When an interest-bearing bond is sold before maturity or bought at a price higher or lower than its face value, a capital gain (or loss) will occur at the time the bond is sold (or matures). Therefore, the adjusted cost base of a bond must be tracked.

The buying and selling of a bond can be more complex compared to a stock because an additional component is involved: accrued interest. When a bond is purchased after its issue the buyer pays the seller accrued interest, in addition to the price of the bond. Similarly, when a bond is sold before maturity, the seller receives accrued interest in addition to the price of the bond. Canadian bonds generally make semi-annual payments. When a transfer of ownership occurs, the interest accrued from the last interest payment date until the sale date is paid by the buyer to the seller.

When you purchase a bond after its issue date, only the price of the bond and the commission are added to the ACB. This is less than the total amount paid because it does not include the accrued interest. As an example, let’s use the following quote for the purchase of $100,000 par value of HSBC BANK CANADA 2.938% 2020/01/14 bonds:

Note that the bond is trading at a premium because the price is greater than the par value. The price is $102,063.00 and the commission is $100.00. Also, there is $965.92 of accrued interest to be paid to the seller, representing the interest accrued from January 14, 2014 (the date of the last interest payment) to May 9, 2014. This accrued interest would be deducted from the interest payment you receive on July 14, 2014 when calculating your net interest income for 2014.

When calculating the ACB, only the price and commission are considered, without the accrued interest portion of the payment. The initial ACB is therefore equal to:

$102,063.00 + $100.00 = $102,163.00

(If the bonds were purchased at the time of issue for the par value of $100,000 then the initial ACB would simply be $100,000 plus any commissions paid.)

If the bond is purchased for the cost above on May 9, 2014 and held until maturity on January 14, 2020, you’ll receive $100,000 (in addition to all the interest payments including the final interest payment on January 14, 2020). This will result in a capital loss:

$100,000.00 — $102,163.00 = —$2,163.00

Let’s say, however, that instead of holding the bond until maturity you sell it on May 9, 2015 for a total price of $104,516.00 and a commission of $100.00. You would also receive an accrued interest payment of $965.92 for the interest accrued from January 14, 2015 to May 9, 2015, which would be taxable as interest income for 2015. This would result in a capital gain:

($104,516.00 — $100.00) — $102,163.00 = $2,253.00

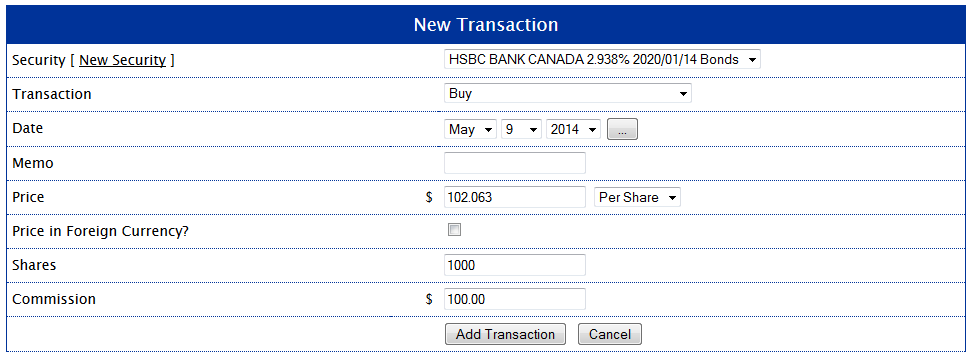

AdjustedCostBase.ca can be used for calculating ACB and capital gains for interest-bearing bonds. This can be accomplished using “Buy” and “Sell” transactions. The “Buy” transaction on May 9, 2014 would be entered as follows:

Bonds are generally sold and quoted in units of $100 so the transaction is shown as the purchase of 1000 units for $102.063 each. But the transaction could also be shown as the purchase of 100,000 units for a price of $1.02063, as long as you’re consistent with using the same unit amount for all transactions. Note that the commission of $100 is included, but the accrued interest payment is not, as it has no affect on ACB.

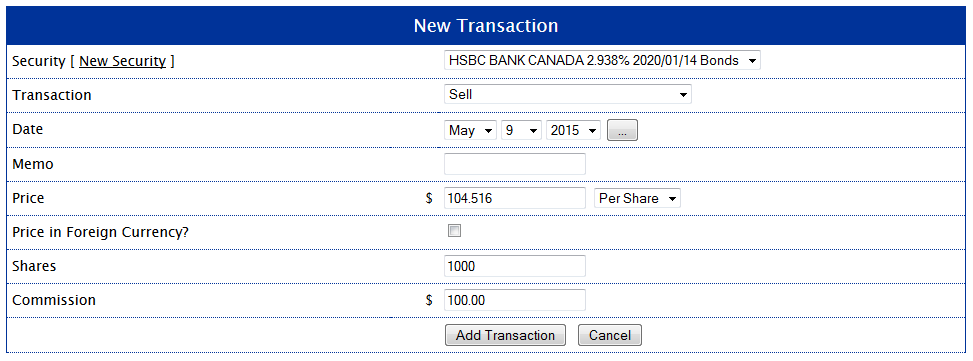

Similarly, the sell transaction would be entered as follows:

Once again, the accrued interest received is not entered because it does not affect the ACB or capital gains. The transaction summary is shown below, with a capital gain of $2,253.00:

How do I account for the accrued interest paid on the bond purchase when I do my tax return?

Thankyou

Mario,

Accrued interest should be included on your T5 slip, so inputting this data should account for it.

Thanks for the reply.

Accrued interest received is included on the T5. I’m talking about the accrued interest that I paid the seller when I purchased the bond. Is this amount shown in any slip?

Thanks again

Mario,

Sorry for misunderstanding the question. The accrued interest that you pay when purchasing a bond reduces the taxable interest for the next bond payment. I don’t think the interest income amount reported on your T5 includes this reduction so you’ll need to apply it yourself.

That’s what I was hoping you’d say.

Thanks again.

Hi.

I cant understand why accrued interest is not part of the adjusted cost base?

Is it because the seller pays tax on the accrued interest, and if the buyer includes the amount of accued interest in the adjusted cost base, he would pay taxes on it too?

Thanks so much.

Luc

Luc,

The accrued interest paid from by the buyer to the seller is neither subtracted from the ACB of the buyer nor added to the proceeds of disposition of the seller. The accrued interest is taxable as income for the seller, and is deducted from the income of the buyer (or rather offsets the income of the subsequent interest payment). The accrued interest does not impact the capital gain of either the buyer or the seller.

hello acb.ca,

i’m not sure if this question should be asked here or in the foreign securities/cash pages. regarding a <1y zero coupon bond (like a US t-bill) bought at auction through a US broker the handling of this security seems pretty straightforward as their is a quanity and a unit price to calculate the discounted price difference and the same can be applied when sold while the interest is just handled as regular income. On the US broker side this results in a 0.00 cost-basis, but obviously for acb we would need to take into account currency fluctuations.

Something odd that I've experienced this past tax year is a re-opening of a t-bill (as opposed to an initial auction) which caught me off guard since the bonds have the same MTD and DTD as well as the same CUSIPs, but were bought at different times and seemed identical to an initial auction bond. A concrete example would be buying a 6-month t-bill and then a 3-month t-bill 3 months later and they share the same CUSIP but different discount prices.

When calculating the ACB for the above scenario should I just treat the t-bills sharing the same CUSIP as the same security just bought at different times similar to how a regular stock/equity security would have its ACB calculated? My guess is yes since they share the same CUSIP, but I'm not sure how the CRA would regard them since they are foreign securities and I wonder if there is a difference in how the CRA treats foreign vs domestic bonds. thank you for your help