SimpleTax is a web-based tax software application that allows Canadian taxpayers to complete and submit tax returns online. It’s one of the few tax software packages that’s offered for free (it has a “pay what you want” pricing policy). It’s fairly easy to use and doesn’t take long to sign up. Since it’s web-based, you can access and work on your tax return from anywhere.

To use SimpleTax, visit their web site and you can start working on a tax return right away. SimpleTax provides help and support documentation on their web site, so detailed instructions about this will not be provided here. Here we’ll discuss how to transfer your adjusted cost base and capital gains information from AdjustedCostBase.ca into SimpleTax and use the two tools together.

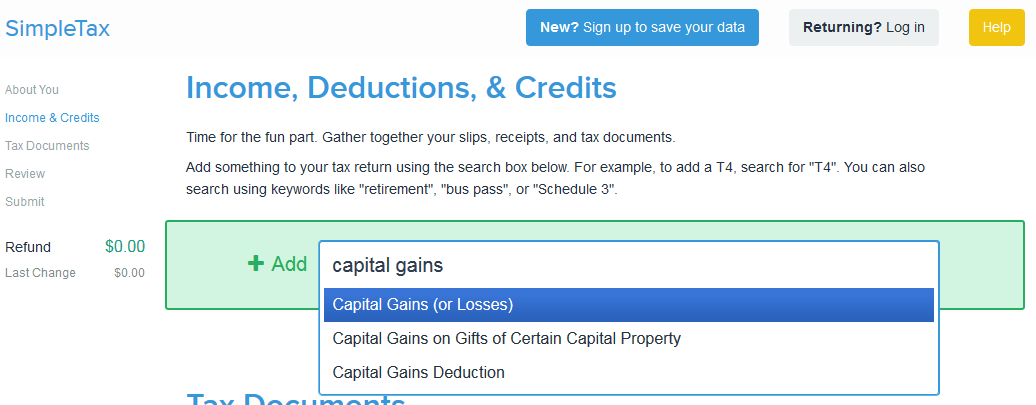

To begin entering the information into SimpleTax, first you’ll need to pull up the “Capital Gains (or Losses)” form. To do so, search for “capital gains” in the “Add” box inside the “Income, Deductions, and Credits” section as follows:

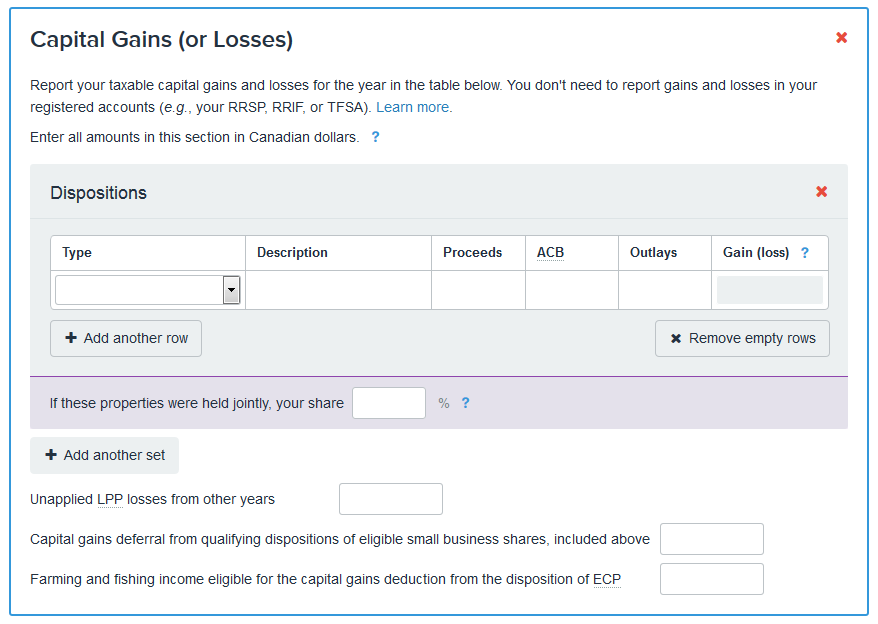

You’ll then see a blank “Capital Gains (or Losses)” form:

SimpleTax allows you to enter dispositions in different “sets.” This can allow you to apply a percentage share to multiple dispositions when properties are held jointly. But in these instructions we’ll assume the securities in question aren’t jointly owned, and a single set will be used.

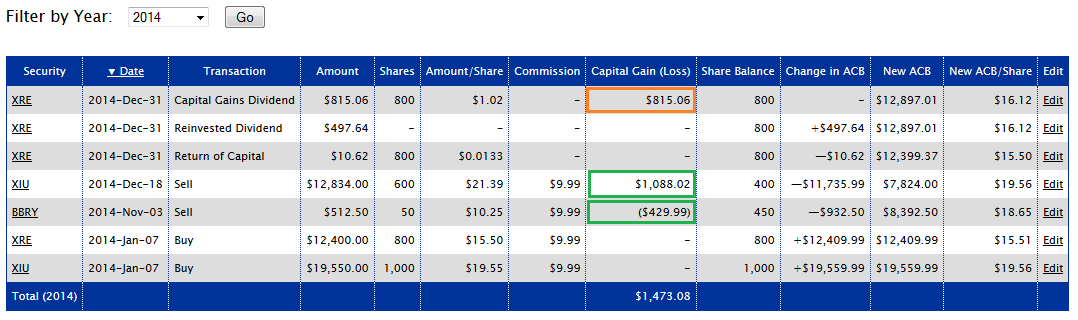

You can view a list of your transactions for the year on AdjustedCostBase.ca by clicking on “View All Transactions” and using the “Filter by Year” function. First, let’s assume that the following transactions took place during the 2014 tax year and have been recorded into AdjustedCostBase.ca:

When completing your tax return, you only need to focus on the transactions resulting in capital gains or capital losses for the tax year in question. The relevant transactions that have implications for the 2014 tax year are highlighted above and are as follows:

- Sell 50 shares of BBRY with a capital loss of $429.99

- Sell 600 shares of XIU for a capital gain of $1,088.02

- Capital Gains Dividend for XRE totaling $815.06

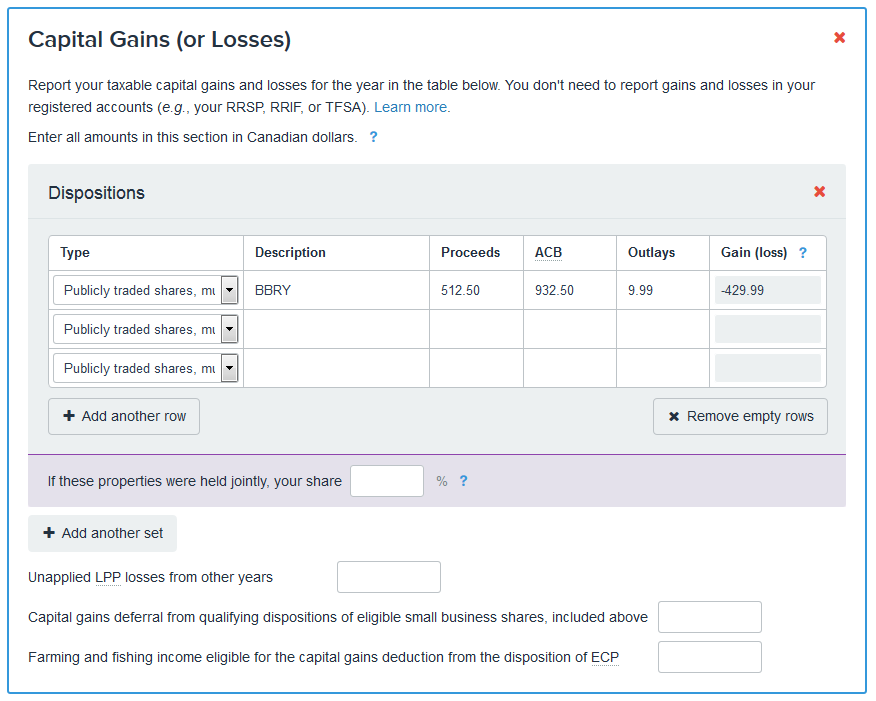

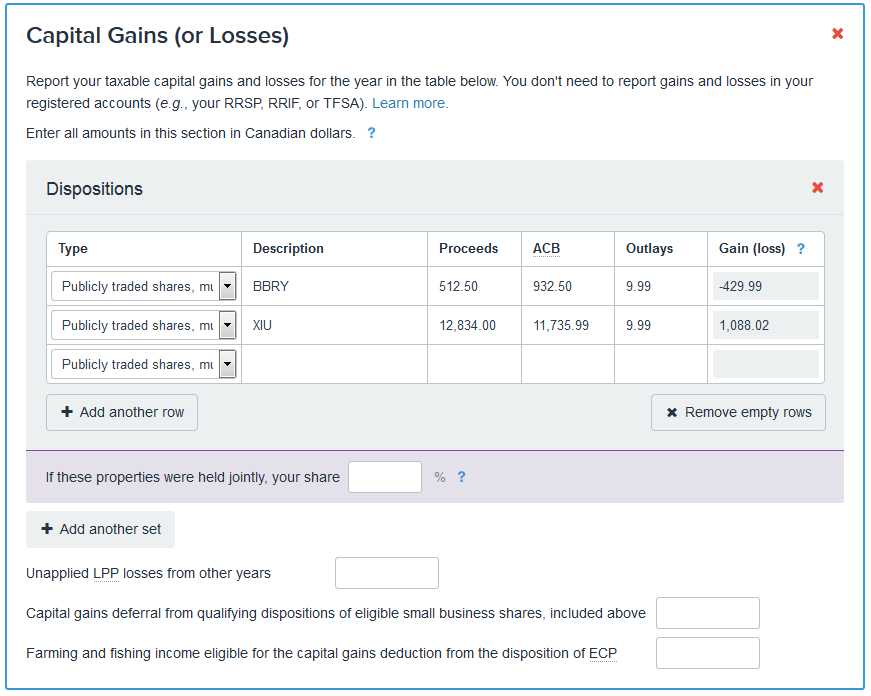

Now we can begin transferring this information into SimpleTax. All these securities are publicly traded shares so for all entries select “Publicly traded shares, mutual fund units, deferral of eligible small business corporation shares, and other shares” as the type.

Starting with the BBRY transaction, input “BBRY” as the description (or any other identifying text as you see fit). Next enter the amount from the sale transaction of $512.50 into the “Proceeds” column (this amount excludes the $9.99 commission). Next, the “ACB” column corresponds to the total adjusted cost base of the shares that were sold. This can be found by looking at the “Change in ACB” column from the transactions list on AdjustedCostBase.ca. In this case the amount is $932.50. Note that it’s shown as —$932.50 because the total ACB for BBRY is reduced by $932.50 as a result of this transaction. But the positive value should be inputted into the “ACB” column on SimpleTax. Therefore, enter $932.50 in the “ACB” column. Finally, the “Outlays” box should be populated with the commission, if applicable. In this case it’s $9.99. After entering all this information, the SimpleTax “Capital Gains (or Losses)” form should appear as follows:

Note that the capital loss is $429.99 is computed automatically by SimpleTax (it does not need to be inputted). As a sanity check, this value should match the capital gain (or loss) reported by AdjustedCostBase.ca (there may be a slight discrepancy due to rounding errors).

Next, we can add an entry for the sale of 600 XIU shares. In this case, put “XIU” as the description, $12,834.00 as the “Proceeds”, $11,735.99 as the “ACB” and $9.99 for “Outlays.” The form should now appear as follows:

Once again SimpleTax’s computed value for the gain of $1,088.02 matches the value computed by AdjustedCostBase.ca.

Finally we have the “Capital Gains Dividend” of $815.06 transaction for XRE. However, this transaction should not be included in the “Capital Gains (or Losses)” form. The reason for this is that the capital gain distribution should appear on the T3 slip you get from your brokerage. T3 slips values are entered elsewhere in SimpleTax. It’s important not to enter this amount twice or you’ll be overpaying taxes.

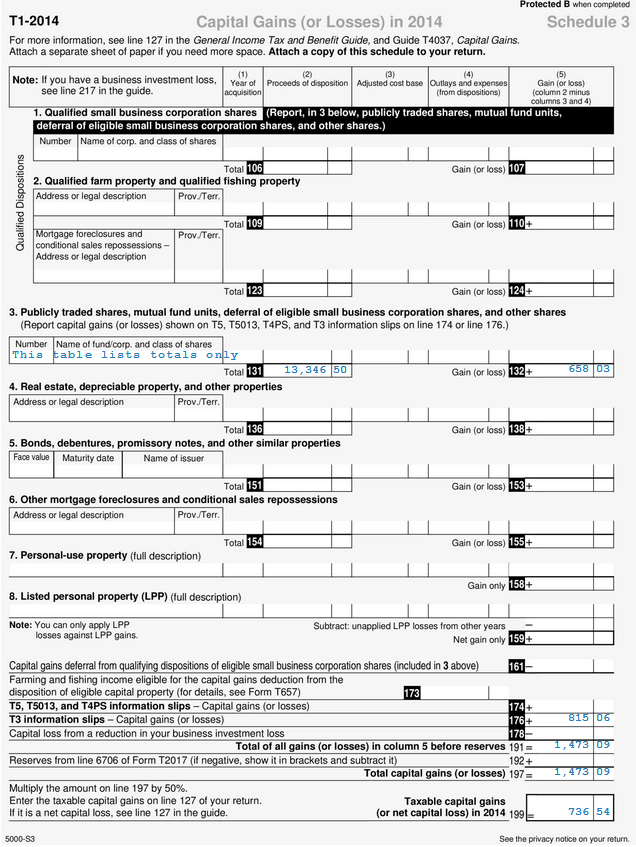

SimpleTax allows you to view all your completed tax forms at any point. In the “Tax Documents” section you can click on “Schedule 3” to see the completed version of the “Capital Gains (or Losses)” document that makes up part of your tax return. For this example, this is what it looks like:

Assuming that you’ve entered the $815.06 capital gains dividend as part of your T3 slip for XRE, the total capital gains should match between AdjustedCostBase.ca and SimpleTax (there may be a tiny discrepancy due to rounding).

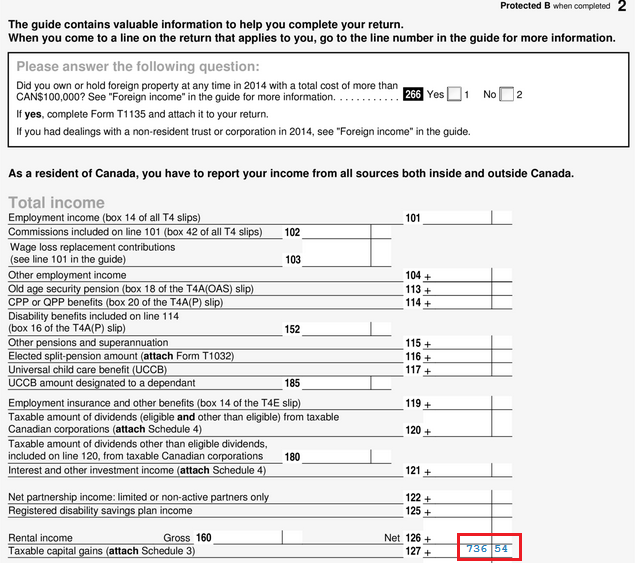

Finally, when you view line 127 on the T1 form, the value should be directly transferred over from line 199 of Schedule 3 (note that this value is half of the total amount of capital gains since capital gains are 50% taxable):

Hello,

Thanks for using the example with SimpleTax.

I would like to ask that you extend the example further, buy looking at multiple sell transactions for the same security. So, using your example of XIU, how would you input the disposition and ACB into SimpleTax when you have sold it multiple times? Do you just aggregate the total disposition and ACB or do you list each separate sell transaction of XIU as a separate disposition in SimpleTax.

Thanks for your help.

When you have multiple dispositions of the same security in the same year, you could either list them as separate entries or combine them into a single entry. With separate entries, the process would involve repeating the steps above. To combine the dispositions into a single entry, you would simply enter the total amount from all dispositions for each column (proceeds, ACB, outlays, and gain/loss). The result should be the same with either method.

What happen when we buy and sell Yahoo which is in USD?

should there be an entry for USD as a security?

Can u provide an example

Jason,

You can find an explanation and an example here:

http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-foreign-currency-transactions/

If you’re asking about which category to use for Schedule 3 for foreign currency, there isn’t really one that seems completely appropriate, so I would go with “Publicly traded shares, mutual fund units, deferral of eligible small business corporation shares, and other shares”.

I am getting quite confused, DO we need to report the currency as capital gain/loss?

According to your site, we are supposed to do the following

1. Buy 100 shares of Yahoo at $100, resulting in USD10K (ignore commission to simply calculation), recording the transaction as Canadian dollar (rate 1.30), which is 13000 Canadian.

2. Sell 10K of USD, and recording the transaction as $13000 Canadian.

3. Sell 100 shares of Yahoo at $101, resulting in USD$10100, exchange is now at 1.31, which resulting in 13231 Canadian. Profit is $231 Canadian.

4. Brought US$10100, resulting in $13231, Canadian, profit is $231.

5. Withdraw US$1000 for vacation, rate is now 1.32 ( I will expect to pay tax on that)

It seems 2 and 4 are redundant, resulting in paying tax twice. However, how do we account for #5

Jason,

For #2, there would potentially be a gain or loss for US dollars, assuming that you used US cash to purchase the stocks, as opposed to using Canadian dollars that are immediately converted.

For #4, this is a purchase, not a sale, so there isn’t any realized gain or loss.

For further information on dealing with capital gains and losses in foreign currency cash, please see the following:

http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-for-foreign-currency-cash/

You are right. I’m treating USD as if they’re just security. In #2, the shares are negative, and I’m assuming it is a short sell. Of course, this is not true, a negative shares will mean the fund is borrowed, which will actually reduce the profit, right.

Another reason we cannot relied on brokerage to provide us with accurate ACB.

Jason,

Normally transactions involving shorting aren’t considered to be on capital account. But if you’re buying shares in a capital account transaction with borrowed funds in US dollars, you may be able to actually couple the foreign currency gain or loss together with the gain or loss on the shares to determine a capital gain or loss. See the following comment:

http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-foreign-currency-transactions/#comment-81348

I understand that too. When I do some more thinking about that, we can actually treat USD as short sell (though shorting aren’t considered). For example

Brought 400 shares of GPRO at $50 at 1.3. ACB = 400 *50 * 1.3 = C$26,000

Sold 400 shares of GPRO at $51 at 1.4 exchange rate. ACB = 0, profit = C$520

Corresponding USD transaction

Sell US$20,000 at 1.3, ACB = -C$26,000, shares = -20,000

Brought US$20400 (51* 400) at 1.4 exchange rate = 28560. shares = 400, ACB = 2560, loss=

previous acb * (shares/total shares) – shares * price * rate

= 26000 * (20400/20000) – (20400 * 1.4)

= 26500 – 28560

= – 2060

That is, we are actually losing money in this transaction, we loss 2060-520 = 1540

Is this correct?

Jason,

The capital gain from the shares is:

(400 shares x USD$51/share x 1.4 CAD$/USD$) – (400 shares x USD$50/share x 1.3 CAD$/USD$)

= CAD$2,560

The loss incurred due to the borrowed funds is:

(USD$20,000 x 1.4 CAD$/USD$) – (USD$20,000 x 1.3 CAD$/USD$)

= CAD$2,000

This loss is not really a capital loss on its own and ACB in general cannot be calculated for negative balances. Although the formulas for ACB appear to work in this case, in general the calculations will not be correct for cases where there are multiple purchases and/or sales. Therefore I’m referring to this value as a “loss on the borrowed funds” as opposed to a capital loss.

Applying this loss on the borrowed funds against the capital gain on the shares, we find that the net capital gain on the shares is:

CAD$2,560 – CAD$2,000

= CAD$560

This makes sense because CAD$560 is the final balance you would have in your account after selling the shares, paying down the borrowed funds, and converting the remainder in CAD$.

If entering these transactions on AdjustedCostBase.ca I would suggest entering the $2,000 loss as a commission.

if there is no change in the price

(400 shares x USD$50/share x 1.4 CAD$/USD$) – (400 shares x USD$50/share x 1.3 CAD$/USD$)

= CAD$28000 – $26000

= 2000

(USD$20,000 x 1.4 CAD$/USD$) – (USD$20,000 x 1.3 CAD$/USD$)

= CAD$2,000

the net effect is zero. Interesting.

By the same token, if the exchange rate goes down from 1.4 to 1.3, we will have

(400 shares x USD$50/share x 1.3 CAD$/USD$) – (400 shares x USD$50/share x 1.4 CAD$/USD$)

= -2000 (capital loss)

borrowed funds

(USD$20,000 x 1.4 CAD$/USD$) – (USD$20,000 x 1.3 CAD$/USD$)

= CAD$2,000.

Net effect is again zero, did I miss something, I would expect when I borrowed fund and the rate goes down, I would pay less (in Canadian).

Jason,

That’s correct. Through the ownership of the US shares, you’re long on the share price as well as US dollars. By borrowing US dollars, you’re short US dollars, so the long and the short position cancel each other out. You’re essentially hedging your exposure to US dollars, so that the gain or loss depends only on the price movement of the shares.

From my broker i received a T5008 statement that lists each security i sold only once, with box 21 filed (but not box 20). And a T5008/Trading Summary which lists each Buy and Sell and provides Quantity of Securities, Price and Proceeds of Disposition or Settlement Amount.

I have calculated my ACB but am still very confused about how to complete my tax return!

I’m using Simple Tax which is why i’m posting on this thread.

If i follow your recommendation, does that mean i don’t need to use the T5008 section of Simple Tax, and only use the Capital Gains section? (Forgive me for being dense, because there is something in Simple Tax that says something along those lines, but I don’t see how this works at all, and for the life of me i’m going mental.)

I thought to dabble with a few trades on $1000 – managed to loose most of it betting on a recovery on the price of oil, and now my tax return says i need to pay over $4000 in taxes based on these T5008’s It makes no sense, and i just can’t afford too!!

Ken,

SimpleTax has some further information about that here:

https://help.simpletax.ca/questions/t5008-slip

It seems that you should input the data either as a T5008 or with the regular capital gains section, but not both.

Hello,

In your response to K Rafih (Feb 17, 2015) you mentioned that it is feasible to combine multiple dispositions of the same security into a single entry. Is this also true if some of those dispositions are disallowed losses per the superficial loss rule and the security in question has been fully sold and not been repurchased in the following 30-day period?

Example: At the start of the year 100 shares of XYZ are held worth $10/share (ACB = $1,000). Halfway through the year, XYZ drops to $5/share and 50 shares are sold. The $250 loss is disallowed because in the following week ABC rises to $8/share and 100 shares are bought (new ACB = $1550, shares = 150). A couple of months later XYZ goes out of business, share value plummets to $0.01 and all 150 shares are sold. For the sake of simplicity, let’s suppose there were no brokerage fees. What values should be entered in the Proceeds and ACB fields? I see two possibilities:

#1: Proceeds = $1.50, ACB = $1,550, Loss = $1,548.50

#2: Proceeds = $251.50, ACB = $1,800, Loss = $1,548.50

Obviously #1 and #2 yield the same loss result, but #2 seems more representative of what happened throughout the year, whereas #1 only reflects the very last transaction which by the way is quite disproportionate (potential red flag for the CRA auditors?). Are both ways of reporting capital losses correct or should #2 be avoided since a disallowed loss was involved in the calculations?

Thanks in advance.

Dan,

The CRA isn’t clear on whether superficial loss transactions should be listed on Schedule 3. I would tend to lean towards not including them, as the form isn’t really designed to properly accommodate superficial loss sales.

So in your example, I would list the following on Schedule 3:

Proceeds: $1.50, ACB: $1,550.00, Loss: $1,548.50

When including sales involving superficial losses in our Annual Capital Gains PDF Reports the ACB adjusted such that it equals the proceeds of disposition. In your example, the first sale involving the superficial loss would be listed as follows:

Proceeds: $250.00, ACB: $250.00, Gain/Loss: $0.00

Combining these two would yield the same answer as you indicated for possibility #2 above.

“When completing your tax return, you only need to focus on the transactions resulting in capital gains or capital losses for the tax year in question.”

Following this guide, my tax owed seemed suspiciously low for a mutual fund I’ve sold recently. Every year I’ve reported the annual reinvested capital gains which are typically quite low but now I’ve sold it all and according to this guide is seems as if I only have to report the gains displayed on AdjustedCostBase.ca in the past year. So for example, in 2016, a year prior to the sale when one of my reinvested capital gains was entered, my ACB was 10,500 and then when it was sold in 2017 it had an ACB of 11,000 with 500 displayed as my capital gain. I believe I’m missing something because I expected to owe a lot more for all these years I’ve held the fund. Is it because of the reinvested capital gains (and associated reporting) that I’m left with not much to report now?

Thanks!

A,

If you are calculating your capital gain by subtracting one ACB from another, that is not correct. Your capital gain is found by subtracting your ACB from the proceeds of disposition. Please see the following:

https://www.adjustedcostbase.ca/blog/how-to-calculate-adjusted-cost-base-acb-and-capital-gains/

im glad I found this website, but wow, im so confused. Don’t even know where to start.

Im with TD Canada, and wealthbar, and have investments in CAD and US accounts, as well as registered and non registered (TFSA, RSP).

I think TD has some sort of feature to calculate things, but im not sure.

Where do I start, last year I just imported the info from CRA onto simpletax using their online import tool, but for this year, thats when I started trading stocks and bonds, so what should be done differently? Some of the stocks I bought then sold a few days or weeks later, and then some re-bought.

This seems so complex im going crazy. Any suggestions? Googling this shows how you calculate cap gains for a particular transaction, but what if you have hundreds?

Panicking…

Russ,

Here is a good starting point:

https://www.adjustedcostbase.ca/blog/how-to-calculate-adjusted-cost-base-acb-and-capital-gains/

Importing data from the CRA into your tax software can work well and save a lot of time for things like employment income or investment income. However, for capital gains this is not always the best idea. The T5008 statements that brokerages use to report dispositions often don’t contain accurate adjusted cost base values. In many cases this information is missing. There are many reasons for this:

https://www.adjustedcostbase.ca/blog/can-you-rely-on-your-brokerage-for-calculating-adjusted-cost-base-and-capital-gains/

In my case, I tried importing my T5008 statements for 2018 using one of the most popular online tax software packages. As the cost base value was missing from my statements (my brokerage left it blank) the software assumed a cost base of $0 (and didn’t even present me with a warning). Had I not been aware of the issue and blindly gone ahead with the calculated values, I would have ended up paying many $1,000’s in extra taxes.

In terms of calculating ACB for a large number of transactions, AdjustedCostBase.ca requires you to input all of the transactions. However, AdjustedCostBase.ca Premium subscribers have access to a feature that allows spreadsheets to be imported. So if your brokerage allows you to download your transactions into a spreadsheet format, this could save you a lot of time. This feature is described here:

https://www.adjustedcostbase.ca/blog/importing-transactions-from-a-spreadsheet/

Hi there,

Thanks for the fast reply!

Yeah I read about the ‘not using broker data’ as its inaccurate’ thing, so are you use the transaction export will be reliable? I think TD does have a feature for this, will check.

Will your import tool also understand how to deal with the less than/more than 30 days repurchase thing, I read thats a kicker too. I’ll definately sign up for premium, as I can see that being 100% worth it. Tax Advisors have quoted me thousands, and thats probably without even doing the laborious paperwork part and counting, which they’ll probs still ask me to do.

Reason I ask about the reliability of the import is that I connected my TD account via Wealthica too, and that kept complaining about invalid transactions, even though I dont quite understand how it could be invalid.

P.s. would be great if there was a way to reply on this page without re-entering all the fields each time.

Im a senior web dev btw, so any help needed, let me know, this is a great cause you did here!

Russ,

Thanks for your comments. I believe you’re referring to the superficial loss rule:

https://www.adjustedcostbase.ca/blog/what-is-the-superficial-loss-rule/

Yes, AdjustedCostBase.ca can identify when the superficial loss rule might apply to a sale transactions in most (but not all) cases. In such cases, a warning message will appear. You will then need to apply the superficial loss rule, as described here:

https://www.adjustedcostbase.ca/blog/applying-the-superficial-loss-rule-for-a-partial-disposition-of-shares/

If you run into trouble importing a spreadsheet, please feel free to use the “Contact Us” section of this web site to send details on the exact issue you’re experiencing.

Right, sounds perfect. I’ll be doing that this Sunday then.

Is premium automated, or is it a manual upgrade (do I need to do it during work hours, or can I sign up on Sunday)

Russ,

You can upgrade anytime yourself so there will be no issue with that.

Hi Sir, I’m having a really hard time wrapping my head around this while doing the ACB. Should have never got myself into this… Anyway, I did a vertical put spread and entered (hopefully correctly) into adjustedcostbase.ca as shown, https://i.gyazo.com/eec8aaa55281827f4ed83841cbedf50d.png

I see a $235.10 capital gain, so now when I head to simpletax to enter them in, https://i.gyazo.com/624578f0f340744f1f51342d2f06e652.png I got confused as the field on “ACB” is 0, which does corresponds to adjustedcostbase.ca but the “Gain (loss)” in simpletax just isn’t correct. For reference, here’s the trade summary from Questrade, https://i.gyazo.com/496650d4a283691c4b3496e11330fcb0.png Please shred some light in what I’m doing wrong, thank you very much!

Tony,

First, all monetary amounts need to be converted into Canadian dollars when calculating ACB. This means that you should either convert the values before inputting them into AdjustedCostBase.ca or input them as US$ and also specify an exchange rate. For further information please see the following:

https://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-foreign-currency-transactions/

Also, while not very consequential in this case, I would suggest adding the SEC fees to the commission, as it doesn’t look like these fees are included in the commission in your case.

Schedule 3 is not really well designed for all scenarios, in particular for transactions involving options. For SimpleTax (or any tax software in general) one thing you can do is input the capital gain or loss into the “Proceeds” column and set the ACB and outlays amounts to $0. This will allow the capital gain or loss to correctly be accounted for and you won’t need to worry about the specific components, which are not always necessarily applicable for options transactions. The correct capital gains and losses will be reported on your tax return if you use this method.

Thank you for your reply. It seems that if I input a capital loss into the “Proceeds” column, let say -200, simpletax automatically set it to zero. But if I input 200 instead, then the “Gain (loss)” column shows a gain of 200. The only way for the “Gain (loss)” column to show a negative number is that if I input the number in the “ACB” or “Overlays” column. If this is the case, should I input any capital gain in the “Proceeds” column and any capital loss in the “ACB” column? Thanks again.

Tony,

In that case you can set the ACB to $200 and the proceeds to $0, which should give you a capital loss of $200.

Hello,

Thanks for your incredible site, very useful.

I have a question and could not find any response to clarify.

I hold many ETFs on my Margin account, but since early 2018 I have only bought ETFs and have never sold any of those.

For tax purposes, do I need to report anything else other than my T3? (Questrade, my brokerage, has not sent me a T5008 because I haven’t sold any ETF).

I have prepared the ABC for all my ETF and transaction including Buys, Capital Gains Dividends (not using DRIP), Return of Capital and Reinvested Capital Gains Distribution.

But now I am at a point that I have no idea what (if) I should enter anything on my tax application. I am using SimpleTax and was reading your instructions at your blog (https://www.adjustedcostbase.ca/blog/using-adjustedcostbase-ca-to-complete-your-tax-return-with-simpletax/) but it seems only to mention about sells.

Could you please provide some guidance? I truly appreciate.

Thank you,

Sam.

Sam,

You won’t need to report any capital gains or losses unless you’ve made dispositions during the tax year. Inputting the data in your T3/T5 slips will be sufficient in that case.

Thank you for your answering.

So to confirm, I should just keep every year doing the ACB calculation for my records, and then when I sell any securities I would use the ACB price to report gains/loss.

Is this a correct assumption?

Thank you for your help, and amazing website!

Sam.

Sam,

That’s right, you’ve got it. Thanks for sharing your feedback!

Hello Mr AdjustedCostBase.ca,

I was about to ask a question on how to input call/put options but it seems like it was already asked and answered by “TONY”!

So Id just leave another message to say thanks to this great website. This is my first time doing Tax on my own and this helped me alot!

Hello,

I noticed there is a “Add another disposition” and “Add another set”. What are the differences? I noticed on your example you used “disposition”. When should “set” be used?

Thanks.

Winchester,

At the bottom of each “set” you can specify a percentage of joint ownership for the dispositions above. So it seems that adding multiple sets allows you to set different ownership percentages for each one. If everything is completely owned by you then you can use a single set.

Hi,

Thanks so much for all the advice you give on your site!

I have a security and I’m not sure which figure to use for ACB. During the year, I’ve bought multiple times, and sold once. This is what it looks like, in chronological order for the year:

BUY 1 – ACB 1

BUY 2 – ACB 2

SELL 1 – ACB 3

BUY 3 – ACB 4

BUY 4 – ACB 5

When I report the capital gain, am I using the figure from the date of sale (ABC 3), or the final transaction of the year (ACB 5)?

Thanks!

John,

When reporting a gain or loss on schedule 3, the adjusted cost base should be populated with the ACB of the shares that were sold. This is equal to the ACB per share just prior to the sale multiplied by the number of shares sold.

Hi,

Is there a way to do a batch import in SimpleTax or do I have to enter each transaction separately? I have thousands of transactions and it seems like a real burden to input all of the transaction one by one. I’m really trying hard to find a tax software that can do some kind of batch import or a least provide me with some sort of basic template of all my transactions, so I could only have to edit some of the information on them, like the ACB for example. I’ve also tried with Turbotax, but the software doesn’t allow me to import my transactions, as I have more than 500 of them. Any luck?

Thank you

Just writing a follow up from my comment above. After having imported all of our transactions on this site and now with the proper ACB of each transaction, is there a way to add up/calculate total somehow? To make the task less painful than entering hundreds of line by line in the tax software?

Thanks again

Max,

I’m not sure if SimpleTax allows dispositions to be imported in batch, however, you could use a single entry with consolidated totals for each column.

I believe that tax software will only submit numbered values from Schedule 3 to the CRA when your tax return is filed electronically. For Schedule 3 this means that only the total of the proceeds of disposition and total capital gain/loss for each category is submitted, as opposed to the details of each transaction. So as long as the total capital gain/loss is correct it should be fine (though it is good idea to maintain your detailed records in case the CRA inquires about it).

If you go to “View All Transactions” and filter by a particular year, it will show the total capital gain or loss from dispositions for the year at the bottom of the page. As an AdjustedCostBase.ca Premium subscriber, you can also generate an annual report that shows the totals of columns that apply to Schedule 3, as described here:

https://www.adjustedcostbase.ca/blog/annual-capital-gains-pdf-reports/