AdjustedCostBase.ca now offers a streamlined method for importing phantom distribution and return of capital transactions for many exchange traded funds (ETF’s), publicly traded mutual funds, income trusts and real estate investment trusts (REITs). Learn more about this feature.

Return of capital is a distribution from an investment that is not considered income. It’s common for a fund or trust to pay out a distribution in excess of its income earned. In this case the excess is considered to be return of capital.

The return of capital portion of a distribution is not considered taxable income for the current tax year. However, the adjusted cost base of the security must be reduced by the amount of the return of capital. As a result, the capital gain is greater when the investment is eventually sold. Avoiding or forgetting to factor in return of capital distributions when calculating ACB will result in an capital gain value that’s too low and therefore would be considered tax evasion.

It’s worth noting that return of capital is usually the most tax efficient type of distribution. In most provinces and most income tax brackets in Canada, the marginal tax on capital gains is comparable to that of eligible dividends. However, the capital gain (and thus the tax on the capital gain) does not occur until the investment is sold. Therefore tax is deferred on return of capital distributions.

Return of capital can occur for a variety of reasons. For example, a mutual fund may decide to distribute more than it has earned, in order to maintain a constant distribution even when income falls. In the case of a Real Estate Investment Trust (REIT), income for tax purposes is often less than net cash flow due to capital cost allowance for depreciation on its properties. As a result, if the REIT distributes its entire net cash flow to unit holders, the distribution will exceed net income and a portion of it will be considered return of capital.

For Canadians holding foreign investments, any income that’s considered to be return of capital by the foreign country will be immediately taxable as income. In other words, a return of capital distribution from a foreign fund does not provide the benefit of deferred taxes, and is taxed as income as opposed to a capital gain (and has no effect on ACB).

Return of capital is reported on box 42 on a T3 slip. However, a T3 slip you receive from your brokerage may aggregate the amount for multiple securities, and ACB must be calculated separately for each security. See Tax Breakdown Service for ETF’s and Trusts from CDSInnovations.ca for further details on this matter.

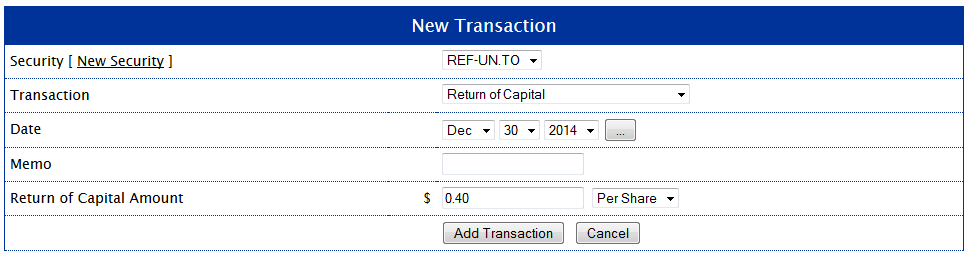

As an example, let’s assume you purchase 1,000 units of REF-UN.TO at a price of $45.00 per unit with a commission of $10.00. The initial ACB becomes:

(1,000 units x $45.00/unit) + $10.00 = $45,010.00

Then assume you receive a $1.00 per unit distribution that’s composed of 60% income ($0.60 per unit) and 40% return of capital ($0.40 per unit). The ACB must be reduced to the following:

$45,010.00 — (1,000 x $0.40/unit) = $45,010.00 — $400.00 = $44,610.00

As a result, the capital gain when the units are sold will be $400.00 greater than it would have been if the return of capital distribution did not occur.

Note that return of capital cannot reduce ACB below zero.

AdjustedCostBase.ca supports calculations for return of capital distributions. For the example above, the following “Return of Capital” transaction would be used:

The ACB would be calculated as follows:

The tool will not allow return of capital to be reduced below zero. If the return of capital amount should exceed the ACB, the ACB will be reduced to zero and the difference will be displayed as an immediate capital gain.

When you subtract the amount of return of capital from your ACB must you then subtract the units owned from your total using the price at time of distribution? I think not but please confirm.

Question:Does the return of capital method mirror the distribution additions but in reverse?

Thank you for your website and information. I understand adjusted cost base much better but still dislike return of capital. The fund is returning my invested money back to me increasing my ACB. If I fully reinvest the return of capital to buy more units should it not be revenue neutral therefore not subtracting the ROC.

The fund returns my money ROC which is subtracted from my account. My capital is returned to me. I never get to see it in cash or reinvested. It disappears into thin air or is kept by the fund.

I give you $100.00. You return the money by handing me a piece of paper saying you returned the $100.00 to me. I now have $100.00 less in my account.

Sounds like smoke and mirrors accounting to me.

Lucy,

ROC involves a cash distribution only and the number of units you own does not change. What do you mean by “distribution additions”?

In some cases, ROC can be a bad sign – for example a fund distributing more cash than it’s taking in to maintain the illusion of a high dividend yield.

But it other cases ROC can be viewed as a good thing. For example, REIT’s commonly have large non-cash expenses such as depreciation on real estate, and as a result cash flow can exceed net income for tax purposes. If the REIT distributes an amount that exceeds its net income, then the difference could be considered ROC. And if the depreciation for tax purposes is larger than the true depreciation of the property, then the distributions may be sustainable. This is beneficial for investors in terms of taxation since ROC will defer taxes into the future as opposed to dividends which are taxable immediately.

If you’re reinvesting an ROC distribution this will be equivalent to not having been paid ROC, all else being equal.

By ,” distribution additions”, I meant the interest, capital gains and dividends distributed to the fund. They are added to your ACB plus the units they buy are also added.

In my previous post I wondered if the return of capital subtraction also required the subtraction of units they had bought. You kindly answered my question by saying no,” the number of units you own do not change”.

You stated,”If you’re reinvesting an ROC distribution this will be equivalent to not having been paid ROC, all else being equal.”

Question#1: To clarify, are you saying that ROC is not subtracted from the ACB if you are reinvesting the distributions?

While researching ROC online I came across this from CRA – “Tax Treatment of Mutual Funds For Individuals” which is new information to me. Now I am really confused!

“If you receive a T3 slip with an amount in box 42 – Amount

resulting in cost base adjustment, the ACB of that mutual

fund trust identified on the slip will change. If box 42

contains a negative amount, add this amount to the ACB of

the units of the trust. If box 42 contains a positive amount,

subtract this amount from the ACB of the units of the trust.”

Question #2. How can the ROC be negative and why is it added?

One step forward and two steps back.

(Under the mattress seems so much simpler)

Thank you for taking time to respond to my questions.

Your knowledge is much appreciated.

I think it’s best to look at the return of capital and the reinvestment of the distribution as two separate events, since as you’ve mentioned the distribution can contain other components in addition to ROC.

Let’s say that you receive a distribution for $1.00 that’s 25% ROC and 75% income, and the entire distribution is reinvested for additional units. The ROC of $0.25 will decrease total ACB by $0.25. Then the reinvestment of the distribution will increase total ACB by $1.00. So the net increase in ACB is $0.75 resulting from both the ROC and subsequent reinvestment.

The ROC does not affect the number of units, but the reinvestment does increase the number of units. If the entire distribution is ROC and is entirely reinvested, the net affect on ACB will be zero. But if the distribution is not entirely ROC (and is still full reinvested) ACB will increase.

I’m not sure under what circumstances ROC would be negative (I don’t think I’ve encountered this before) but it would make sense that it should be added to ACB since a positive value is subtracted from ACB.

Quick question: I understand that ROC reduces the ACB of the held securities, but what happens when you dispose of ALL of your shares in the year and then receive a ROC at the end of the year (per your T3 slip)? I’m assuming that you still subtract the ROC from the ACB at the time of the sale(s), (or from what you report) so that it reflects on your capital gain/loss? Or is there another way to do this? Many Thanks!

lastminutetaxdoer,

ROC can occur in distributions that happen any time of the year. Most likely you received ROC distributions before you sold the shares and that’s why it’s listed on your T3 slip. You should include it when calculating ACB (before the shares are sold).

Of course, that makes obvious sense! And I went through my T3 Summary of Trust Income and that made it easier to find and enter the ROCs, rather than go through all of my securities transactions. Luckily the calculations turned out to be the same as if I subtracted it at the end of the year but I will make sure to enter them as they are distributed throughout the year. Thanks:)

In your article you said:

“For Canadians holding foreign investments, any income that’s considered to be return of capital by the foreign country will be immediately taxable as income. In other words, a return of capital distribution from a foreign fund does not provide the benefit of deferred taxes, and is taxed as income as opposed to a capital gain (and has no effect on ACB).”

Is this something new? I am looking at my $US account for 2011 and see a ROC distribution. The $amount of the ROC is not included in the total income on the companion T5 form, therefore was not taxed as income. If it is not to be used to reduce the $UC cost base, then is it really a tax-free distribution? Or have I missed something?

Tony,

It’s my understanding that it is indeed the case that distributions that are classified as ROC in a foreign country are fully taxable to Canadians. Here’s an article that explains the idea further:

http://business.financialpost.com/personal-finance/taxes/not-all-dividends-are-taxed-the-same

I am getting a return of capital adjustment figure on year end statements and on the T3 box 42,but not receiving any actual money. This roc adj. is used to decrease my adjusted cost base and therefore increase my capital gains if I were to sell the shares. Since I’m not receiving any actual $ what purpose does this serve?

Sol,

It’s possible the return of capital was reinvested into the fund and not distributed. If this was the case then the return of capital would decrease the ACB, but the reinvestment would increase the ACB by the same amount, and they would effectively cancel each other out.

Unfortunately, reinvested amounts are not reported on T-slips. To see if there was a reinvested distribution for your fund you can follow the instructions here:

http://www.adjustedcostbase.ca/blog/tax-breakdown-service-for-etfs-and-trusts-from-cdsinnovations-ca/

and look for any “Total Non Cash Distribution” amount.

Hi, I’m new to mutual funds this year, but learning fast. One of the T3’s that I received this year had an amount in Box 42. I have not disposed of the funds in the T3, so can I just ignore the amount in Box 42 this tax year until the year that I sell the fund and then use it to get an adjusted cost base?

Mame,

Yes, that’s right.

@Mame Bate

Probably OK for this year, but after several years its possible for the RoC you receive on your investment to exceed the amount you initially paid for your investment. If the cumulative return of capital exceeds the amount you actually paid to acquire fund units, then your ACB could go negative. Negative ACB in a trust unit results in a capital gain that must be reported in that year. You should be tracking return of capital you receive on a fund by fund basis when you hold your funds in taxable accounts.

Thank-you both – I am taking notes for this and future years 🙂

Hi,

I own a company and have investments, one of which is an REIT stock. I am wondering how to account for ROC in my books of account, or even IF the ROC should be reflected in my books. (I enter the monthly dividends into my books.)

I keep a separate spreadsheet of purchases/sales and monthly dividends, and it is easy to apply the ROC there to reflect the ACB. Should I also be making a (credit) journal entry to the book value (asset) account to reduce the book value in my books of account (to accurately reflect company assets)? And if so, what is the contra account I should debit? It isn’t income for the current tax year. I didn’t receive any cash in hand. It isn’t dividends. How do I account for it?

Thanks!

oradba.ca,

Normally for ROC, you can account for it in your books by crediting/decreasing the REIT and debiting/increasing cash. That seems unusual that you didn’t receive the distribution in cash, so you may want to double check that (unless the distribution was reinvested, in which case you would debit/increase the REIT, effectively negating the ROC).

Thank you, I think have it now. The confusion comes by my monthly investment statement wherein the total distribution is listed simply as dividends. It isn’t until I get the T3 details that I can see this single value broken down into ROC (box 42 – amount resulting in cost based adjustment), Capital Gains (box 21, but listed on my statement as “Capital Gain Div”), and Other Income (box 26).

I have been accounting monthly in my books as 100% dividends, and then when the T3 details arrive I remove the money from dividends and adjust the cost base in my book value account. Since I only report annually, this works for me for the most part. My year end is July and I get the T3 details for the previous calendar year. I’ll have to see if I can get these details on demand.

Your article and reading through the comments have been very helpful.

Thanks!

I receive T3 slips with box 42 ROC details. I would like to post the information on Quicken Home & Business 2016 program. There is a transaction on Quicken named Return of Capital & Transfer but what do I enter for Transfer Account?

For a Canadian REIT, is the amount reported in box 21 of the T3 slip as a capital gain added to the adjusted cumulative cost base?

Ian,

Capital gains distributions do not affect ACB, unless they are reinvested (via a DRIP or a phantom distribution). Capital gains that appear on your T-slips are reportable and taxable for the current tax year.

hello,

Is tax info on T5008/RL-18 usually correct for income tax purposes?

Do I still need to verify ACB as per box 42 for all years?

I don’t have any records when I stopped receiving cash dividends and started reinvesting.

Also, on the statement I received from the Trust, I can see that amount is reported in the box 42 of T3 was used for shares acquisition. Confused. It says in the post that ROC is not used to buy shares. Should I then increase ACB by that amount or decrease?

Please advise and clarify.

Thanks

laa,

A report on ACB and capital gains from a mutual fund directly is more likely to be correct than that from a brokerage. See the following for more information about this:

https://www.adjustedcostbase.ca/blog/can-you-rely-on-your-brokerage-for-calculating-adjusted-cost-base-and-capital-gains/

If a return of capital distribution is reinvested, then the two actions effectively cancel each other out, resulting in no change in ACB. However, if the distribution is not entirely composed of ROC and/or the distribution is not entirely reinvested, then there will likely be a net change in ACB.

Pingback: Ask the Spud: Can I Make Taxable Investing Easier? | Canadian Couch Potato

How do you deal with the ROC reported on Box 113 of T5013 (Partnership Income)? I believe it is still used to reduce the ACB of the limited partnership. How do make an entry of this in the transactions? Btw, I’m using your premium service and I really love it so far! Thanks:)

lastminutetaxdoer,

I believe ROC reduces your ACB for a limited partnership in the same way as other types of units. This can be inputted into AdjustedCostBase.ca as a “Return of Capital” transaction as described above. Just make sure that the total return of capital amount is correct when adding the transaction.

Thanks for your feedback!

Pingback: Easier than ACB – Canadian Portfolio Manager Blog

Hello,

My broker on an annual basis reduces my ACB by the amount of ROC on my T3 slip saving me the headache of doing the calculations myself unless I sell before the adjustments are processed. For most of my securities the amount reduced matched Box 42 on my T3 with the exception of Chartwell REIT. This REIT had a non-reportable component to the distribution that seems to have thrown the calculation out of whack. Does a non-reportable component affect the amount of the book value adjustment I should have on my ROC?

MungoDM,

According to Chartwell’s 2016 Management Discussion & Analysis:

“In 2016, 36.7% of our distributions were classified as return of capital, 58.2% as non-taxable capital dividend and 5.1% as non-eligible dividend.”

The non-taxable capital dividend portion does not affect ACB (and of course is not taxable). Only the return of capital portion affects ACB.

Thank you greatly for sharing this valuable website and information. I have found it to be tremendously helpful to figure out how to calculate and track the adjusted cost base. For the Return of Capital ACB calculations, you have provided an example using the ROC percentages. Could you kindly offer an example on how you calculate the ROC when the CDS tax break down service reports ROC RATE instead of PERCENT values, using 2016 Horizons Active Emerging Markets Dividend ETF – Class E units (HAJ) for instance. I would like to know either how to calculate either the ROC ACB using the RATE value, or how to convert the RATE to PERCENT so I may apply it to your original example. Thanks again.

AS,

When the ROC amount is provided to you as a dollar amount, no further calculation is necessary. Adding a new “Return of Capital” transaction in AdjustedCostBase.ca you can input this dollar amount as a per share value. For example, the ROC amount for HAJ distribution with a record date of January 29, 2016 distribution would be $0.00466 per share.

Hi there, I disposed of a REIT which I held for a few year last year. In the past two years in April I noticed ROC amounts in my online brokerage activity. Although it reported $0 I made a note of the amount of the ROC and reduce my ABC in my own record keeping. I am wondering what am I to do for tax purposes if I notice another ROC adjustment next month despite having sold my shares last year? Would I have to reduce my ACB again and report the gain/loss for the 2017 tax return ?

Thanks

JB15,

ROC for the REIT would only be applicable to you for distributions occurring before you sold it. It’s not clear to me about the time frame for which your brokerage is reporting this. For example, does the April item correspond to an aggregate of all ROC for the previous year? In any case, there are ways you can determine the ROC on your own, without relying on your brokerage’s reporting, which may be incorrect or delayed. Here are some possibilities:

– https://www.adjustedcostbase.ca/blog/streamlined-import-of-return-of-capital-and-phantom-distributions-and-for-exchange-traded-funds-etfs-publicly-traded-mutual-funds-and-trusts/

– https://www.adjustedcostbase.ca/blog/tax-breakdown-service-for-etfs-and-trusts-from-cdsinnovations-ca/

– Check the REIT’s web site or contact them about ROC information.

I am a tax preparer and find this all so confusing . .. none of my clients keep track of their ACB making the necessary adjustments of ROC. And there is no way I can track it for them without loosing my mind!

Why can’t the fund companies with their fancy computer systems keep track of this for us and give us a “good” number to use at tax time???

Hi – I Am invested in a limited partnership and have an ROC – box 113 on on T5013. I see that it reduces my ACB, but how is this supposed to help my total tax payable in 2017? I can’t see anywhere ro apply this ACB in the Turbo Tax software, so am looking for sone assistance on this. Am I misunderstanding this? Isn’t there supposed to be a tax advantage to me on an ROC?

Thanks very much in advance.

Ben,

You will not need to report anything related to your ACB of these shares and the return of capital distributions until the shares are ultimately sold. This is in fact the tax advantage of return of capital compared to other forms of distributions such as dividends or interest income (although from an accounting perspective, return of capital is equivalent to getting some of your original money invested back). Return of capital will reduce your ACB, thus increasing your capital gain when the shares are sold, but the amount is not immediately taxable.

Thank you – just one thing further on that. If I am receiving an ROC on that, why would the partnership be reporting those ROC as dividends, but also showing them on the T5013 as interest from Canadian sources? Box 128. Again, I may be missing something here, but that seems to defeat the purpose of the investment as a limited partnership rather than an interest bearing investment.

Ben,

A distribution can have different portions designated as different types of income. For example, it could be part return of capital and part interest. The different components should add up to the amount of cash distributed (unless there was also a non-cash portion of the distribution).

How can I find a list of TSX companies whose payments are substantially return of capital?

I’ve come to several dead-ends trying to find the answer to my question and this might not be the best place to ask, but here goes:

If a U.S. share holder of a Canadian company receives a ROC, what are the tax implications? I believe they are not taxed by Canada, but can anyone offer any ideas of how this is reported to the U.S. IRS and what tax rates apply? Does my cost basis of the stock drop based on the payment?

Thanks in advance

Baffled

Tony,

I’m sorry, but I’m unfamiliar with US tax rules.

In the reverse situation – where a Canadian owns US shares and receives a distribution that is considered return of capital in the US – the distribution is normally considered to be foreign income.

As if I haven’t pulled enough hair out doing this !!!!

I have entered lots of entries representing every transaction reported on my monthly statements from CIBC’s Personal Portfolio Service accounts, merged them and entered them into your site.

I made the assumption that Reinvested Distributions on these statements are to be entered on your site as a Reinvested Dividend (so the amounts would be shown on the T3 as dividends), but now realize that if they could be reinvested capital gains. I then read that a reinvested capital gain is considered a sell followed by a purchase. MORE Sell lines to go onto Sched 3!!! How do I determine if these are Reinvested Dividends or Gains?

I stumbled on this looking for info on Return of Capital. I have 2 funds in the portfolios that report on the T3 statement a “Return of Capital”. BUT I can’t find anything in the monthly statements that suggest anything about “Return of Capital” itemized. Let alone a date of when it occurred to lower the ACB by the RoC.

I’m just drowning here!

Stuart,

I have never heard of a reinvested distribution corresponding to a deemed disposition. I’m not sure whether you are referring to dividend reinvestment plan (DRIP) or whether this is the result of a phantom/non-cash distribution. These are described here:

https://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-reinvested-distributions-dividend-reinvestment-plans-drips/

https://www.adjustedcostbase.ca/blog/phantom-distributions-and-their-effect-on-adjusted-cost-base/

In either case, there should be no deemed disposition. The reinvested amount will be taxable as investment income in the year of the distribution. Phantom distributions are often, but not always, coupled with capital gains.

If you’ve already inputted phantom distributions as Reinvested Dividend transactions on AdjustedCostBase.ca, you can leave things as is. You may need to input additional transactions to account for any return of capital or capital gains distribution components associated with these distributions.

There’s the rub … the info on the T3 gives a summary showing the breakdown across the funds for the year of the items reported on the T3 detailed boxes But return of capital is NOT shown in those boxes and the monthly statements don’t show where it came from! AND there’s nothing to indicate WHEN to date the transaction for the reported return of capital.

The reinvested distributions don’t say what their source was … I added up the reinvested distributions and they are more than the reported dividends.

I am coming to the conclusion that this is a nightmare that never seems to end!

All the statements seem to add up properly without any phantoms.

A little closer mebbe … IF I add, for a given fund in the portfolio

Capital Gains

Actual amount of eligible dividends

Taxable amount of eligible dividends

Foreign non business income less tax on same

Return of Capital

This adds up to the reported reinvestments

BUT all I have are totals and no dates these amounts happened so can’t know in what order they need to be inserted and what to do with them!!!

Stuart,

I would suggest contacting the fund company to see if they can provide the exact dates. If you haven’t sold any units at all during the tax year in question, it should rarely matter when you input the return of capital transactions (an exception being in the rare case where return of capital might reduce your ACB to zero). In this case you could input the return of capital as an aggregate amount at the end of the year. If, however, you’ve sold units during the year then the timing of the return of capital can impact your capital gains.

I was wondering what constitutes as a foreign investment for ETFs. I have some Canadian listed ETFs (XUU, XEF, etc.) that hold investments from foreign countries and received notice on the T3s that there is some return of capital for these funds. Am I to claim the ROC as capital gains from these funds in the year that they are distributed or because they are Canadian listed funds, adjust the ACB accordingly?

Many thanks for your insights!

Chris,

For Canadian-listed ETF’s such as those that distribute return of capital, your ACB should be reduced accordingly and the return of capital portion of the distribution will not be immediately taxable. It’s only distributions from foreign funds that cannot be considered as return of capital, even if they are considered the equivalent of such in the foreign country.

Hi – I have a T5013 reporting an amount in box 128 for Interest Income. Box 113 is also reporting an amount slightly less than box 128. I realise that the ROC in box 113 is to reduce the ACB, but do I need to deduct 113 from 128 to realise/defer the tax benefit/cost in each year that I own the limited partnerships share? If not, I don’t see the near term benefit of owning a limited partnership holding.

Thanks in advance,

Ben

How do I calculate the ROC to apply to my ACB when I have only sold a portion of the stock I own? I have owned the stock for a few years and the T-slip for 2017 also showed an ROC amount.

Jim,

Your ACB should be adjusted based on each individual distribution that includes return of capital (on the record date). If you have bought or sold units during the year, you should not simply deduct the total return of capital if there were multiple distributions throughout the year.

Hi – I posted this mid April, but didn’t see a reaponse. Any thoughts??

Hi – I have a T5013 reporting an amount in box 128 for Interest Income. Box 113 is also reporting an amount slightly less than box 128. I realise that the ROC in box 113 is to reduce the ACB, but do I need to deduct 113 from 128 to realise/defer the tax benefit/cost in each year that I own the limited partnerships share? If not, I don’t see the near term benefit of owning a limited partnership holding.

Thanks in advance,

Ben

Ben,

The potential tax advantage of return of capital is that it’s not taxable in the year of the distribution. It reduces your ACB, and as a result you will incur a higher capital gain when you eventually sell.

Return of capital is not directly related to interest income. These are two different types of distributions. Return of capital should not be deducted from any other form of income.

My T3 totals for Return on Capital for Year 2018 include amounts paid in January 2019. Can I assume that I can exclude the January 2019 amounts when reporting/calculating my capital gain? (my Adjusted cost base has gone negative)

Debra,

Often funds make distributions with a record date near the end of the year, and the cash is paid out at the beginning of the following year. For the purposes of determining the year applicable to a distribution, it is the record date that matters. So it’s possible that a cash received in 2019 can apply to the 2018 tax year.

Hello,

I have a question related to how this whole process works and trying to do the accounting for it. If an ACB is reduced the journal entry would look like. I know it is a return of capital when I look at the box 42 for the T3 slip.

CR Investment

DR ????

What would the DR side be? Especially if the cash balance did not change after the ACB on the mutual fund/ trust was reduced. In my case, its the Chartwell fund.

Ryan,

If return of capital is distributed, either you should receive the cash or it is reinvested. If it is reinvested, then this would be equivalent to a credit for the investment and a debit for cash, followed by a debit for the investment and a credit for cash (the two sets of transactions would cancel each other out). In some rare cases a phantom distribution may have a return of capital component, in which case the return of capital and reinvestment would again cancel each other out, and it can be the case that no additional units are received.

I believe the ACB calculation method described in the comments for limited partnerships are incorrect. Their tax advantage is really the fact that no matter the characteristic of the original distribution, it can be used to reduce the ACB.

The following site[1] pretty much says all income must be used for calculating the ACB. If I use BIP.UN[2][3] for 2018 as an example, the calculations take into account all income distributions no matter their type.

[2] is an example of an ACB calculation for someone who received BIP.UN units as a special dividend from BAM.A.

[3] describe the distributions for a single unit of BIP.UN in 2018

We can clearly read in [2]:

“A holder of units is required to reduce the adjusted cost base of their units by an amount equal to the cumulative distributions received plus/(minus) any cumulative income/(loss) and other amounts allocated on their T5013. Taxable income is allocated to unit holders based upon distributions. The computation of adjusted cost base must be done in Canadian dollars.”

In the example[2], the ACB is reduced by a total of $2.44931 per share for 2018, this number matches the combined dollar amount for all distributions found in [3]. This is regardless of the distribution characteristic.

Paradoxically, we can see in [2] that the ACB is increased by $0.89666, which also matches the total tax allocation in [3].

For this site, although sub-optimal in terms of their description, I believe all income from an LP would be booked as an RoC while the net tax allocation would be booked as a “re-invested capital gains distribution” with zero shares received.

I am still trying to figure out how beneficial is an LP in terms of savings versus a regular REIT. I believe where it becomes beneficial is that losses in the partnership are carried through to the unit holder. In this case, BIP.UN was profitable for 2018, but BPY.UN[4] was not. In such cases, the ACB for BPY.UN would go up, not down, and this is backed up by the example at [5].

Open questions:

– If distributions, other than “true” RoC, are taxed in the year they are received, how is this more tax efficient?

– If ACB is reduced by all distributions, doesn’t that mean we’re taxed a second time on the same dollars when the units are actually disposed?

– If the ACB of the units ever goes to zero, doesn’t this mean the same dollars are taxed twice? First in the distribution, second on the capital gain.

[1] https://www.mnp.ca/en/posts/an-introduction-to-partnerships

[2] https://bip.brookfield.com/~/media/Files/B/Brookfield-BIP-IR-V2/2018-tax/Calculation%20of%20Adjusted%20Cost%20Base%20Common.pdf

[3] https://bip.brookfield.com/~/media/Files/B/Brookfield-BIP-IR-V2/2018-tax/2018%20Canadian%20Taxable%20Income%20Calculation%20Common.pdf

[4] https://bpy.brookfield.com/~/media/Files/B/Brookfield-BPY-IR-V2/tax-information/BPY%202018%20Canadian%20Taxable%20Income%20Calculation%20Updated%20Language.pdf

[5] https://bpy.brookfield.com/~/media/Files/B/Brookfield-BPY-IR-V2/tax-information/BPY%20Adjusted%20Cost%20Base%202018%20Final.pdf

Patrick,

It seems that technically speaking, the full amount of distributions from a limited partnership should be deducted from ACB, while the income should be added to ACB. In the case of BIP.UN in 2018, $2.4493 per share was distributed, of which $0.8968 was net taxable income. The difference of $1.5525 is considered return of capital.

We can calculate the ACB by deducting $2.4493 per share and then adding $0.8968 per share, resulting in a net decrease of $1.5525. In this case, this is equivalent to reducing the ACB by the amount of return of capital. Either approach should have the same end result.

So while all distributions from a limited partnership will decrease ACB, the net effect is the ACB will decrease by the amount of return of capital. If the distribution amount is smaller than the net income, the ACB would increase. This would be equivalent to a net reinvested distribution.

Note that a reduction in ACB in isolation is not a tax advantage but rather a disadvantage. A lower ACB will result in a high capital gain when the units are eventually sold.

The potential tax advantages of a LP may depend on the investor’s circumstances as well as the characteristics of the LP. One potential advantage can be the ability to flow-through losses. Another is that if the units are held in a registered account, no taxes would be paid by either the investor or the LP (with the possible exception of foreign taxes withheld). In the case of a corporation held in a registered account, the investor would not pay taxes but the corporation would (and there would be no dividend tax credit available).

With return of capital, there is not really any double-taxation. While your ACB will decrease, the value of the shares or units should fall by the same amount, all else being equal. The ROC distribution is not taxable at the time of the distribution, and in theory there is no net change in capital gains when the shares or units are eventually sold.

Your ACB is not permitted to fall below zero. If an ROC distributions exceeds your ACB then the ACB will be reduced to zero and the excess will be taxable as a capital gain at the time of the distribution.

Thanks for replying,

It just seems strange that if I have, say Canadian based interest allocated to me in a T5013, that I would reduce my ACB on that too because I’m paying taxes on the income reported on that tax slip.

Technically speaking, I am taxed in a non-registered account on that interest, so why is it reducing my ACB too?

Also, same thing, if my shares hit 0 eventually, that means I would pay taxes on both the income found on the T5013 and on the capital gains on the shares in the same year.

It seems in both cases increasing the ACB by the tax allocation is meant to counter this double taxation effect but I don’t get it.

LPs are giving me a headache.

Patrick,

I think it’s best to think of the tax consequences of a limited partnership as 3 distinct parts:

1) Net income is earned and taxed in the investor’s hands

2) The net income is reinvested, increasing ACB

3) Cash is distributed as return of capital, decreasing ACB

If the net income is equal to the distribution, then 2) and 3) will cancel each other out, with no net increase or decrease to ACB. You will simply be taxed on the net income earned and you’ll receive that as a cash distribution.

When you incur capital gains due to your ACB falling below zero, the net capital gains incurred during your lifetime will be the same as if you were permitted to reduce your ACB below zero. The only difference is that capital gains that would have been incurred in the future will be shifted to the present.

I have a slightly different situation:

I am holding my investments inside a TFSA so I do not receive a T3 slip at the end of the year.

When I receive my monthly statement in May each year (for past 3 years) I see a description called “ROC Cost Adjustment” and there will be 12 line items (for each month of the year). There is no amount of cash being returned to me however the securities Company decreases my original cost base (ACB).

From what I’ve read above if there is no cash being distributed back to me, the funds maybe getting reinvested – but if this were the case, why is the securities company reducing my ACB?

I contacted the CFO’s at each of the holdings (one of them is a REIT) and have received no response.

How else can I find out what exactly this “ROC Cost Adjustment” is?

Mandy,

It could be that the distribution was reinvested as a phantom distribution (in some uncommon cases phantom distributions can be classified in whole or in part as return of capital) or reinvested as a result of being enrolled in a dividend reinvestment program.

Note that it is not necessary to track ACB for holdings in registered accounts.

Thanks for that information. I am aware that tracking cost base for registered accounts is not necessary. I guess I’m just curious and trying to learn as much as possible:)

I will do some more research into what a “phantom distribution is”. I know for a fact that I don’t have a dividend reinvestment program setup with any of the holdings in question.

You run a great resource here – bravo!!

If I have an interest in an LP and net income is always reinvested (increased to ACB), when I redeem units I won’t have a gain as ACB increased to FMV of the units? Although I may have gains allocated on the T5013 up to the point of redemption.

Carl,

If your ACB happens to be equal to the proceeds you receive from the sale, then yes, your capital gain would be zero. Maybe this would happen if there is some agreement to redeem the units at book value. But this is an unlikely scenario in general with publicly traded partnership units (for example, Brookfield Infrastructure Partners L.P.) as you would be selling the units at market value, which fluctuates continuously.

I have investments in REIT’s and recently redeemed a portion and withdrawn the cash.

How do I report the profit which is 9% Capital Gain, 30%I income ad 31% Return of Capital?

Gerry,

I’m unclear about what you mean by a profit being allocated into capital gains, income and return of capital. If you’re referring to a distribution, then the return of capital portion reduces your ACB. The remaining elements should appear on your T3 slip and should be reporting on your tax return accordingly.

If you have sold units then a capital gain or loss will occur.

Hi,

In regards to estate planning, if you own stock which its ACB has eroded over time because of ROC, and you leave that stock in kind to your kids as an inheritance, will the estate have to pay capital gains based on the reduced ACB or on the original book value of the stock?

Thanks!

Claude,

At death someone is deemed to have sold all assets at fair market value (except in certain circumstances, such as when assets are passed along to a spouse). The final tax return should report the disposition based on the ACB, including all adjustments such as return of capital.

Hi

I was looking to purchase a REIT listed on the Toronto stock exchange that has hotels situated in the USA and it pays a US dollar distribution. I am told the distribution is approx 40% ROC and 60% income. You stated earlier that foreign REITS are considered foreign income when it comes to the ROC portion and there is no tax deferral and ACB and it’s considered regular income like the rest of the distribution. Is that still the case with the Reit itself being listed on the Toronto stock exchange or is it still considered foreign?

If that is the case and it is considered foreign and the ROC is taxable does my ACB stay the same and not get lowered then?

And finally the IRS withholds 30% of the distribution in a taxable account I believe.If I sign a W8BEN form I believe I get 15% of that back, is there a way to get the last 15% back ?

Thanks for your help

D

To address the comment of Darran Chapman, I believe you’re talking about HOT.UN… Please note that thing is not a REIT but a limited partnership (LP).

ACB must be adjusted by all income received and then subtracted by the tax allocation.

Darran,

I believe this depends on where the company is located rather than where its stock is listed (some companies are inter-listed). It sounds like this is considered a US REIT, in which case ROC would not apply. You can check your T-slips to see how the income is reported. If you received a T3 slip with a portion of this REIT’s distribution allocated to box 42, then that is an indication that the income can be considered ROC.

The withholding taxes do not impact ACB, however, you can claim them on T1 return to avoid double paying this tax.

Thanks, Patrick. Yes, a portion of American Hotel Income Properties REIT LP’s distributions are considered to be return of capital for Canadian investors.

Hi,

Yes, it is indeed RoC, but it doesn’t really matter since it’s an LP. It’s incorrect to just reduce by the total RoC in such cases.

Patrick,

That approach seems to be equivalent to just subtracted the reported ROC from your ACB. In 2019 American Hotel Income Properties REIT LP reported the following (all figures converted into CAD$):

Total Reported Return of Capital: CAD$0.7195

Total Distributions: CAD$0.8591

Total Foreign Dividend and Interest Income: CAD$0.1965

Total Capital Gains: CAD$0.0468

Total Carrying Charges: CAD$0.1757

If I subtract the income from the total distribution amount:

Total Distributions – (Total Foreign Dividend and Interest Income + Total Capital Gains – Total Carrying Charges)

= CAD$0.8591 – (CAD$0.1965 + CAD$0.0468 – CAD$0.1757)

= CAD$0.7915

Both approaches yield the same result. Are there any situations where this is not the case?

Hi,

I believe so, looking at BPY.UN for 2019[1], even if there was RoC, there’s no adjustment to the ACB at all for the year. The tax allocation was enough to cover the full RoC payout. Per this document we subtract $1.75825/unit but add back exactly $1.75825/unit.

If we use other documents/examples for other years on this page[2][3]. I believe this is how it should be done for 2019.

I believe this calculation is correct. Please let me know what you think.

[1] https://bpy.brookfield.com/~/media/Files/B/Brookfield-BPY-IR-V2/tax-information/bpy-summary-2019-bpy-units.pdf

[2] https://bpy.brookfield.com/stock-and-distribution/tax-information

[3] https://bpy.brookfield.com/~/media/Files/B/Brookfield-BPY-IR-V2/tax-information/BPY%20Adjusted%20Cost%20Base%202018%20Final.pdf

Patrick,

BPY.UN’s tax allocation for 2019 seems similar to that of HOT.UN in that there is an excess of distributions over taxable income allocation, with the difference being equal to return of capital that reduces ACB.

It’s different for 2018 though:

https://bpy.brookfield.com/~/media/Files/B/Brookfield-BPY-IR-V2/tax-information/BPY%202018%20Canadian%20Taxable%20Income%20Calculation%20Updated%20Language.pdf

In this case the total of the cash distributions is smaller than the taxable income allocation. This case is similar to a phantom distribution in a fund/trust since there is a net increase in ACB.

This scenario can still be inputted into AdjustedCostBase.ca using a “Return of Capital” transaction, with the return of capital amount set to the negative net amount (negative return of capital amounts are allowable).

Or, it could be inputted using the following transactions:

– A Reinvested Dividend transaction with a total amount set to the total tax allocation of the LP.

– A Return of Capital transaction with the amount set to the distributions received from the LP (not the net return of capital amount).

I own Dream Office REIT and I get annual Return On Capital. This year was $377. I did not see this money at all all it did was lower my average cost per share.

What is the purpose of this and why would I want it? It artificially inflates my gains. This is held in an RRSP.

Derek,

Distributions from Dream Office REIT have been almost entirely allocated as return of capital for the last few years. If you did not receive any distributions as cash then it’s likely that you’re enrolled in a DRIP and the distributions were reinvested in new units. It it not necessary to track ACB for holdings in RRSP accounts as capital gains do not need to be calculated there.

As in Derek example, if the return of capital, ROC enrolled in a DRIP was NOT in a registered account therefore the ROC is reinvested then the ROC is not deducted from the ACB.

Would this statement be true?

Lucy,

It’s true that if a distribution entirely consists of ROC and it is entirely reinvested then there will be zero net change in ACB. However, I would suggest thinking about the distribution and reinvestment as two distinct events. In many/most cases distributions are not entirely made up of return of capital (for example, Dream Office REIT’s distributions were 98.96% ROC in 2019). Also in the case of a synthetic DRIP only a whole number of shares are acquired with the remainder paid in cash. Either of these factors would result in a net change in ACB.

Thanks for the reply, however, I didn’t see any increase in share numbers either. My dividends are DRIP, so I see those reinvested as new shares monthly, butnot the ROC. No new shares, bo cash, just adjusted cost per share.

Any idea what is going on?

What my line item says is:

DREAM OFFICE REAL ESTATE INVT TR UNIT SER A 2019 RETURN ON CAPITAL ADJUSTMENT TO BOOK COST -337.52

There doesnt seem to be a purchase of shares and there is no money going into my account.

I have the same DRIP experience not only with ROC but some kind of phontom Capital Gain (on which I must pay tax). As you observe, no additional shares are acquired, so I assume this is simply a way of giving the impression that the “dividend return” is maintained at a suitably high rate.

Derek,

If you’re enrolled in a DRIP then I would not expect you to receive any cash (with the exception of a residual amount if the distribution is only reinvested in whole shares). The return of capital is included in the distribution, which in your case is reinvested. It isn’t a separate amount.

Awit,

It is a fairly standard practice for ETFs to reinvest capital gains realized on dispositions (for example, when index constituents change or when rebalancing). For many investors it would be undesirable to receive potentially large distributions in this case and it is unrelated to income received from the holdings. So ETFs will typically reinvest realized capital gains. The shares are usually immediately consolidated such that each unitholder maintains the same number of units as before. Further information is available here:

https://www.adjustedcostbase.ca/blog/phantom-distributions-and-their-effect-on-adjusted-cost-base/

Some great comments to read here. Thank you for explaining this so well.

Do you know of a website that will break down the annual distribution into it’s separate parts (eg, ROC, Div, Int, Cap Gain)? Morningstar used to do this. I can no longer find it on their website.

For US taxes, the ROC is considered a taxable distribution. If from a Canadian mutual fund, or other flow through entity, then it becomes a PFIC and is taxed as such on a special IRS form.

Gail,

You can view the tax breakdown for a mutual fund on Morningstar from a fund’s page by clicking on “Distributions” in the “Performance” tab. This will bring up a table showing the distribution breakdown on an annual basis. Data for individual distributions does not seem to be available, however.

For publicly-traded funds, please see the following:

https://www.adjustedcostbase.ca/blog/tax-breakdown-service-for-etfs-and-trusts-from-cdsinnovations-ca/

I am confused about how to enter transactions which involve a monthly distribution.

I own a growth and income mutual fund. Each month I receive a distribution which is reinvested. So, let’s say I started with 100 shares. After the first month, I received a distribution of 1share. My holdings now show as 101 shares. The value of this transaction is identified as $10.

That happens each month. At the end of the year, I have 112 shares and distributions valued as $120. Then I receive a tax slip indicating all the distributions are considered “Return of Capital”. I.e. – return of capital for the calendar year was $120.

How do I logistically enter these transactions? Do I use the reinvested dividend for each monthly transaction and then a year end return of capital entry so my ACB is adjusted? If I just enter them as monthly Return of Capital transactions, my share holdings never increase and do not match the number of shares from my monthly account statement.

Thanks.

Andrew,

For each monthly distribution you will need to input one “Return of Capital” transaction and one “Reinvested Dividend” transaction.

In the case where you haven’t sold any shares throughout the year then you could consolidate the ROC transactions into a single value at the end of the year. However, if any units were sold during the year, then the ROC transactions should be broken down by month as this will impact the capital gains/losses for these sales.

Thanks. Much appreciated.

I have received two T5’s (from different Companies) which are showing at the bottom of the slip “Return Of Capital” for your records. The funds are’ Mackenzie US Midcap Growth Class’ and ‘Fidelity Insights Currency Neutral Class’.

Do I deduct these from the ACB?

Thanks

Mary,

Yes, return of capital (normally found on a T3 slip) should be deducted from your ACB. If there were multiple distributions for the year, then in general the amount corresponding to each distribution should be deducted at the time of each distribution (though in some scenarios, such as when there are no sales during the year, a total annual amount can be deducted at the end of the year).

I own a stock (Great Bear Resources) that distributed spinoff shares as a return of capital in my non-registered account. The following is copied from the Condensed Financial Interim statements: “On May 5, 2020, GBR completed a share capital reorganization by way of statutory plan of arrangement whereby all shares of Royalties Corp. were distributed to shareholders of GBR, as a return of capital (the “Arrrangement”).

…..

Pursuant to of the Arrangement, existing shareholders received one (1) share of the Company for every four (4) GBR shares they held…”

I calculated the ACB of the Royalties Corp shares as $.12/share from information given. I believe that needs to be deducted from the ACB of the original GBR shares.

1) What should the initial ACB of the Royalties Corp shares be listed as?

2) It appears that the arrangement was set up so that one share of Original GBR was re-distributed as 1 share of New GBR + .25 share Royalties Corp. Is the conversion from Original GBR to New GBR considered a deemed disposition in my taxable account?

Pete,

It appears that there will not be any immediate deemed disposition/capital gain in most cases:

https://greatbearresources.ca/site/assets/files/3835/management_information_circular_april_23_meeting.pdf

“A Resident Holder who exchanges GBR Shares for New GBR Shares and Royalties Corp Shares pursuant to the Arrangement (the “Share Exchange”) will be deemed to have received a taxable dividend equal to the amount, if any, by which the fair market value of the Royalties Corp Shares distributed to the Resident Holder pursuant to the Share Exchange at the time of the Share Exchange exceeds the “paid-up capital” (as defined in the Tax Act) (“PUC”) of the Resident Holder’s GBR Shares determined at that time. Any such taxable dividend will be taxable as described below under “Holders Resident in Canada ‒ Taxation of Dividends – New GBR Shares and Royalties Corp Shares”. However, the Corporation expects that the fair market value of all Royalties Corp Shares distributed pursuant to the Share Exchange under the Arrangement will not exceed the PUC of the GBR Shares. Accordingly, the Corporation does not expect that any Resident Holder will be deemed to receive a taxable dividend on the Share Exchange.

A Resident Holder who exchanges GBR Shares for New GBR Shares and Royalties Corp Shares on the Share Exchange will realize a capital gain equal to the amount, if any, by which the fair market value of those Royalties Corp Shares at the effective time of the Share Exchange, less the amount of any taxable dividend deemed to be received by the Resident Holder as described in the preceding paragraph, exceeds the “adjusted cost base” (as defined in the Tax Act) (“ACB”) of the Resident Holder’s GBR Shares determined immediately before the Share Exchange. Any capital gain so realized will be taxable as described below under “Holders Resident in Canada ‒ Taxation of Capital Gains and Capital Losses”.

The Resident Holder will acquire the Royalties Corp Shares received on the Share Exchange at a cost equal to their fair market value as at the effective time of the Share Exchange, and the New GBR Shares received on the Share Exchange at a cost equal to the amount, if any, by which the ACB of the Resident Holder’s GBR Shares immediately before the Share Exchange exceeds the fair market value of the Royalties Corp Shares as at the effective time of the Share Exchange.”

This can be inputted into AdjustedCostBase.ca as follows:

1. Return of Capital for GBR with a total amount equal to the fair market value of the Royalties Corp shares received at the time of the exchange. If this fair market value exceeds your ACB of GBR then the ACB of GBR will be reduced to $0 and you will incur a capital gain based on the difference in values. Otherwise, there will be no capital gain incurred.

2. Buy Royalties Corp shares for an amount equal to the fair market value of the shares at the time of the exchange.

I hold the same mutual fund (Renaissance Diversified Income Fund) in an RRSP and LIRA. January 2021 statement shows 12 entries saying “RTN OF CAPITAL YEAR END VALUE” and there is an amount next to each entry. However, if ROC is supposed to be distribution of cash or reinvested into other units, that is not shown on the statement. My cash balance did not go up and the number of units held did not go up. So, what’s the point of these 12 entries? What purpose do they serve? Shouldn’t the total of those 12 entries be reflected by an increase in my cash balance or by an increase in the number of units held? I am very confused. Please help. Thanks.

Minoo,

I can’t say for sure but I suspect this is just an informational entry rather than an actual transaction involving cash or shares. This amount may be the total amount of return of capital from other distributions throughout the year.

What date should be used when entering ROC transaction. On the details of my T3 slip, there are two dates – record date and payable date.

Hira,

The record date should be used.

Re: Record date and Payment date for USD investments.

I just realized that when I import ROC entries using your wonderful tool they are dated for the record date so that amount is converted to CAD$ using the Fx rate for that date.

However when I enter the cash entry for that same payment (for the US Dollars received) I use the payment date and that is converted to CAD$ using that date’s Fx rate.

Given that these two dates are often more that two weeks apart there will almost always be a difference in those two rates. Should I be concerned about this?

Lisa,

I’m not sure whether it is better to use the exchange rate on the record date or the payment date, but I would suggest being consistent between these two transactions. If you decide to go with the payment date, then you could temporarily change the date to the payment date, lookup the exchange rate, and then switch the date back to the record date.

If an actual currency exchange occurs (that is, if the distribution is converted when it is deposited into a Canadian dollar account) then I would suggest using the exchange rate that was applied.

Re: Return of Capital

I understand that RoC has no tax consequences, and can be used to lower Total Cost and thus ACB/unit.

I am confused, however, as to the correct way of calculating Total Cost and thus ACB/unit if I choose instead to buy more units.

Please tell me which of the following scenarios is correct. Each comes from what I consider to be a reliable source! In each scenario the final ACB differs from any other scenario.

SCENARIO 1

I use the RoC amount directly to purchase additional shares.

So Total Cost goes up, Total # Units goes up, ACB/unit goes up.

SCENARIO 2

I subtract the RoC amount from Total Cost.

So Total Cost goes down.

Then I purchase additional units with the same amount.

So Total Cost goes back up to what it was, Total # Units goes up, so ACB/unit goes down.

SCENARIO 3

I subtract the RoC amount from Total Cost.

So Total Cost goes down.

Then I add the number of units that the RoC amount covers.

So Total Cost goes down, Total # Units goes up, so ACB/unit goes down.

Pauline,

Scenario 2 is correct.

I would suggest thinking about this as two steps: a distribution followed by a reinvestment. In practice, often only a portion of the distribution is designated as return of capital. And if the distribution is only reinvested in a whole number of units, then only a portion of the distribution may get reinvested. So the return of capital doesn’t always negate the reinvestment, and you may end up with a net change in total ACB.

If I read “Total Cost” for what you call “total ACB” at the end, I understand all that you have explained.

THANK YOU!

Hello,

If a distribution is 100% ROC, and the entire amount gets reinvested every month, does ACB always remain the same ? Would this mean you would never have to pay any tax ?

If a distribution is 90% ROC, and the 90% gets reinvested, is ACB reduced by this amount ?

Thank you.

Cassandra,

Yes, if a distribution is 100% ROC and the entire amount is reinvested, then there will be no net change in total ACB. However, I would suggest thinking about the ROC and reinvestment as two separate events because:

– Often only a portion of a distribution is considered ROC.

– Sometimes only a portion of a distribution is reinvested (such as when only a whole number of shares can be purchased)

Thank you very much.

I have a $100,000.00 investment that pays $1,000.00 per month in a distribution which is 100% ROC.

If I reinvest the whole $1,000.00 every month for one year, and assuming that the share value is the same as at the time of purchase if I decide to sell, does that mean ACB will never change, meaning there is no capital gains tax or any other tax owed ?

Cassandra,

In that scenario your total ACB remains the same but your ACB per unit would decrease due to the reinvestment in additional units. So if the price remained exactly the same you would incur a capital gain when selling.

However, I think the situation you’re envisioning is more nuanced. All else being equal, the unit price should theoretically fall by an amount equal to the amount of the distribution after the ex-dividend date. So assuming that the market valuation remains constant, the share price will drop.

To give a numerical example, suppose you buy 100 units at $10/unit, for a total ACB of $1,000 initially. If the investment incurs a distribution of $1/unit (entirely ROC) then your total ACB drops to $900 but then increases back to $1,000 as a result of the reinvestment. The unit price drops to $9 as a result of the distribution and 11.11 additional units are purchased at $9/unit. Your ACB per unit becomes $9/unit, resulting in capital gain of zero if you sell for the new market price of $9.

Thank you very much for your time and explanation, I appreciate it.

Return of Capital for Canadian Securities Trading in USD

Just realized I have erred in entering ROC calculations for WIR.U with this fantastic ACB calculator.

Though it’s a Canadian security, it traded in USD before being bought out by a private firm last year.

I had been entering the ROC information provided by CDS (in USD) rather than the numbers from the CRA which are already conveniently converted to Canadian dollars with the annual average conversion rate. I use the day of purchase currency exchange rate (because my accountant started the process years ago). I just realized there’s no currency button on ROC for my shares. So, I’ll go back a few years, readjust and make a T1 adjustment if necessary.

I gather this wasn’t factored into the programming because for US or other foreign securities, ROC is moot – fully taxed on receipt?

Chris,

Any monetary amounts that you input into AdjustedCostBase.ca should be either already converted into Canadian dollars or specified in a foreign currency along with an exchange rate. And yes, you cannot specify an exchange for Return of Capital transactions so you’ll need to first convert the amount yourself.

Some funds and trusts including WIR.U issue distributions in US$ and in some cases they also report their tax information in US$. In these instances you’ll need to convert any return of capital amounts into CA$.

In some instances like in the case of WIR.U, trusts make distributions in US$ even though they are Canadian-domiciled. For US-domiciled funds, all distributions should be taxable as foreign income, as you’ve pointed out. This is the case even if the distributions are considered to be the equivalent of return of capital, capital gains, etc. by the foreign jurisdiction.

Hello,

Re 2021 tax season; I held 300 shares of ZAG.TO between March and July and sold for a profit of roughly $22.

After entering 15.87052 ROC per month from the Statement of Trust Allocations and Designations spreadsheet, the ACB report shows a Capital Gain of $4,761.16/mo. for 3 months (Apr, May and Jun) with a Grand Total Capital Gain (2021) of roughly $19K.

Is there something incorrect here?

Thanks for your help!

Regards,

Jeremy

Jeremy,

BMO reports its distribution tax breakdown for its ETFs in percentages of the total distribution amount, rather than monetary amounts for each component. The 15.87052 value actually means 15.87052%. The “Calculation Method” field specified on the spreadsheet is set to “Per Cent”. If you multiply that percentage by the total cash distribution amount of $0.04 you get $0.0063482 per month, or $0.076178 for the full year (in this particular case the distribution amounts and tax breakdown values are the same for each month throughout the year).

When inputting Return of Capital transactions into AdjustedCostBase.ca you should therefore use a per share amount of $0.0063482 for each distribution.

Thank you for your help!!

I hope you can help. I owned units in WPT Industrial REIT which was acquired by Blackstone in 2021.

At the end of 2020, my ACB for my units in WPT REIT was $10,480.67.

My 2021 T3 in box 42 shows a ROC of $4,557.56. (The 2021 T3 also show capital gains of $7,546.55 and foreign income of $936.16 but I do not believe these numbers are important when calculating the capital gains on the forced disposition of my units).

My 2021 T5008 (and my TD trading summary for 2021) shows the proceeds of disposition for the WPT REIT as $3,014.82

If I understand your blog correctly, my new ACB would be $10,480.67 – $4,557.56 which equals $5,923.11

So my gain/loss would be $3,014.82 – $5,923.11 which equals -$2,908.29 (or a capital loss of $2,908.29).

But the T5008 shows an ACB of $10,483 NOT $5,921.21.

It looks like the T5008 is showing the ACB from 2020. I suspect the $10,483 is just a rounding error. In other words, It looks like the T5008 does not take into account the 2021 ROC (Box42) on the 2021 T3.

Am I missing something? Or is the T5008 just wrong.

P.S. Since I bought WPT REIT in 2020. My ACB calculations should be VERY easy.

2021 ACB = cost of acquiring the units in 2020 – 2020 ROC – 2021 ROC.

I double checked my numbers. I am convinced that the ACB is just wrong on the T5008 since it does not take into account the 2021 ROC shown in box 42 of the 2021 T3 slip.

Lesson learned. Do not count on the CRA or TD Waterhouse on calculating the correct ACB!

Rob, You are correct on both counts. I had the same idea after my tax forms arrived. My T5008 was recently amended by my broker, Qtrade.

“ The acquisition proceeds for 2021 T5008 tax slips were reported as $20.89 per share. The company later announced that only $4.214 per share would be treated as the acquisition price proceeds for Canadian tax purposes. This would have resulted in an over reporting of capital gains in your T5008 tax slips.

We have cancelled the redemption that was processed at $20.89 per share and reprocessed at $4.214. ”

This is why you ALWAYS want to do your own calculations!

Rule of thumb: T5008 should never be used to calculate your ACB.

Turbotax shouldn’t give the option to use it as a tax form.

CRA uses it as a record of a security transaction occurring – a reporting requirement of security exchanges.(It will miss Return of Capital or reinvested capital gains dividends from ETFs.)

I use it to double check that I have recorded all my capital gains/losses.

Also, a T5008 will not capture the transfer of securities from non registered account to a registered account such as a TFSA or RRSP. The premium service from Adjustedcostbasis.ca is worth the cost.

Rob,

I can’t verify your calculations without further details such as the number of units of WPT you held, but I can share some details about the tax treatment of the acquisition of WPT Industrial REIT by Blackstone in 2021. When WPT Industrial REIT was acquired in October, 2021, unitholders received US$22.00 per unit. Some details on the tax treatment are available here:

https://s24.q4cdn.com/499711848/files/doc_downloads/2021/10/Tax-Guidance-in-Connection-with-October-2021-Acquisition.pdf

In particular:

– A special distribution paid by the REIT in the amount of US$1.11 per REIT Unit (the “Special Distribution”).

– A distribution paid by the REIT in the amount of US$16.676 per REIT Unit (the “Final Distribution”).

– Proceeds of disposition resulting from the sale of each outstanding REIT Unit to the purchaser of REIT Units, in exchange for an amount equal to US$4.214 per REIT Unit (the “Unit Acquisition Price”)

For Canadian federal income tax purposes, the Consideration is expected to be treated as follows:

– The Special Distribution of US$1.11 per REIT Unit is considered to be a distribution of trust income.

– The Final Distribution of US$16.676 per REIT Unit is considered to consist of capital gains realized by the REIT in connection with the Transaction and a return of trust capital.

– The Unit Acquisition Price of US$4.214 per REIT Unit is considered to be proceeds realized on the disposition of REIT Units.

These figures have been converted into Canadian dollars for the purposes of adding the applicable transactions in AdjustedCostBase.ca.

The “Special Distribution” of US$1.11 per unit is equivalent to CAD$1.36851 per unit based on the exchange rate reported by the Bank of Canada at the time of the distribution. It does not impact your ACB or result in capital gains because it is taxable as 100% foreign non-business income (though this amount should be reported on your T3 slip).

The “Final Distribution” of US$16.676 per unit is equivalent to CAD$20.59528 per unit. It is taxable as CAD$7.56790 return of capital and CAD$13.02738 capital gains. If using the streamlined import features available to AdjustedCostBase.ca Premium subscribers, these transactions should get added when you import the data.

Finally, you’re deemed to have disposed of your units for US$4.214 per unit or CAD$5.20 per unit. You’ll need to input a “Sell” transaction for this amount on AdjustedCostBase.ca to represent this disposition, and it will result in a capital gain or loss (unlike the return of capital/capital gains transactions, this transaction needs to be added manually even if importing the tax data).

Thanks for all the comments.

Here are some more details pricing that the T5008 and the Trading Summary from TD Waterhouse is just plain wrong.

Dec 16, 2020 bought 580 shares of WPT REIT for $18.09 CAD plus $9.99 CAD commission.

Dec 16, 2020 ACB = $10,502.19 CAD

2021-01-05 ROC = $21.52 CAD

2021-01-05 ACB is now = $10,480.67 CAD

2021-10-22 Brookfield buys WPT REIT.

ROC shown on T3 = $4,557.56 CAD

So Final ACB should be $10,487.67-$4,557.56 or $5,923.11 CAD

But T5008 show the ACB as $10,483.00 CAD

The ACB is completely wrong. Looks like the ACB on the T5008 is the ACB BEFORE taking into account the big ROC received as part of the Brookfield acquisition. (YD even messed up that calculation!)

The proceeds of disposition shown on my Portfolio statement and on the Trading Summary is $3,014.82 CAD.

So the gain/loss is 3,104.83- $5,923.11or -2,908.29 CAD. (i,e, a loss of $2,908.29 CAD).

My T3 also shows a huge capital gain and significant foreign income. If you combine the capital gain and the foreign income on the T3 with the capital loss calculated above, I made over $5,500 CAD.

Bottom line. Do not trust the T5008.

P.S. I checked online to see if TD Waterhouse has issued a new T5508. It has not.

Rob,

Your calculations look correct. I got very similar numbers (not exactly the same, but there can be some variance depending on what US$ exchange rates you use). There can be many reasons for why a T5008 can be incorrect, and in particular I wouldn’t put much faith in it for cases involving complex corporate actions such as this.

This is the first year that I have a ROC for one of my equity index funds. This amount is found on my T3 slip, but I cannot find any transactions in the monthly statements related to ROC. So, I assume that I would just enter a ROC transaction for the amount reported in box 42. The T3 slip shows which fund that the ROC is for. There is no date and since there are no transactions listed in the statements I used Dec 31 2022 as the date. Is this correct?

Also, when you sell a fund that has a ROC does the fund company report the correct amount on the T5008 slip? Cost or book value and Proceeds of disposition or settlement amount. Or do I need to use my own ACB calculations?

I found this process for my ETF’s less confusing as I use the premium service and was impressed by how easy the import of tax information was for my ETF’s.

Cameron,

If you’ve imported the tax information for the fund, there is no need to manually input return of capital transactions. You only need to input purchases (including DRIPs) and sales.

In some cases you can get the correct result by creating a single aggregate Return of Capital transaction for the entire amount for the year. But if you’ve sold units at any point during the year, the resulting capital gain or loss and ACB may not be entirely accurate. T3 slips and transaction records don’t always provide you with sufficient information.

I own a high interest savings ETF in a non-registered account (i.e. CASH.TO) and I’ve been trying to do the ROC calculation but I am a little confused.

On Horizons website they list the ROC distribution as 0.1341 per unit for ROC or 11.66% on a percent basis for 2022.

For one of my monthly transactions, let’s say I have 1313 units of CASH.TO and my total dividend for that month was $182.77. Out of that $182.77, $150.27 was reinvested as part of DRIP program. So if I calculate ROC using the percent I get $182.77*11.66%=$21.31. However, if I calculate ROC using per unit distribution I get 1313*0.1341=$176.07. The two ROC calculations are way off. What am I missing? Is the distribution per unit provided by Horizons on an annual basis and I’m applying it on a monthly?

Milos,

The $0.1314/unit return of capital amount is an annual total, whereas the $182.77 amount (corresponding to $0.13920/unit) is a the total cash distribution amount for one particular month (September, 2022). So you are comparing the return of capital for an entire year with the return of capital for a particular month.

In general, the tax breakdown for distributions is not necessarily the same from month to month. One month may have a higher or lower percentage allocated towards return of capital than another month in the same tax year. So it may not be completely accurate to estimate return of capital by applying a fixed percentage to each distribution throughout the year, if you have purchases and sales throughout the year.

But CASH.TO does have the same percentage allocated towards return of capital for every month in 2022. So for the September, 2022 the return of capital amount would be $0.13920/unit x 11.66% = $0.01624/unit, or $21.32 for 1,313 units.

Thanks so much for the response, it’s clear now.

Is there an easy way to tell when a stock or ETF will have a constant distribution breakdown on annual basis versus when it will vary period by period? For example, for CASH.TO I looked at the Horizon website and they just provided an annual distribution summary and in the prospectus it just says distributions are made on a monthly basis but I couldn’t find anything stating specifically that it l’s constant for a year nor any monthly distribution summary.

Milos,

There is not always a simple way to obtain the necessary tax breakdown information. In some cases it may be available on the fund provider’s web site. Your brokerage may provide a detailed record of tax allocations on a per-distribution basis.

For general guidelines on obtaining this info, please see the following:

https://www.adjustedcostbase.ca/blog/tax-breakdown-service-for-etfs-and-trusts-from-cdsinnovations-ca/

https://www.adjustedcostbase.ca/blog/streamlined-import-of-return-of-capital-and-phantom-distributions-and-for-exchange-traded-funds-etfs-publicly-traded-mutual-funds-and-trusts/

Another BMO ETF here. Trying to figure out the return of capital.

ZWC – BMO Canadian High Dividend Covered Call ETF

This dividend pays a monthly dividend, and the amount for return of capital according to the CDS Innovations file shows 59.47215 per month. Is this an amount or a percentage? I’m confused as to what number I would enter for the return of capital.

Thank you! This is an amazing site!

Marc

Marc,

BMO usually reports their distribution amounts by percentage. You can refer to the “Calculation Method” field in the spreadsheet to confirm. In this case 59.47215% of the distribution is allocated as return of capital. You would need to multiply this percentage by the total distribution amount to convert this into a dollar amount.

Thank you for your response! So then obviously I would put that amount in the field as opposed to trying to figure out a ‘per share’ amount?

Marc,

Only the monetary amount should be inputted into AdjustedCostBase.ca (not the percentage). You can add a “Return of Capital” transaction with a per share amount equal to the percentage multiplied by the total dollar amount of the distribution.

Thank you very much for your replies!

If you reinvest a 100% ROC distribution every time you receive one, and continue to do this in perpetuity without ever selling, would you never pay any tax ? Thank you.

Cassandra,

A distribution consisting entirely of ROC would generally not be taxable regardless if whether the cash is reinvested.

The only scenario where reinvesting the distributions would have an impact is in the case where the aggregate ROC accumulates to such a large amount that your ACB would otherwise drop to zero without the reinvestment.

Thank you for your reply.

Just to clarify, if the ACB never got to zero, and the stock was never sold, there would never be any tax payable ?

Thank you.

Cassandra,

Yes that’s correct in theory.

I’m afraid I’m still confused about ROC and how it impacts adjusted cost base for my USD.