before you upgrade the AdjustedCostBase.ca Premium).

Hello, I use the Streamlined Import of Tax Information which pulls info from CDS. What happens if CDS revises a record on their end after I have already imported? Thank you.

Karim,

If there is a revision of the data which you’ve already imported, and it impacts your ACB or capital gains, the transaction data will be automatically updated and you will receive an e-mail notification.

In many cases, revisions do not have any impact. In such cases the data will not need to be updated and you will not receive a notification.

is there a link or section that describes all benefits of the premium service please?

If not you are more than welcome to e-mail them to me. Thank you for the help you offer us all on the website

Cedric,

You can see a comparison of AdjustedCostBase.ca Premium vs. Basic by following the “Manage” link on the top right just below the main blue menu bar (while logged in).

Here is a list of features that AdjustedCostBase.ca Premium offers:

Hello,

I’ve recently joined this website and starting entering info from years ago. Does it matter the order when I do the streamline import? For example, if I’m entering 2018- 2024, can I enter all the transactions buy/sell transactions and then streamline 2018, 2019, 2020, etc.

Or should I enter all transactions for 2018, streamline, then enter 2019, streamline, etc?

Thanks.

Tammy,

This does not matter either way and will not impact the result. The only restriction is that you won’t be able to import the data for a particular year if your share balance is zero for the entire year.

Newbie question: Do I have to enter all of my buy/sell transactions for an ETF before importing data from you or can I enter/edit these later?

Don,

You don’t necessarily need to input your complete transaction history before importing the data. However, you won’t be able to import any data for a given year unless you have a positive share balance during at least some part of that year. After importing the data you can go back and add/edit/delete transactions.