The tax consequences of investing with stock options on capital account are complex in comparison to directly investing in stocks. The tax treatment is as widely varied as the different combinations of opening options transactions (buying/selling put/call options) and closing transactions (the options can expire, can be exercised, or can be bought/sold to close). When stock options are exercised, there is added complexity in calculating the adjusted cost base and capital gains for the underlying security.

Here we’ll discuss the tax treatment of stock options for Canadian investors under the assumption that the trading occurs on capital account. This differs from the tax treatment when the trading is considered to be on income account. The rules for determining whether trading is on capital account or income account are somewhat subjective and beyond the scope of this discussion. But some of the conditions the Canada Revenue Agency may use to determine that trading is on income account include the following:

- When the trading is characteristic of a professional trader

- Frequent trading or short holding periods

- Extensive knowledge and time spent researching the markets

- Substantial use of debt to finance the purchases

- Use of special information not available to the public

The CRA generally considers options trading to be on the same account as transactions for shares. Selling of naked call options is generally considered to be on income account, but the CRA will allow this to be considered on capital account provided that this is done consistently from year to year.

The general taxation rules for stock options on capital account dictate that a positive cash flow is immediately taxable as a capital gain. A negative cash flow cannot be claimed as a capital loss (or reduction in capital gain) until the options transaction is closed (or the underlying shares are sold, in the case where shares are acquired due to the options being exercised).

The tax treatment of stock options on capital account is summarized in the table below. The possible opening transactions (Buy Call Options, Buy Put Options, Sell Call Options, and Sell Put Options) are shown in the top row and the possible closing transactions (Options are Exercised, Options Expire, and Options are Closed) are shown in the first column. To determine the tax treatment of a particular options transaction, look at the cell corresponding to the relevant opening and closing transactions.

| Buy Call Options | Buy Put Options | Sell Call Options | Sell Put Options | |

| Options Expire | The cost of the options is a capital loss in the year the options expire. (Example 1) | The proceeds from the sale of the options are a capital gain in the year the options are sold. (Example 5) | ||

| Options are Closed | The cost of the options is deducted from the proceeds of the sale to determine the capital gain (or loss) in the year the options are sold to close. (Example 2) | The proceeds from the sale of the options are a capital gain in the year the options are sold. The cost of the options is a capital loss in the year the options are bought to close. (Example 6) | ||

| Options are Exercised | The cost of the options plus the cost of the shares is added to the ACB of the underlying security when the options are exercised. (Example 3) | The cost of the options is deducted from the proceeds of the shares when calculating the capital gain (or loss) on the sale of the shares when the options are exercised. (Example 4) | The proceeds from the sale of the options are a capital gain in the year of the sale, but the capital gain is cancelled on the exercise date (if the gain was reported on a previous year's tax return, that year's return should be amended). The proceeds from the sale of the options are added to the proceeds from the shares to determine the capital gain on the sale of the shares when the options are exercised. (Example 7) | The proceeds from the sale of the options are a capital gain in the year of the sale, but the capital gain is cancelled on the exercise date (if the gain was reported on a previous year's tax return, that year's return should be amended). The cost of the shares, less the proceeds from the sale of the options, is added to the ACB of the underlying security when the options are exercised. (Example 8) |

In all cases brokerage fees should be deducted from proceeds or added to costs.

In the case of selling call or put options where the options are exercised, the proceeds from the options sale are initially treated as a capital gain in the year of the sale. But when the options are exercised, that capital gain is canceled. If the options are exercised in a subsequent tax year, this will necessitate filing an amendment on the previous year’s tax return. The extra paperwork required may be a motivation for some to avoid selling options that expire in a future year.

Referring to the table, there are a total of 8 different tax treatment scenarios for all the different combinations of opening and closing options transactions. Let’s look at an example for each case.

Some background information on the possible opening transactions:

- Buy Call Options: Buying the right to purchase shares of the underlying security

- Buy Put Options: Buying the right to sell shares of the underlying security

- Sell Call Options: Selling the right to purchase shares of the underlying security

- Sell Put Options: Selling the right to sell shares of the underlying security

The possible closing transactions:

- Options Expire: The expiry date of the options passes and the holder of the options (the buyer) did not choose to exercise them.

- Options are Closed: An offsetting position is bought or sold to close the options before the expiry date. For example, a seller of put options buys back the same put options to close the transaction. Or, a buyer of call options sells the same call options to close the transaction.

- Options are Exercised: The holder of the options (the buyer) chooses to exercise them before the expiry date.

Example 1: Buy Call or Put Options / Options Expire

- Buy call (or put) options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $1,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- The options expire on January 15, 2016 without being exercised or sold to close

The ACB of the options is $1,020 (the total amount of $1,000 plus the commission of $20). When the options expire it’s as if they were sold for $0 since they expire worthless. This results in a capital loss of $1,020 on January 15, 2016.

Example 2: Buy Call or Put Options / Options are Closed

- Buy call (or put) options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $1,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- The options are sold for a total price of $1,500 and a commission of $20 on October 8, 2015

The ACB of the options is $1,020 (the total amount of $1,000 plus the commission of $20). When the options are sold the total proceeds are $1,480 ($1,500 – $20). A capital gain of $460 ($1,480 – $1,020) is realized on October 8, 2015.

Example 3: Buy Call Options / Options are Exercised

- Buy call options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $1,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- Exercise the options on January 14, 2016 with a commission of $20

The ACB of the options is $1,020 (the total amount of $1,000 plus the commission of $20). On January 14, 2016 100 shares of Microsoft (MSFT) are acquired for a cost of $10,000 (100 shares multiplied by the strike price of $100/share) plus a commission of $20. The ACB of the Microsoft (MSFT) shares becomes $11,040 ($1,020 + $10,000 + $20). No capital gain or loss is reported on the options.

Example 4: Buy Put Options / Options are Exercised

- Buy put options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $1,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- Buy 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $12,000 plus a commission of $20 (you’ll need to own the underlying shares when exercising the put options because you’ll be required to sell the underlying shares)

- Exercise the options on January 14, 2016 with a commission of $20

The ACB of the options is $1,020 (the total amount of $1,000 plus the commission of $20). The ACB of the underlying Microsoft (MSFT) shares is $12,020 ($12,000 + $20). When the options are exercised on January 14, 2016, the cost of the options is subtracted from the proceeds to determine the capital gain (or loss). The capital loss resulting from the sale of the shares/exercising of the options is $3,060 ($10,000 – $20 – $1,020 – $12,020) on January 14, 2016.

Example 5: Sell Call or Put Options / Options Expire

- Sell call (or put) options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $1,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- The options expire on January 15, 2016 without being exercised or sold to close

A capital gain of $980 ($1,000 – $20) is realized on April 13, 2015. When the options expire, no further gains or losses are realized.

Example 6: Sell Call or Put Options / Options are Closed

- Sell call (or put) options for 100 shares of Microsoft (MSFT) on April 13, 2015 with total proceeds of $1,000 and a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- The same options are bought back for a total price of $1,500 and a commission of $20 on January 7, 2016

A capital gain of $980 ($1,000 – $20) is realized on April 13, 2015. A capital loss of $1,520 ($1,500 + $20) is realized on January 7, 2016.

Example 7: Sell Call Options / Options are Exercised

- Buy 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $12,000 plus a commission of $20 (you need to own the underlying shares because exercising the call options will require you to sell the underlying shares – this type of transaction is referred to as selling covered call options)

- Sell call options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $3,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- The options are exercised on January 14, 2016 with a commission of $20

The ACB of the underlying Microsoft (MSFT) shares is $12,020 ($12,000 + $20). A capital gain of $2,980 ($3,000 – $20) is realized on April 13, 2015 from the sale of the call options. This gain must be reported for the 2015 tax year. When the options are exercised on January 14, 2016 the underlying shares are sold for $100 per share. Also, the $2,980 capital gain is retroactively canceled and the 2015 tax return must be amended. A capital gain of $940 ($10,000 – $20 + $2,980 – $12,020) is realized on the sale of the underlying shares.

Example 8: Sell Put Options / Options are Exercised

- Sell put options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $3,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- The options are exercised on January 14, 2016 with a commission of $20

A capital gain of $2,980 ($3,000 – $20) is realized on the sale of the options on April 13, 2015, which must be reported in the 2015 tax year. When the options are exercised on January 14, 2016 the $2,980 capital gain is retroactively canceled and the 2015 tax return must be amended. The shares are acquired for a cost of $10,020 (100 shares multiplied by the $100 strike price, plus the $20 commission). The net cost of the options of $2,980 is subtracted from the acquisition cost to determine that the ACB of the Microsoft (MSFT) shares is $7,040 ($10,020 – $2,980).

Calculating Capital Gains and ACB with Stock Options on AdjustedCostBase.ca

AdjustedCostBase.ca is a free tool that allows Canadian investors to calculate ACB and capital gains. It includes support for stock option transactions on capital account. This can save stock option investors from the great time and aggravation that results from manually performing these kinds of complex calculations.

On AdjustedCostBase.ca, options are associated with their underlying security. This means that when adding an options transaction, the underlying security should be selected. You should not create a separate security for each type of options. For example, if you buy call options for Microsoft (MSFT) then the transaction should be added for the “Microsoft (MSFT)” security. You should not create a separate security for these particular options.

Both the opening and closing transactions are entered jointly, meaning that you don’t need to create a second transaction for the closing portion of the options transaction. If the options transaction has not yet been closed (i.e., it has not expired, been exercised, or bought/sold to close) then the status can be set to open and you’ll be able to edit the transaction at a later date to incorporate the closing status.

If the options are closed in multiple ways (for example some options expire while the others are bought/sold to close, or options are bought/sold to close at separate times) then you can deal with this by splitting it into multiple transactions. For example, if you buy call options for 200 shares and sell 100 options while the remaining 100 expire, you can add two opening options transactions for 100 shares each, while setting the closing portions of the transactions accordingly.

Let’s look at using AdjustedCostBase.ca for a couple of the examples from above.

Example 1 on AdjustedCostBase.ca: Buy Call or Put Options / Options Expire

- Buy call (or put) options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $1,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- The options expire on January 15, 2016 without being exercised or sold to close

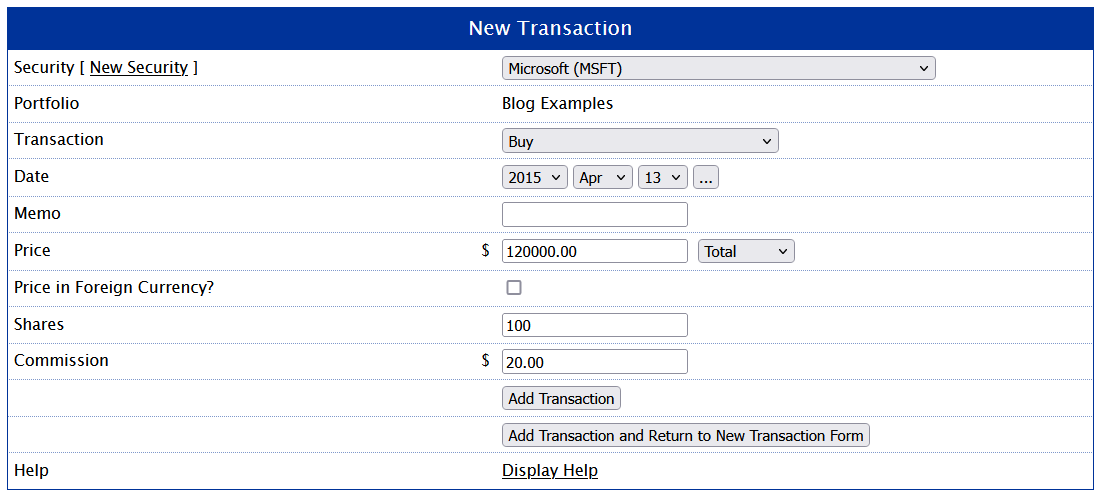

First, add Microsoft (MSFT) as a security in your account. Next add a new transaction. Set the security name to “Microsoft (MSFT)” and the transaction type to “Buy Call Options (to Open).”

For the number of shares enter 100. Note that options are often sold in groups of 100 shares and 1 option can sometimes refer to an option to buy/sell 100 shares. On AdjustedCostBase.ca the number of shares associated with an options transaction refers to the actual number of shares associated with the options, not the number of blocks of 100.

Next set the date to April 13, 2015, the total price to $1,000, the strike price to $100 and the commission to $20. Set the “Options Status” to “Open” (let’s assume that we’re entering the transaction on the purchase date and we don’t yet know what the closing transaction will be).

The form should appear as follows:

![]()

After adding the transaction you’ll see it listed as follows:

As expected, there is no capital gain or loss just yet. Once the options expire, click on “Edit” to update the status of the options transaction. Set the “Options Status” to “Closed: Options Expired” and set the closing date to January 15, 2016:

![]()

Note that you do not add a new transaction for the closing transaction portion. The opening and closing transactions are joined together in a single transaction. After editing the transaction, you’ll see a capital loss on the closing date of $1,020, consistent with the example above:

Example 7 on AdjustedCostBase.ca: Sell Call Options / Options are Exercised

- Buy 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $12,000 plus a commission of $20 (you need to own the underlying shares because exercising the call options will require you to sell the underlying shares – this type of transaction is referred to as selling covered call options)

- Sell call options for 100 shares of Microsoft (MSFT) on April 13, 2015 for a total amount of $3,000 with a commission of $20, a strike price of $100 and an expiry date of January 15, 2016

- The options are exercised on January 14, 2016 with a commission of $20

First, add Microsoft (MSFT) as a security in your account if it doesn’t yet exist. Next add a new transaction for the purchase of 100 shares of Microsoft (MSFT) as follows:

After adding the transaction you should see a total ACB for Microsoft (MSFT) of $12,020:

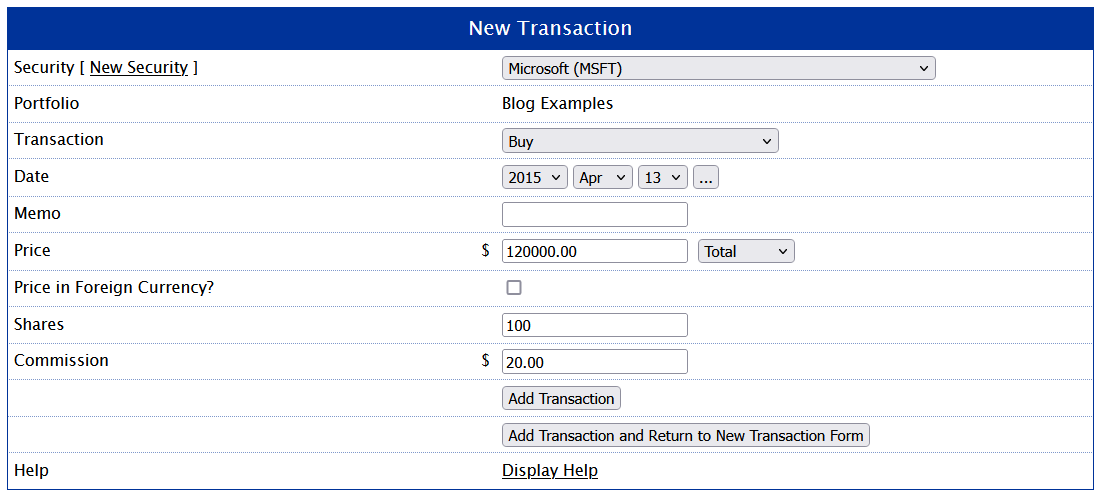

Now add a new transaction for selling the covered call options. Set the transaction type to “Sell Call Options (to Open)”, the date to April 13, 2015, the price to a total amount of $3,000, the number of shares to 100 (since options on 100 shares are being sold), the strike price to $100, and the commission to $20. Leave the “Options Status” field set to “Open” since at the time of selling the options you won’t know how the options will be closed. The form should look as follows:

![]()

After adding the transaction you should see the following list of transactions:

Note that there is a capital gain of $2,980 on April 13, 2015.

Now we’ll set the status of the options transaction to reflect the options being exercised. Click on the “Edit” link for the “Sell Call Options (to Open)” transaction. Set the “Options Status” field to “Closed: Options Exercised”, the closing date to January 15, 2016, and the closing commission to $20 as follows:

![]()

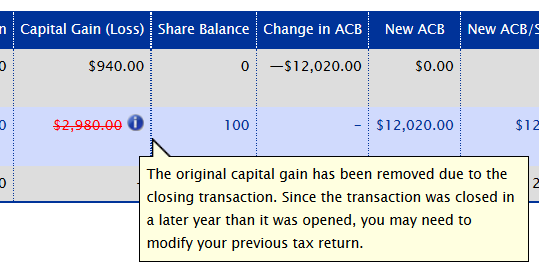

After editing the transaction, you’ll see the following list of transactions for Microsoft (MSFT):

The closing portion of the options transaction shows a capital gain of $940 on January 15, 2016, which is consistent with the original example from above. Also, note that the original capital gain of $2,980 on April 13, 2015 has been crossed off, indicating that it’s been canceled. Hovering over the information box, you’ll see the following explanation:

Thank you for this great site. I believe there is a small error in the last sentence of Example 6….

“A capital loss of $1,480 ($1,500 – $20) is realized on January 7, 2016.”

should read…

“A capital loss of $1,520 ($1,500 + $20) is realized on January 7, 2016.”

Adding (as opposed to subtracting) the commission cost when buying back the options.

Marc,

Thanks for letting me know about the error. I’ve corrected this.

Thank you for the amazing software.

I can’t find any way of managing foreign currency (USD) options transactions in the same way as regular long and short stock transactions?

Am I missing something?

If not would you consider adding this?

Thank you again,

Neil

Neil,

There’s currently no way to enter foreign currency on AdjustedCostBase.ca for stock option transactions in the same way you can for buy and sell transactions. Thanks for your suggestion – this may be added in the future.

For now you’ll need to convert all values into Canadian dollars yourself, including the opening and closing prices and opening and closing commissions. In particular, in cases where the options are exercised, you’ll need to go back and convert the strike price into Canadian dollars based on the exchange rate at the time the options are exercised since the strike price is used for calculating ACB and capital gains (this is not necessary if the options are sold or expire).

Thank you for the kind and detailed response. I will use this method for now.

I hope others request this addition too!

Hi: I’m not sure if this is the correct forum for my comment. I am just starting/learning how to enter transactions. It does not appear as though the edit feature for option transactions allows you to go back and change the entry to a foreign currency transaction. It seems as though if you miss that feature on initial entry (as I have done on several occasions), and your transaction is indeed in a foreign currency, you need to delete the transaction and start again. Is that correct? Thanks

My mistake. I overlooked the fact that there is no feature coverts option transactions to foreign currency amounts. Sorry

I noticed that someone in the thread has already suggested if you can add a feature on AdjustedCostBase.ca for stock option transactions in foreign currency. I would like to know if this feature is coming soon, if not, would you kindly consider?

Thanks!

I do quite a bit of option trading in foreign currency, and adding a feature for it would be a great addition to your website. Will a feature like this be made available soon? Thank you

Hi, in your first example, if a person had bought the option using foreign currency, would the capital loss be based on the expiry date exchange rate or when the option was purchased?

Andy,

The exchange rate would be the one on the settlement date for the purchase of the options.

Hello, for tax claim purposes, does superficial loss apply to option trading. For example, if I purchase a call option and it expires after 10 days, is it considered a superficial loss because it expired within 30 days of the purchase? Does the same apply if I close the position, or if I exercise the option?

Also, if I purchase a call option and then sell the underlying stock at a loss within 30 days, I believe it is considered a superficial loss. But if I exercise the option at a time beyond the 30 days, does it affect the sale of the shares such that the loss can be claimed?

Rishi,

The expiry of an option will not trigger a superficial loss:

http://www.cra-arc.gc.ca/tx/ndvdls/tpcs/ncm-tx/rtrn/cmpltng/rprtng-ncm/lns101-170/127/lss-ddct/sprfcl/nt-eng.html

“In certain situations, when you dispose of capital property, the loss may not be considered a superficial loss. Some of the more common situations include the following…The disposition results from the expiry of an option.”

I would assume that closing or exercising options could trigger the superficial loss rule as these scenarios are not listed above.

If you exercise a call option more than 30 days after selling the underlying shares then the superficial loss rule would not be triggered, assuming no other transactions took place, since there is no disposition within the superficial loss period.

“The CRA generally considers options trading to be on the same account as transactions for shares. Selling of naked call options is generally considered to be on income account, but the CRA will allow this to be considered on capital account provided that this is done consistently from year to year.”

I’m not sure I understand this. How do I determine if I record the sale of a naked call as income or capital? So long as I always record it as capital, then it’s allowed?

What about in the case of a vertical call spread? If one leg is buying a call, and the other leg is selling a call at a higher strike price, then is one leg recorded as capital and while the other leg is income?

The aforementioned quotation seems somewhat ambiguous, so I’d love any insight you have on this. Thanks!

Sev,

The CRA does not seem to have any more specific objective metrics they use to determine whether investment income should be reported on income account or capital account.

They’ve published some general guidelines in IT-479R in section 11:

http://www.cra-arc.gc.ca/E/pub/tp/it479r/it479r-e.html

“Some of the factors to be considered in ascertaining whether the taxpayer’s course of conduct indicates the carrying on of a business are as follows:

(a) frequency of transactions – a history of extensive buying and selling of securities or of a quick turnover of properties,

(b) period of ownership – securities are usually owned only for a short period of time,

(c) knowledge of securities markets – the taxpayer has some knowledge of or experience in the securities markets,

(d) security transactions form a part of a taxpayer’s ordinary business,

(e) time spent – a substantial part of the taxpayer’s time is spent studying the securities markets and investigating potential purchases,

(f) financing – security purchases are financed primarily on margin or by some other form of debt,

(g) advertising – the taxpayer has advertised or otherwise made it known that he is willing to purchase securities, and

(h) in the case of shares, their nature – normally speculative in nature or of a non-dividend type.”

Hello,

What happens when there are multiple option trades involve in one single trade like below:

On Oct 31, 2017 I sold an Iron Condor in the SPY ETF using the 15-Dec-17 expiry cycle. The Iron Condor components were:

Sold 248 Put and 267 Call. Bought 233 Put and 277 Call.

The Credit received was $102 USD. Commission fees were $5 USD and US taxes $0.02 USD.

On Nov 20, 2017 the position was fully closed by doing the opposite trade:

Buy 248 Put and 267 Call. Sell 233 Put and 277 Call. The Debit paid was $51 USD. Commission fees were $5 USD and US taxes was $0.02 USD.

Total Profit was $102-$51 = $51 – $10 commission fee – $0.04 US taxes = $40.96 USD.

Since the buy/sell orders for the calls/puts are being on done on the same day, can the selling price of $102 credit minus $5.02 in fees = $96.98 be converted to CAD and then the buying price of $56.02 ($51 + $5.02 in fees) be converted to CAD also to calculate the profit in CAD for tax purposes or does each component have to broken out separately and converted to CAD on each date, one by one?

233 Put:

Oct 31, 17 – Bought for $44.10 including fees. Nov 20, 17 – Sold for $16.02 including fees.

248 Put:

Oct 31, 17 – Sold $125.70 including fees. Nov 20, 17 – Bought for $64.51 including fees.

etc….

Since CRA permits you to use the exchange rate from the day of the transaction date, or the average annual exchange rate if multiple transactions occurred over the course of a year, if you use the average annual exchange rate, you can just total up all the various legs of the option and then convert everything to CAD instead of breaking it up individually and it also saves you a lot of time!

Thus in my example SPY Iron Condor – $51 profit – $10 Commission – $0.04 US tax = $40.96 USD and using the 2017 BoC average exchange rate gets you $53.19 CAD.

Rahim,

Yes, I believe that can be true, but only if the position is fully closed both at the beginning and end of the year.

Rahim,

ACB for options strategies involving multiple legs can be calculated as if each leg were a separate transaction. In special cases where the options positions are fully closed at the beginning and end of the year, it should be possible to sum up the cash flows to calculate the capital gain or loss. And in such cases with foreign currency, the capital gain or loss can first be calculated in the foreign currency and then converted into Canadian dollars, provided that an average annual exchange rate is used. However, if the position spans multiple years, then the calculations will be more complex.

Hello,

Yes, the various option positions were opened in 2017 and fully closed in 2017. Using the Bank of Canada average annual exchange rate makes the calculations a lot simpler since you can total the multiple legs up for each option trade and then convert it to CAD using average annual exchange rate 🙂 Using the daily exchange rate for each trade and each separate options leg would take hours and hours and not worth the headache!

Thanks, RK

For buying to close options that were initially sold to open (Example 6), is it correct that this would never result in a superficial loss, since it’s not a disposition that triggers the capital loss?

Egon,

When selling options to open, you incur an immediate capital gain and then claim a loss when the options are bought back. The intention of the superficial loss rule is to prevent taxpayers from claiming capital losses too early (in most common scenarios the application of the superficial loss rule does not reduce lifetime capital losses, but rather defers losses into the future).

The rules for selling options to open already result in an immediate capital gain and deferred capital loss, so I don’t think the superficial loss rule would generally apply in most situations. If you bought back and resold options in quick succession, the capital loss would likely nearly cancel out the capital gain anyways.

Hi, I am confused by your last paragraph in your June 12 2017 response. Maybe I don’t really understand that person’s question. My understanding of the example is:

-a person already has shares, then buys a call option

-then sells the shares at loss within 30 days of his option purchase

-keeps his call options after 30 days of the sale

Wouldn’t that mean his sale is a superficial loss since he still has the right to purchase the shares?

I have a question on whether this scenario would have a superficial loss:

-buy shares. 5 days later buys call option of that stock.

-a few days later closes the option at a loss.

-after 30 days still holds those shares.

Thanks

Andy,

In that scenario I don’t believe that the superficial loss rule would be triggered. The first condition of the superficial loss rule is:

“During the period that begins 30 days before and ends 30 days after the disposition, the taxpayer or a person affiliated with the taxpayer acquires a property (in this definition referred to as the “substituted property”) that is, or is identical to, the particular property.”

In the situation you’ve described, although call options are acquired within the superficial loss period, but the underlying shares are not. Call options are not identical to the underlying shares. Options (the rights to acquire the underlying shares) are only mentioned in the second condition of the superficial loss rule:

“At the end of that period, the taxpayer or a person affiliated with the taxpayer owns or had a right to acquire the substituted property.”

I don’t believe the superficial loss rule applies in the second scenario you mentioned either.

Thanks, I think I get it now. I had presumed that call options and shares were the same, but I realize now they are not identical.

Hello,

If my employer offered me 1000 options at strike price of $5, and then later that year it was exercised and sold at $15.

How do I fill out the transaction form? Would this be a buy call options to open with the status of closed: sold?

Thanks,

Mia

Mia,

The tax treatment of employee stock options may vary depending on the case, but in general I would suggest using a “Buy” transaction on the date the options were exercised. The amount for this transaction should be equal to the total of the following:

1. The cost paid for the options (if any)

2. The exercise price of the shares

3. The taxable benefit

Assuming that you didn’t pay anything for the options and that the fair market value at the time of exercise was $8 per share, then you would pay $5 per share and would likely see a taxable benefit of $3 per share ($8 – $5). This could be inputted into AdjustedCostBase.ca as follows:

1. Buy shares for $8 per share ($5 exercise price + $3 taxable benefit).

2. Sell shares for $15 per share.

Hi

Is it possible to import option trades from a spreadsheet? Testing the import tool seems to indicate that it will work but each option will be added as a unique security. This may still work for my purpose since none of my option trades have been exercised. I hold the underlying security on some of the options being traded.

Thanks

Brad,

Importing transactions involving options from a spreadsheet is not supported. However, if all transactions involve buying options (calls or puts) to open and the options either expire or are sold to close, then the tax treatment should be equivalent to transactions involving shares.

In the case of options being sold to close, the capital gain/loss is equal to the proceeds of disposition less the cost, with the gain/loss being recorded at the time of the sale. In the case of options expiring, the proceeds of disposition are zero, with the loss being equal to the cost of the options.

How do you adjust a call options if the company went through a

‘Split”? For example I buy to open a call last month and the company had a 5:1 split? Do I just go back and edit the original entry?

Charlemagne,

If a company incurs a stock split between the times of your opening and closing options transactions, this will be accounted for by AdjustedCostBase.ca. You will, however, need to input a split transaction as described here:

https://www.adjustedcostbase.ca/blog/the-effect-of-stock-splits-on-adjusted-cost-base/

In the case where you’ve bought call options to open and the company subsequently incurs a 5-for-1 split:

– If you sell the options to close and input the amount as a per share value, it should be inputted based on the post-split price.

– If you exercise the options, then the amount of shares received will automatically be adjusted based on the split ratio. For example, if you bought options on 100 shares right before a 5-for-1 split, then you’ll receive 500 shares upon exercising them.

Hello,

Would the superficial rule apply for this situation?

-bought a call option on a stock and then closed it at a loss.

-then a week later bought call option on the same stock but with a different strike price and expiry date, and held this option for a few months.

I don’t know if there would be superficial loss. Thanks.

Andy,

I don’t believe the superficial loss rule would apply in that situation.

In Example 5 or 6,

Do I need to report the premium I got RIGHT AWAY in taxation year 2015 for CRA?

If that is the case, It does not matter I will close the position in year 2016 or let it expire at that time.

If that is the case, it is not good to hand onto long term naked put option as I will incur much larger capital gain right away.

Victor,

Yes, premiums you receive from selling call or put options on capital account are taxable as capital gains in the year the options are sold (2015 in these examples).

I understand I have to report the premium for taxation year 2015.

The question is do I have to report this premium when I file the tax return for 2015, OR I need to wait until I file tax return for 2016 to make adjustment at that time.

Victor,

The capital gains in examples 5 and 6 would be reportable in your 2015 tax return.

Neither of these examples involve an adjustment. In the case where an adjustment is required (for example, options are sold and then exercised in a subsequent tax year) then you would still report the gain in the year the options are sold. In the next year you would need to file an amendment to the previous year’s return to remove the gain.

Hello,

This is my first year doing taxes on my option activity (mostly writing put/call options with various multi-leg strategies), with some stock assignment/exercise in 2020 (Started July 2020, and leading into this year).

Based on the article and the various comment clarifications:

1) Income vs Capital Account

“The CRA generally considers options trading to be on the same account as transactions for shares. Selling of naked call options is generally considered to be on income account, but the CRA will allow this to be considered on capital account provided that this is done consistently from year to year.”

I have a full-time job and the option gain/losses are not as substantial, and would want to book as capital gain/losses in the first year in order to consistently do so in the following years. Provided I follow this above clause and report as capital gain/loss for 2020 and beyond, do you know of any reported anecdotes associated with this?

What does IBKR/Brokerages report to the CRA – is it just the T5008?

2) Net P&L Calculations across Option Scenarios

Per Rahim (one of your commenters from 2018), “the average annual USDCAD exchange rate can be used after summing everything up in USD for the multiple option leg positions”, which does simplify the calculations. Does this apply to to all option activity?

For filling in the capital gains/losses as part of the return ala T5008, for all the option activity, is there a need to report by security? Or can it all be lumped together as a net gain/loss for all option activity across multiple legs across multiple securities?

Assuming this batch of transactions are closed or expired (without assignment/exercises) and resolved within the the same year 2020

a) Batch 1 – Option Activity across multiple securities opened and closed/expired in 2020

– Calculate Net P&L Gain and Losses including Commissions in Non-Base Currencies (USD) – Apply 2020 Annual Average USDCAD Rate

USDCAD = 1.3415 (per https://www.bankofcanada.ca/rates/exchange/annual-average-exchange-rates/)

– Can this be reported as one line (or per Security per Box 21? It is expected that per security basis is reported?)?

b) Batch 2 – Option Activity left unresolved in 2020 until later years

– Option Written – Capital gain in 2020 – Can this follow the USD/CAD Rate for 2020?, if it was Bought back in 2021, would that use the 2021 Average USDCAD Rate?

– Option Buy – Nothing booked in 2020 until it is Closed later on – say 2021 – for a gain or loss – Can this use the 2021 Average USDCAD Rate?

Can the Option Written Capital Gain for 2020 just be lumped into Batch 1?

c) Batch 3 – Options that are exercised or assigned in 2020

– ACB of the underlying stock needs to be determined and when the stock is either sold or called away via options

– Can Annual Average Rate be used in this case or should exchange rates as of the transaction dates for the option write and the stock exercise be utilized?

Per https://turbotax.intuit.ca/tips/t5008-slip-statement-of-securities-transactions-10957,

Box 14: The date your securities transactions occurred, December 31 if you are submitting multiple transactions.

Box 16: The quantity of security you disposed of.

Box 17: The description of the security, if multiple these may be in Box 21.

Box 20: The cost or book value. This is not necessarily your adjusted cost base (ACB), which you are responsible for calculating (although your broker or advisor be able to advise you of this amount). If your broker leaves this box blank, you must still calculate it and report it.

Box 21: If you’d like to report on a per security basis you could use this section to detail the amount you received from each security.

If you are using information from your T5008 in your tax return, you should note that you need to include the amount in Canadian dollars. Therefore, if there is an exchange rate listed in Box 13 of your T5008, you need to use it to calculate the Canadian dollars you need to report.

3) Alternatively, instead of using an average exchange rate, there may be a difference (advantage / disadvantage) compared to using the actual USDCAD rate at the time of transaction

– is it applicable to use the conversion done by IBKR which is recorded on every transaction as of the transaction date?

– what’s a good way to gauge which way is more advantageous – or will it require to calculate the detailed per transaction CAD-equivalent amounts (which in IBKR, the transactions are reported in base currency using the FX rate application as of the transaction date/time)?

– i.e. average USDCAD exchange rate is higher than the transaction date rates such that a net gain in CAD would be higher using the average rate versus the transaction rates – advantage to use the individual transaction rates (conversely, losses are more advantageous with the USDCAD exchange rate)

4) T5008 Brokerage Reports and Admendments

Per https://turbotax.intuit.ca/tips/t5008-slip-statement-of-securities-transactions-10957,

“If you are using information from your T5008 in your tax return, you should note that you need to include the amount in Canadian dollars. Therefore, if there is an exchange rate listed in Box 13 of your T5008, you need to use it to calculate the Canadian dollars you need to report.

If you notice that there was an error on your T5008 slips later you can have them amended and correct the error with the Canada Revenue Agency (CRA).”

I am using IBKR and I believe based on your previous articles IBKR T5008 have changed over the years (switch away from FIFO? And uses an average base cost?).

Is it normal for Tax Return to be different from the IBKR T5008 submission? Should there be anything done to submit any amendments?

Thank you in advance

Based on the various option tax treatment scenarios, is it a correct understanding that using options in most scenarios and avoiding assignment is a bit simpler in the sense that you don’t need to consider ACB calculation of stock holdings (since no underlying is acquired)?

This would suggest writing options and buying long-dated options like LEAPS can just be handled as per above?

Thoughts?

Appreciate your post.

If you buy a call spread that expires in following year, how is it reported for tax purposes.

See example

15-Dec-20 BUY 1 TO OPEN JPM 19-Feb-21 120 CALL 7.12 5.25 debit

15-Dec-20 SELL -1 TO OPEN JPM 19-Feb-21 135 CALL 1.87

In this example bought a spread in Dec which expires in Feb of the next year. My T5008 has only the leg that was sold in 2020. Do we include the leg that was bought $7.12 in cost basis ? This results in a debit of $5.25 or do we include that leg when the option position is closed.

Appreciate your help

Thanks

B

Can the AdjustedCostBase.ca app be used with an income account (margin account)? I have made many strategy trades (Vertical Call & Vertical Put) of less than 30 days and I was wondering if there was an app that work for me.

Thank you for any help.

Keith,

AdjustedCostBase.ca is intended for calculating gains on capital account only, and cannot be used for transactions on income account.

That is to bad, I am sorry to hear that.

Do you have any plans to produce an app in the future that can be used on an income account? I am quite sure that there are more people out there like me that could use an app of that nature and would be willing to pay for it.

Is anyone aware of an app of this nature that is available now? I had over 250 option Put & Call strategy trades last year and it sure would be nice to have an app to help keep track of them.

Again, thank you for any help.

Keith

I am trying to understand Example 7, specially bullet point 2 “Sell call options for 100 shares of OPT on April 13, 2015 for a total cost of $3,000”. Where does the $3000 come from or how do I calculate this value? After I purchased a covered call, I have the premium, strike price, and commission, but where is the “total cost” for an option?

Thanks for your help.

Charlie,

The $3,000 is the amount that the options were sold for (i.e., the market price of the options). The phrasing has been updated and hopefully it’s a little clearer now.

So the $3000 is the total amount of premium received? For example, as the seller of a covered call, the Bid is $30 (30 * 100 = $3000)?

Charlie,

Yes, that’s correct.

I know others have asked about whether we can use ACB.ca for income accounts and you replied it’s for capital but from my understanding it seems the process in calculating gains and losses are the same but the rates which they are taxed are the only difference. Could you maybe enlighten me on any differences in calculating income for income accounts that wouldn’t be used in capital accounts or vice versa?

I’ve read through the post and comments, but I think I need some clarification on a Vertical spread I recently entered.

I entered the spread into ACB as 4 separate transactions and now there’s an alert about the naked sale of call options. Is it OK to calculate the trade combining the spread entry STO and BTO total as the open transaction and the spread exit BTC and STC as the closing transaction (see trade details below)?

Would this avoid the naked call alert or does it matter, and will CRA need the breakdown of legs?

Thanks for your help in advance!

Jeremy

Sold a $182.50 strike call for $1.38 and bought a $187.50 strike call for $0.25 (total credit $1.13), then bought the $182.50 for $1.35 and sold the $187.50 for $0.09 (total debit $1.26).

Hi AdjustedCostBase,

On the Calculating Adjusted Cost Base when Purchasing Foreign Currency Securities blog you wrote:

“April 21, 2015 at 3:03 pm

Bunmi,

I can’t find any information that confirms the CRA’s stance on this, but it makes more sense to me to to use the exchange rate on the purchase/trade date as opposed to the settlement date. …”

Then in a comment above you wrote:

“April 27, 2017 at 4:56 pm

Andy,

The exchange rate would be the one on the settlement date for the purchase of the options.”

Does this mean exchange rate to use for stocks is T+0 and for options is T+2? Or did you obtain new information confirming CRA’s stance is T+2 for stocks and options?

Thank you for this wonderful site,

Ben

Ben,

I don’t see any reason to use a different choice between trade date and settlement date for options vs. stocks.

The only known documentation I know about on the subject of using an exchange rate on the settlement vs. trade date can be found here:

https://taxinterpretations.com/cra/severed-letters/2015-0588981c6

“Should the exchange rate in effect on the transaction date or the settlement date be used in respect of transactions on capital account carried out on a foreign exchange, such as the New York Stock Exchange?

…

Thus, in the example of a taxpayer receiving proceeds of disposition of the sale of a security on the New York exchange in an American dollar account, the conversion to Canadian dollars must be made at the noon rate quoted by the Bank of Canada for the settlement date for the transaction.”

This suggests using the exchange rate on the settlement date. However, I take this roundtable document with a grain of salt. It’s a transcription of a verbal statement made by a single CRA employee at a conference and isn’t even published on the CRA’s web site nor is it officially available in English. Much of the content either isn’t backed up by documentation on the CRA’s web site, and I have seen similar documents that contradict the CRA’s web site. In any case, I would suggest choosing one method and sticking with it.

I frequently purchase options by starting a small position then building it by averaging down over several days or weeks. These will be same strike price and expiry. How would I input these transactions so that they reflect an accurate ACB? Also is there a special treatment for diagonals? Thanks!

Perhaps as an extension to what Henry asked on Feb 1: how should I enter it when I sell options on a stock (all at once, unlike Henry), and then buy back to close only a portion of the options, letting the rest expire (or potentially having the rest get exercised)?

Andrew,

In cases where options are closed in multiple ways, you can split the opening transaction into multiple transactions on AdjustedCostBase.ca.

Hello,

I have a couple of Options questions, the second of which is making my head spin.

1) I’m wondering why there’s no ACB shown for my Option entries (see below–hopefully the formatting worked)? I only buy or sell Calls and Puts, either buying Calls or Puts, or Vertical Spreads. I always separate the vertical spreads into two entries, for example, one for the Sell Call open/close and the other for the Buy Call open/close. None of the entries in my ACB report have an ACB.

2) My head has been spinning trying to figure out the ACB P&L to compare to my T5008’s Cost or Book Value and Proceeds of Disposition. As it relates to the T5008, what would be the Cost or Book Value and what would be the Proceeds of Disposition, and is my combined ACB & P&L for the 182.50 Call (-$25.77) and for the 187.50 Call (-$19.70)?

ACB report,

Nov 12 | Call Sold 187.50 | $ 11.30 | 100 Opt. | $0.11 | $ 1.26 | ($22.20| 0| -| $0.00| -|

Nov 12 | Call Bought 182.50 | $169.60 | 100 Opt. | $1.70 | $13.76 | ($183.36)| 0| -| $0.00| -|

Nov 2 | Buy Call 187.50 | $ 31.00 | 100 Opt. | $0.31 | $ 1.24 | -| 0| -| $0.00| -|

Nov 2 | Sell Call 182.50 | $171.17 | 100 Opt. | $1.71 | $13.58 | $157.59| 0| -| $0.00| -|

T5008

Box 17 Box 20 Box 21

Nov 2 | Call 182.50 | $181.04 | $157.58

Nov 12 | Call 187.50 | $ 26.00 | $ 7.99

Thanks for your help!

Jeremy

Given all scenarios and where SPX options are cash settled, how are they treated under Canadian taxation ?

Jeremy,

Options transactions on AdjustedCostBase.ca should be inputted with the security set to the underlying shares. In other words if you sell call options for BMO then you should add a “Sell Call Options (to Open)” transaction for BMO, rather than creating an separate security for BMO options. Buying or selling options does not impact your ACB of the underlying shares, and therefore no change in ACB is shown in these cases. When options are exercised the ACB of the underlying shares does change, and this will be reflected in the data.

If you sell options to open with net proceeds of $157.59 and later buy them back for $183.36 then you will incur a capital gain of $157.59 followed by a capital loss of $183.36, or a net loss between the two segments of $25.77.

If you buy options to open for a total of $32.24 ($31.00 + $1.24 commission) and sell with net proceeds of $10.04 ($11.30 – $1.26 commission) then the capital loss will be $22.20 ($10.04 – $32.24).

I’m not sure exactly why these values don’t match what is reported on your T5008 slips but assuming you’ve inputted the data correctly there can be many reasons:

https://www.adjustedcostbase.ca/blog/can-you-rely-on-your-brokerage-for-calculating-adjusted-cost-base-and-capital-gains/

Thanks for this info. and clarification. The arithmetic for selling options (same with short positions), for whatever reason locks up my brain, similar a double negative in a sentence. Anyway …

I’ve been entering all my options trades under the name ‘Options’, as it says here: https://www.adjustedcostbase.ca/blog/adjusted-cost-base-and-capital-gains-for-stock-options/, and in the Memo section I include the security ticker, the option expiry and strike, and the USD to CDN exchange rate. So is it better to enter all Options trades under the actual Security, which in the example I gave was Disney (DIS) as opposed to the generic ‘Options’ security name?

Thanks again!

Jeremy,

Yes, in that case you should input the options transactions under the security Disney. I apologize for the confusion – we will update this page to be clearer. Also, in cases where the options are not exercised (i.e., they are bought/sold to close or expire) then it should not make any difference on the resulting gains/losses if you don’t use the underlying security.

Thank you for all your help! 🙂

Today I bought an option to close and sold an option to open in 1 transaction on questrade.

In your SW, I have to enter 2 separate transactions. I guess I should just split the commission I paid for the trade between the two transactions?

Thx

-Colin

Colin,

It seems reasonable to split the commission between the transactions in such cases.

Hello, can you please confirm that when options are only bought and then closed to sell or left to expire that we can import them where the option transactions are a new security and it doesn’t make a difference if we don’t use the underlying security, as it doesn’t affect the ACB of the underlying security?

Thank you very much for your responses.

Ivan,

Yes, in the case of buying options and selling to close then the capital gains should be the same regardless of whether you use an options transaction or a pair of “Buy”/”Sell” transactions. In the case of buying options and letting them expire, this is equivalent to selling for $0. In these cases there is no impact on the ACB of the underlying shares. For all other cases, however, using options transactions is necessary to achieve the correct results.

Now we’ll set the status of the options transaction to reflect the options being exercised. Click on the “Edit” link for the “Sell Call Options (to Open)” transaction. Set the “Options Status” field to “Closed: Options Expired”, the closing date to January 15, 2016, and the closing commission to $20 as follows:

In the table example for #7 example – is the part saying set the option status to Closed Options Expired a mistprint since the options are exercised? and in the acutal table it says Closed Options to Exercised.

In the exercised examples it says exercised on the last day berore expiration eg Jan 14 2016 – what is the significance of this date in each of the examples ie the one day before? (and the leaving it that late?) and is it always third party who is doing the exercising (at least one of my brokers refers to this as an assignment – so some confusion over the naming). When can the holder of the option do the exercising a) does it always have to be when the strike price ie reached or b)in some circumstances prior?

Ronaldo,

Thanks for pointing out the error. The text has been updated.

The terms of options are determined based on the exchange and/or specifics of the options. For example American-style options (typically used in North America) allow for exercise any time before the expiration date. European-stype options may only be exercised at a single point of time at the expiration date. There is no significant meaning behind the exercise dates in the examples.

Right Acb.c at anytime i can exercise the option wrt American-Style options and do not have to wait for the strike price to be reached – but if can get a better deal at market (and taking into consideration commissions and how much i paid for the option) then no reason for me to exercise, whilst my online brokers do not offer European style in any event.

As to the question about many of your examples wait to exercise on last day before expiration – the reason for this my broker explained is if i am in the money and wait to be assigned then i pay an extra $65 commission (as least at my current brokers) than if i sold it off myself online (and if i still wanted the actual stock then i can purchase it myelf online).

I will assume my comments correct unless U correct my thoughts on this of course. thks

Hi @AdjustedCostBase.ca,

Could you please help with the following situation?

Last year I bought put options on two different dates to protect my portfolio. Specifially, #5 contracts in March (-$1,000), then #15 contracts in April (-$3,500).

Then I closed partially in May, fully in June. First close was to sell #10 contracts (+$6,500), second close was to sell another #10 contracts in June (+$9,500).

These were the same contract (underlying, expiry, strike). Both sales resulted in gains/profits.

Could I combine 1st open with 1st close, and 2nd open with 2nd close? The result would be a gain of $5,500 ($6,500-$1,000) for 1st trade, and a gain of $6,000 ($9,500-$3,500) for the 2nd trade. For reporting purposes, I’ll aggregate the gains.

My concern is that since the #. contracts are different, it doesn’t count as a full close; although that’s how I’m treating it.

Could you kindly let me know if the above journaling is acceptable?

My other thought is to treat the contrac as if it’s the security itself, inserting the trades as buy/selll orders with commissions. However, if I actually held the underlying security, it would mess up the ACB.

I saw other posts about 1 open and multiple closes, however, my situation is a bit more complicated with multiple opens, as well as different sizes 🙁

Suggestion: it would be very convenient to add the functionality of allowing multiple opens and closes within the same entry ticket. Similar to how trades are aggregated and netted within the same security name.

Thanks a lot in advance for your time and help!

Regards,

Kelvin

Kelvin,

For the particular case where options are bought to open, I think there are a number of approaches you can use that would yield the same result. The simplest might be to combine everything into a single transaction, in particular a purchase of 20 contracts for $4,500, with the options sold to close for $16,000 (which would yield the same total capital gain of $11,500).

For more complex scenarios, such as the case where a portion of the options are closed in one tax year and the remainder closed in the next tax year, you might need to break up the transactions into 2 or more parts.

Example 7 some clarification

Could u please run through the transactions not from my point of view, ie the seller of the call option but from the buyer’s point of view as that should make it easier to digest?

As i see it now: if i do not already own the stock i need to buy it as it has to be covered so pay 12k.

I sell call option to open strike $100 to Buyer who pays me $2,980usd and when Buyer on Jan 15 2016 excercises (presumably because the stock price comfortably exceeds $100usd so Buyer can recoup what he originally paid and have some potential profit margin by buying the stock at a discount to the then market price when Buyer eventually sells.

Although the Capital gain is lost (and tax gets refunded upon refiling) for tax purposes I think i still have the 2980usd in my pocket? I am also paid in addition by the buyer $10,000usd? and somehow i end up with a profit of 940usd? Yes still fuzzy after reading and printing out the full Example of 7 being the 2nd example ACBc gives. thks

Ronald,

Example 7 assumes that you already own the underlying shares when selling call options. Selling of naked call options is generally considered to be on income account, but the CRA will allow this to be considered on capital account provided that this is done consistently from year to year.

The net proceeds from selling the options are a capital gain for the 2015 tax year. That capital gain, however, would be cancelled. Instead, the net proceeds from selling the options are added to the capital gain that results from selling the underlying shares upon exercise (which occurs in 2016 in the example). So you would still end up with a capital gain from the proceeds of selling the options, but it would be incorporated into the capital gain/loss from selling the underlying shares upon exercise.

Wow, an amazing software to be honest.

I am using it for the first time. I am a little confused regarding how to enter options in the tool. Why there are only 4 transaction types for the options:

Buy call options ( to open)

Sell Call options (to open)

Buy put options ( to open)

Sell put options (to open)

What about “to close” ?? I mean if I buy a call and then sell the same call, how do I enter my selling transaction. Also same with expired option? How do I enter those?

Thanks!

Ishan,

The opening and closing portions of an options transaction are inputted jointly into AdjustedCostBase.ca. When adding or editing an options transaction, you’ll see fields corresponding to the closing status. If the closing status is known at the time of adding an options transaction, you can set it immediately. Otherwise, you can edit the transaction at any point to set the closing status.

Example 2 above covers the case of buying options and selling to close. Example 1 covers the case of buying options that later expire.

I had a question about Strike Price while entering the options transactions. Why do we have to convert strike price to CAD from USD, how does it affect? I am using Total amount which is converted to the CAD and adding contracts multiple by 100 to make it shares. I am just not understanding in this case why we want the strike price. and what if my amount is in CAD but the strike price in USD?

Sorry I had to add to the above question. I bought multiple calls of the same strike price over many months as it was a LEAP. so now when I convert the strike price to CAD it is different every time for every transaction I add even if the actual strike price does not ideally change its just changing because of USD to CAD conversion. The thing is strike price does not get used to calculate the amount for buy and sell.

Ishan,

The strike price is used to calculate ACB/capital gains for the underlying shares in cases where the options are exercised. In cases where the options are sold/bought to close or expire, the strike price has no impact.

You can choose to input the strike price in either CAD$ or foreign currency. In the latter case, you’ll need to input an appropriate exchange rate for the closing transaction date.

Hi,

I just wanted to make sure I inputted everything correctly. I entered options I had received over time as (buy options – open). Then when I exercised them, I set them to “exercised”. When I exercised them, I immediately sold the stock, so I added another transaction as a normal “sell” transaction of the shares I got through the options exercise.

Does that approach make sense? And then in the T5008 I would enter the proceeds from the stock sale and the change in ACB as the book value? (and the ACB would be affected by the options exercise?)

I noticed during the options exercise / stock sell transaction that a significant amount was taken off by the brokerage for taxes. Can I consider these part of commission? Or deduct the taxes from the final “proceeds” value since the proceeds were smaller because of the taxes? I don’t see anywhere in the T5008 slip to enter those taxes and I want to make sure I’m not being taxed twice. Thanks!

Marina,

Yes, you should add an additional “Sell” transaction following the exercise of the options. The T5008 slip is not something that you as an investor would complete. Your brokerage will complete this form and remit it to you and the CRA. You report capital gains and losses on Schedule 3.

Great article. I just learned about this software, wish I knew this few years ago instead of doing it all myself.

Is my understanding of superficial loss accurate in the scenarios below?

1. Sell to Close call option or shares at a loss and repurchase another call option with 30 days (different expiration and strike) – Superficial loss triggered

2. Sell to Close call option or shares at a loss and purchase put option within 30 days (irrespective of strike or expiration) – No superficial loss triggered as put option only gives you right to sell, , not right to buy security.

3. Sell to Close call option or shares at a loss and sell to open (write) call options within 30 days (irrespective of strike or expiration) – No superficial loss triggered as selling call option only gives you obligation to sell, not right to buy security.

4. Sell to Close call option or shares at a loss and sell to open (write) put options within 30 days (irrespective of strike or expiration) – No superficial loss triggered as selling put option only gives you obligation to buy, not right to buy security. The buyer of this put option by decide to not exercise after all.

So essentially, writing call or puts, or buying puts will have no impact on superficial losses? Only buying calls and shares triggers superficial losses?

Also, I remember seeing CRA severed letters where they say 2 options with different expiry and strike may not be identical? What is the position of adjustedcostbase.ca on that?

Hello

How do you enter call options that went through a stock split (3:1) and expired out of the money (two years after) or worthless?

example I bought a 1 call option for $2000 in 2021. stock split 2022 but the call expired in 2024.

When I entered the expiration date, I end up with 3 call option but the loss is $6000 but I only paid $2000.

Charlemagne, thanks for posting this question as I had the same issue recently.

I had Call options in Direxion Daily 20+ Year Treasury Bull 3x. When I entered the reverse split (1:10) the loss amount was incorrect, so I ended up removing the split entry and the loss amount corrected, though the contract quantity was incorrect.

I’m curious what ACB support suggests.

I found the solution. Initially I have the price entered as per share. When I changed it to “total” price of the option. It maintained the correct amount and post split qty of shares when entering the date of expiration.

Charlemagne and Jeremy,

Thank you for raising the issue. We have resolved the issue and you should now be able to properly use per share amounts without having to apply any workarounds.

Thank you!!

Long time user and I appreciate this website so much.

Question: I thought I saw capital gains broken out in two periods for 2024, can’t find it again. Can you share if this update will be applied to the website for gains? Currently we are supposed to include gains in two periods, Period 1 being Jan 1 2024-June 24 2024, and Period 2; June 25 2024 – December 31st 2024.

Also, when preparing the annual capital gains report of all stocks, it does not show the proceeds, cost base, and expense, and gain (loss) broken out per ticker. Can this be improved on to streamline the report instead of having to pull each report for each ticker?

Thank you

T W,

Today the federal government announced the deferral of the capital gains inclusion rate increase from June 25, 2024 until January 1, 2026. It will be up to the next government to decide whether to reintroduce the proposed legislation or scrap it.

Therefore there will no longer any need to separate the reporting of capital gains into two periods for the 2024 tax year. As a result, the previous functionality on AdjustedCostBase.ca that displayed separate capital gains totals for before June 25 and on/after June 25 for 2024 has been disabled.

The annual reports generated on AdjustedCostBase.ca are intended to assist with completing Schedule 3. Schedule 3 does not require capital gains totals to be broken down on a per security basis, so our annual reports do not split up the data this way. As you suggested you would need to generate separate reports for each security to see the per security totals.

Hey, I bought 2 of the same stock options on different dates in 2022,

with one option sold in 2023 and one sold in 2024

for example:

2022-01-01 bought ABC 19JAN24 50C @ $1000

2022-02-01 bought ABC 19JAN24 50C @ $2000

2023-01-01 sold ABC 19JAN24 50C @ $3000

2024-02-01 sold ABC 19JAN24 50C @ $4000

It looks like the tool expects a 1:1 mapping for the open and close transactions, and doesn’t calculate the average cost basis for the option, so I’d have to choose either a capital gain of

3000-1000=2000 for 2023-01-01 and 4000-2000=2000 for 2024-02-01

or

3000-2000=1000 for 2023-01-01 and 4000-1000=3000 for 2024-02-01

both of these seem wrong, I think the correct ACB in this case would be:

(1000+2000)/2, resulting in a capital gain of 1500 in 2023 and 1500 in 2024

am I missing a setting to combine options together but sold on different dates in the transactions menu?

slight correction to my previous comment —

the end should say “resulting in a capital gain of 3000-1500 =1500 in 2023 and 4000-1500=2500 in 2024

Fairly,

As each options transaction on AdjustedCostBase.ca can only support a single closing status, you can split this case up into two separate “Buy Call Options (to Open)” transactions for 50 shares each. Then you’ll be able to set separate closing statuses for each case to represent the different sale prices.

Is there any order to follow when closing options positions?

For example, if I sell to open 2 contracts on different dates and with different prices, then I buy to close 1, and get assigned on the second.

Should I use FIFO? LIFO? Whatever works for me?

(both contracts have the same strike and expiration)

Simon,

There would be a capital loss incurred corresponding to the buyback cost of the contract that was bought to close. For the other contract, the proceeds of the sale of the other contract would be added to the proceeds of disposition of the underlying shares to determine the capital gain (in the case of a call option) or would be added to the ACB of the underlying shares (in the case of a put option).

This can be represented on AdjustedCostBase.ca by created 2 separate option sales transactions with distinct closing statuses.

I’m not sure that FIFO or LIFO is applicable here.

So, let’s imagine the following situation:

– Day 1: sell to open ABC $10 Put exp Aug 29, collect $20 premium

– Day 2: sell to open ABC $10 Put exp Aug 29, collect $10 premium

– Day 3: buy to close ABC $10 Put exp Aug 29, pay $5 premium

– Day 4: assigned ABC $10 Put exp Aug 29, pay $1000 stocks

At then end of Day 3, I have a cap gain of $25.

On Day 4, this is where things get complicated, because I can’t say which contract is exercised and which one was sold (there’s no reference on my brokerage account, it’s just a position size).

I have what looks like 3 possibilities:

– write off the $20 premium, my ACB is $9.8, cap gains $5

– write off the $10 premium, my ACB is $9.9, cap gain $15

– average the premiums for the options position (ie. $0.15/share), ACB is $9.85, cap gain $10

A few questions, if you have a moment (also, do you have a donate button? Would like to send some $ for your help)

1) I buy TD stock and TD calls. However, it seems the buying/selling of calls never affects the ACB of the TD stock. Almost like the stock and calls act independent of each other for ACB. Is this correct? I had thought the options are considered the same as the underlying stock, so that’s what’s making me 2nd guess.

2) If I buy 100 shares in a stock and pay $20 commission. If I then sell 5 shares and a month later I sell the remaining 95 shares, would I proportionally split the buy commission among these two transactions or could I put the full $20 buy commission with the initial sale of 5 shares?

3) I buy 100 shares of call options for TD bank and sell them. But, it is a superficial loss as I purchased the underlying stock 20 days later. I know I can’t claim this as a capital loss, but shouldn’t this be added the ACB somehow where I am able to take the loss in the future? (This is how it was explained to me). However, in this program the ACB of the underlying stock doesn’t seem to be affect by buying (and closing) options. I’m not quite sure where to put that superficial loss number.

^Just to add to question #3 previously. It seems your program allows me to select superficial loss of shares that are sold, but not for call options that are sold. I tried to write the superficial loss for options as if they were regular shares, but it messes up the calculations as it used the ACB for the cost, rather than what I paid for the options. Not sure how to list call options that were closed/sold at loss as superficial.

Zec,

Section 54 of the Income Tax Act states the following:

“for the purpose of this definition…a right to acquire a property (other than a right, as security only, derived from a mortgage, hypothec, agreement for sale or similar obligation) is deemed to be a property that is identical to the property”

indicating that for the purposes of determining superficial losses a broader net is used: the right to acquire a property and the underlying property itself are considered identical for this purpose. This definition only applies for the purposes of the superficial loss rule, however.

For this case, you could apply the superficial loss rule using AdjustedCostBase.ca as follows: