The Canada Revenue Agency requires capital gains or losses and adjusted cost base for securities to be reported in Canadian dollars when the transactions are on capital account. This means that when calculating ACB, all amounts should be converted into Canadian dollars. This occurs even if you use a cash balance in foreign currency to purchase a security (as opposed to converting Canadian dollars to make the purchase) or leave the proceeds from the sale of a security in foreign currency (as opposed to converting the proceeds into Canadian dollars).

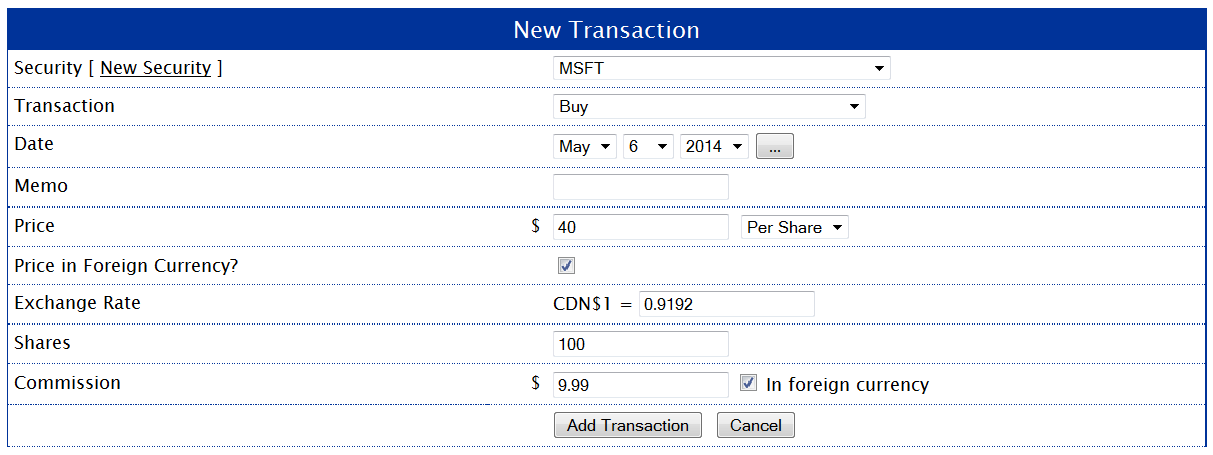

As an example, starting from a zero share balance, consider the purchase of 100 shares of MSFT for USD$40.00 per share with a commission of USD$9.99 when the exchange rate is CAD$1 = USD$0.9192. To calculate the ACB, the amount of the transaction needs to be converted to Canadian dollars. Therefore, the initial ACB becomes:

((100 shares x USD$40.00/share) + USD$9.99) / (0.9192 USD$/CAD$) = CAD$4,362.48 (or CAD$43.62 per share)

Note that when calculating ACB, the commission should also be converted to Canadian dollars. If the commission is paid in Canadian dollars it does not need to be divided by the conversion rate.

Future buy or sell transactions should be calculated using the future exchange rate. For example, suppose that in the following year 40 shares of MSFT are sold at a price of USD$50.00 per share with a commission of USD$9.99 and an exchange rate of CAD$1 = USD$1.0344. The sale results in a decrease in ACB equal to:

((40 shares) x (USD$50.00/share) — USD$9.99) / (1.0344 USD$/CAD$) = CAD$1,923.83

This results in a capital gain equal to:

CAD$1,923.83 — (CAD$4,362.48 x (40 shares/100 shares)) = $178,84

The new ACB is therefore:

CAD$4,362.48 — (CAD$4,362.48 x (40 shares/100 shares)) = CAD$2,617.49 (or CAD$43.62 per share)

All values must be converted into Canadian dollars, even if you’re using a foreign currency cash balance to make a purchase and even if you do not convert the proceeds from a sale into Canadian dollars.

The CRA permits you to use the exchange rate from the day of the transaction date, or the average annual exchange rate if multiple transactions occurred over the course of a year. If a currency exchange was involved in the transaction, you may use the actual exchange rate you received.

The Bank of Canada provides the following resource that you can use to find the exchange rate on the date of a transaction:

Bank of Canada – 10-Year Currency Converter

The Bank of Canada also provides average annual exchange rate data:

Bank of Canada – Annual Average Exchange Rates

In the case where a cash balance in a foreign currency is used to purchase shares in the same currency, the cash is deemed to be sold and converted into Canadian dollars at the time of the transaction. This may result in a capital gain or loss as a result of selling the foreign currency (see Calculating Adjusted Cost Base for Cash in Foreign Currency).

AdjustedCostBase.ca supports calculations for foreign currency for buy and sell transactions. The following illustrates how the above example can be inputted. The initial purchase of 100 shares of MSFT for USD$40.00/share with a USD$9.99 commission and a CAD$1 = USD$0.9192 exchange rate is entered as follows:

The “Price in Foreign Currency?” checkbox is checked, as well as “In foreign currency” because both the stock and the commission were priced in U.S. dollars.

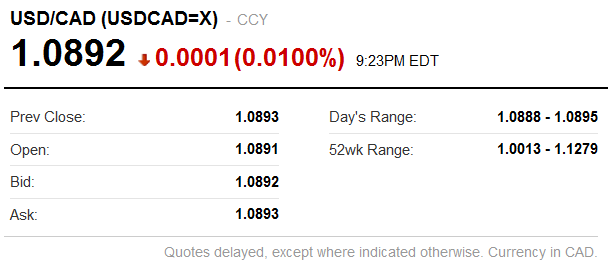

The exchange rate needs to be inputted as the value of one Canadian dollar in the foreign currency. It is important not to use the inverse of this value. If your exchange rate is provided as the value in Canadian dollars for one unit of foreign currency, the value must be inverted. For example, the following is taken from Yahoo Finance showing the exchange rate as USD/CAD (instead of CAD/USD):

In this case it shows USD$1=CAD$1.0892. This needs to be converted to the proper format: CAD$1 = 1/1.0892 = USD$0.9181.

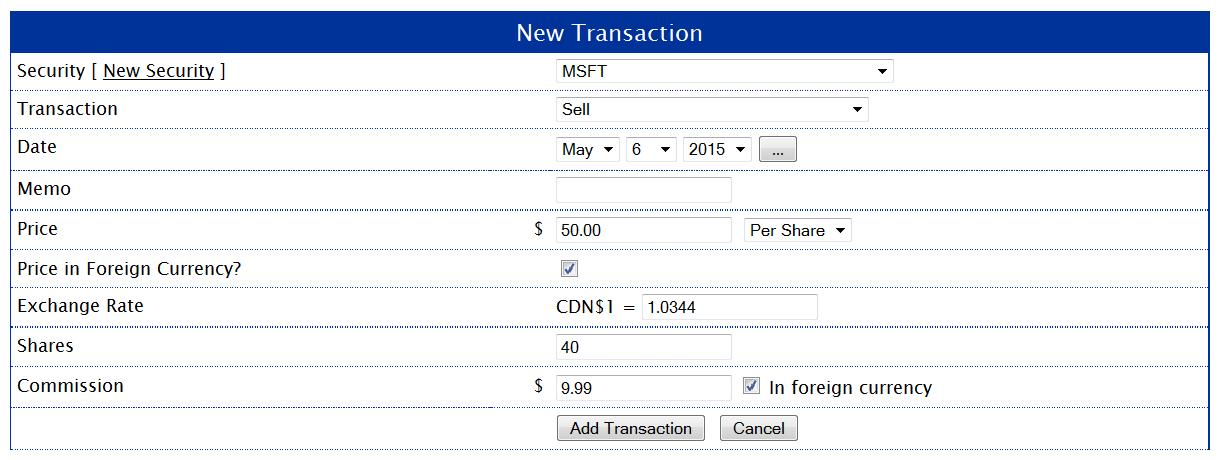

Next we enter the sale of 40 shares for USD$50.00/share with an exchange rate of CAD$1 = USD$1.0344 and a commission of USD$9.99:

Once again the “Price in Foreign Currency?” checkbox is checked, as well as “In foreign currency” because both the stock and the commission were priced in U.S. dollars. The transactions are shown below:

All the amounts are shown after they’re converted to Canadian dollars. The ACB balances and capital gain match the calculated values in the example above.

For a year with dozens of trades in volatile USD stocks, what is the easiest way to determine whether to use daily foreign exchange rate or the annual average rate?

Whichever rate is chosen, should the rate be entered in each Security transaction or just applied to the total capital gains/loss for the year when filing tax return?

Bankofcanada.ca site lists CDN-USD average rate of 1.10446640 for year 2014. Should this value or the inverse value of 0.90541460 be used in the adjustedcostbase.ca entry box?

If you have multiple transactions over the course of the year, you can choose whether to use the exchange rate on the date of each transaction or use the average exchange rate. You should, however, try to be consistent with this choice over the year.

The currency conversion should be applied to each transaction. Applying the exchange rate to the final total capital gain or loss is not correct and could yield a vastly different answer.

Yes, those figures are correct for the average annual USD exchange rate for 2014.

Still a bit confused on that… if you use the average USD exchange rate for all transactions within the year, wouldn’t that would out to the same result? You mention it could have a ‘vastly different answer’?

For example method 1:

Sale 1: $100 USD at 1.10 exchange = $110

Sale 2: $200 USD at 1.10 exchange = $220

Sale 3: $300 USD at 1.10 exchange = $330

Summing them is $660

Versus method 2:

Sale 1 $100 USD + Sale 2 $200 USD + Sale 3 $300 USD = $600 USD

$600 USD at 1.10 exchange = $660

For the security transaction entry box, do we use the BankofCanada value, or the inverse value? (I’m thinking it’s the inverse?)

You seem to be calculating the proceeds of the disposition in your example, not the capital gains. The capital gain is found by subtracting the proceeds (and commission) from the ACB. Since the ACB is tracked in Canadian dollars the proceeds must also be converted into Canadian.

There is a special case where you might be able to get away with only converting the final capital gain result: where all transactions for a security take place in a single year (the share balances at the beginning and end of the year are both zero), you’re using an average annual exchange rate and the commission is in foreign currency. However, I wouldn’t recommend using a method that only works in very limited cases. Also, Schedule 3 requires you to report all figures in Canadian dollars so I don’t see much of an advantage to this method.

On AdjustedCostBase.ca you always need to enter the value of $1 Canadian in the foreign currency. Depending on the source of the exchange rate data, you may or may not have to convert this value. In the case of the Bank of Canada’s average annual rates, they’re listed as the value of one unit of foreign currency in Canadian dollars, so you do need to invert the value.

Pingback: Taxable Consequences of Norbert’s Gambit | Canadian Couch Potato

Could you please clarify the following:

1. Does the same adjusted cost base rules requiring each purchase and sale event to be reported in Canadian dollars also apply to “trading account” where multiple daily trades in the U.S stock markets are undertaken by an individual investor? Does the rule differ for 100% taxable trading a/c as against 50% inclusion capital investment a/c?

2. If the rules remain same for a trading a/c under “1” above, can an Annual average exchange rate data for all transactions be used instead of cumbersome actual exchange rate at the time of each purchase and sale transaction?

Nadeem,

The methods described here for calculating capital gains and ACB for transactions involving foreign securities are under the assumption that you’re trading on capital account, and not on income account. The factors the CRA uses to determine whether you’re trading on capital account or income account are somewhat subjective. Some of these factors include a high frequency of transactions and short ownership period, which may match up with your situation. Look for a post about this soon but in the mean time you can take a look at the following:

http://www.cra-arc.gc.ca/E/pub/tp/it479r/it479r-e.html

If trades are considered to be on capital account, then yes, you may use an average annual exchange rate.

It seems like a Canadian resident investing in US stocks will be at a loss if CAD$ depreciates over the US stocks portfolio holding period? that is kind of counter intuitive, or am I missing something?

If you hold US stocks and the Canadian dollar depreciates against the US dollar, then the value measured in Canadian dollars will increase (assume the stock price in US dollars doesn’t change).

Quite an interesting discussion. I wonder what tax treatment will be on a US$ margin Trading Account for a Canadian resident from an FX gain/loss tax perspective. For example, a canadian resident invests US$100K of her own capital in a US stock plus 200% margin provided by her broker. So her total initial exposure will be US$300K. Assuming that there is no change in the underlying stock’s price during the holding period, but the CAD$ declines by 20% during this holding period. If that trade is liquidated with no underlying stock price gain, she will get back only US$100K (US$300K-US$200K margin). Even if the investor immediately converts the proceeds into CAD$, she will receive only CAD$ 120K (US$100K x 1.20 CAD/USD rate). However, based on the above tax treatment, she may be required to pay tax on CAD$60K exchange gain (US$300K shares value x 1.20 CAD/USD rate). She will lose US$40K net of her own capital!! I know I am wrong somewhere as it cannot happen anywhere in the rational world!

Could you please clarify the correct tax treatment for US$ margin trading account under the above example? Thanks..

Rihana,

According to IT-95R (https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/it95r/archived-foreign-exchange-gains-losses.html): “determining the income tax status of foreign exchange gains or losses is the identification of the transactions from which they resulted, or, in the case of funds borrowed in a foreign currency, the use of the funds.”

So if you borrow US dollars for the purpose of buying stocks, and the transactions for the stocks are considered to be on capital account, then any gain or loss resulting from foreign exchange rate fluctuations on the borrowed funds would also be considered to be on capital account, and would offset or augment any gain or loss on the stocks.

In your example, assuming that the dollars were at parity at the time the funds were borrowed and the stock purchased, the gain on the stock would be CAD$60k ((US$300k x CAD$1.20/US$) – (US$300k x CAD$1.00/US$)). However, there would be an offsetting loss due to the borrowed funds. In this case, the USD$200k that was borrowed is would result in a capital loss of CAD$40k ((US$200k x CAD$1.20/US$) – (US$200k x CAD$1.00/US$)). The appreciation of the US dollar causes a loss on the borrowed funds. Therefore, the net capital gain would be only CAD$20k.

I’m not completely clear whether the borrowed funds would be treated independently in the case where you have other long positions in US dollars.

Thanks for a very informative reply to my query. Referring to the same query, will I be correct in deducing that the FX gain/loss will be zero if I use “Annual Average Exchange Rate” assuming that both legs of the trade were opened and closed within the same year (2014) as follows?

((US$300k x CAD$1.104466/US$) – (US$300k x CAD$1.104466/US$)) = 0

Is my above calculation is correct? If I am right, will the use of Annual Average Exchange Rate beneficial for the investors who don’t want any FX risk in their stock trades?

Thanks,

Rihana

Rihana,

The CRA permits you to choose either the average annual exchange rate or the daily exchange rates when multiple transactions have occurred, as long as you’re consistent with which method you use (although I’m not sure whether special rules apply for borrowed funds).

But when you have transactions involving actual currency conversion, as opposed to deemed purchases and dispositions, it may be advantageous over the long run to use the actual conversion rate that applied to your transactions (and the daily rates for deemed purchases and dispositions). This is because the currency conversion spread (the difference between what you pay to buy and sell currency) will slightly reduce capital gains.

I’m not sure I agree that using the annual average rate will reduce foreign exchange risk. Although it can change the calculated capital gain, it doesn’t hedge the currency risk of your investments. Also, using the average rate will not always be beneficial like in your example – it could just as easily increase calculated capital gains, depending on the fluctuation of the exchange rate.

I am bit confused about your comment that using the average rate will not always be beneficial and it could just as easily increase calculated capital gains, depending on the fluctuation of the exchange rate. Could you please elaborate it may be by an example. Thanks as always 🙂

In your example, the stocks gained in value as measured in Canadian dollars because the value of the US dollar rose. If you use the average annual rate then no gain is reported so it works out to your advantage compared to using the daily/actual rates. But if, on the other hand, the US dollar fell, you’d be better off using the daily/actual rates because you would be able to harvest a capital loss.

But I wouldn’t recommend picking the method based on this because you should be consistent with whatever method you choose, and it should end up averaging out to about the same over the long run.

Great blog. Thanks. Hope you can respond again. It’s hard to find an explanation on these foreign investment topics. If I understand …

– When buying US stocks it is necessary to calculate the ACB based on the $US exchange rate on the purchase date PLUS in that tax year claim any exchange rate gain or loss for any existing $US used in the purchase.

– When selling US stock the capital gain or loss is based on the proceeds at sale with the exchange rate of the sale. There is no related foreign exchange gain or loss due to the difference in the exchange rates between purchase and sale of the US stock.

– If I then spend the $US directly on personal expenses (no $CDN conversion) I still have to calculate a foreign exchange gain or loss for income taxes.

Are these points understood correctly?

I have seen the selling described as two pieces, capital and forex gain/loss.

I called CRA twice about this and got two answers. Both times I was referred to an expert. The first said pay no attention at all to the exchange rate gain/loss on the purchase. The second said to use my historical ACB for the $US exchange rate and not the exchange rate on the purchase date and also that I had to pay no forex gain/loss if I spend the $US on personal uses like a family trip. The latter would defer any forex gain/loss to selling the stock but I’d like to do what is correct.

What do you think of the CRA advice?

Also would you or anyone else know where to report the foreign exchange gain or loss in the tax forms? Is it somewhere on Schedule 3 such as section 5 line 153?

Sincere thanks for your help.

HI;

Would really appreciate input on my question. When I am inputting a US stock position in ACB transaction page, I am confused as to which ‘foreign currency exchange rate’ is supposed to go in that box. When I go to the Bank of Canada website and lookup the Monthly Average Exchange rate 10yr lookup, either the average or monthly average I see there are 2 columns:

1) 1 USD->CDN; 2) 1 CDN->US . Therefore, I am baffled as to which is supposed to go in the transaction page area. I’m gathering it is the 2nd one? As well, I am unsure of which U.S. dollar rate to choose: (noon), (close), (high), (low) from BoC page.

If I am recording and using daily rates from my broker ie. Disnat Direct (Desjardain), what is the proper conversion if they are listing it as “*US/Canada Exchange Rates (Mar. 28, 2015): 1.258”. ? Would this rate need to be converted to this format ‘CDN>US’ 1/1.258 = USD$0.7949 ?? before it goes in transaction page ‘foreign exchange box’??

Your help is much appreciated!

Greg,

It sounds like you’re understanding correctly. Except:

“There is no related foreign exchange gain or loss due to the difference in the exchange rates between purchase and sale of the US stock.”

The gain or loss will depend on the difference in exchange rates at the two points in time. As in the example from above, both of these exchange rates are factors in determine the capital gain, since the amount invested and the proceeds are both converted into Canadian dollars when calculating ACB.

Yes, I believe that spending foreign currency is considered a deemed disposition and can result in a gain or loss. From IT-95R:

“Examples of the time when the Department considers a transaction resulting in the application of subsection 39(2) to have taken place…at the time funds in a foreign currency are used to make a purchase or a payment”

I’m not sure what to make of the advice you received…both answers seem to contradict each other as well as information from the CRA’s web site and the Income Tax Act.

There actually doesn’t seem to be a place that’s completely appropriate for foreign currency cash gains on Schedule 3, but I would say section 3/line 132 is the best match. Section 5 may not be the best choice because foreign currency does not have a face value or maturity date.

Rob,

The exchange rate should be inputted into AdjustedCostBase.ca as the value of one Canadian dollar in foreign currency units. So at times like the present where the US dollar is more valuable than the Canadian dollar, the value you enter will be a value less than 1.

In your example you’ll want to go with the value in the “1 CAD->USD” column.

Depending on the data source and where you’re looking up the currency value, you might be given the value of one unit of foreign currency in Canadian dollars (e.g. 1 USD->CAD) or the value of one Canadian dollar in units of foreign currency (e.g. 1 CAD->USD). As you’ve guessed you can convert between the two formats by calculating the reciprocal (1/x), and it looks like 0.7949 is the appropriate value.

I believe the noon rate is the preferred rate to use. However, I’m not sure that the average monthly rate is the best choice for calculating capital transactions.

I use Average Annual Exchange Rate of 1.1044 consistently for all my purchases and dispositions during 2014. I have 2 questions as follows:

1. What exchange rate should be used in 2015 for all outstanding stocks holding carried forward from 2014. Should it remain at 1.1044 assuming that the original purchase year was 2014?

2. Which Annual Avg exchange rate should be used in 2015 for dispositions of stocks purchased in 2014. Should it be 2014 rate or 2015?

Michelle,

If you have outstanding stocks that you own, there’s no need to persistently apply any kind of exchange rate as the ACB will remain the same. ACB usually only changes when a purchase or sale occurs.

The exchange rate you use should be the prevailing rate at the time of each transaction. When multiple transactions occur then the exchange rate on each transaction date (or each transaction’s year if using the average annual rate – or the actual exchange rate when a currency conversion occurs) will apply.

Thanks very much for your reply! As a new user to this room, I am greatful I found this site, as it is a saviour to my frustration with ACB’s over the years and having to have tax person do most of it. But now it is becoming more clear and the calculator or transaction entry sheet is great!

Wondering if anyone else can comment on what they use from Bank of Canada’s website for exchange rate for US stocks? Is the “US dollar-noon” the one most of you use? If so, do you use the daily rate or yearly average rate? Based on trading a few times a month. Thanks very much!

Pingback: Ask Bender: How do I report my US-listed Vanguard ETFs on Form T1135? | Canadian Portfolio Manager

Hello:

If I would be able to get your feedback on this scenario below for a US position traded a few times over. On my trading summary from discount broker I have the following transactions in US $ of course: (commissions included in their calculations): 2014:

Mar. 19: BUY 1000 @ 3.47 = 3475

Mar. 29: SELL 1000 @ 3.78 = 3774.91 (proceeds)

Jun. 13: BUY 800 @ 6.60 = 5285

Jun. 13 SELL 685 @ 7.72 = 5283.08 (proceeds)

If I were to take total proceeds of $9057.99 /(US avg exch. 0.90518452) – Total ACB $8760 /(US avg exch. 0.90518452)

=$10006.79 – $ 9677.59

= $329.20 Capital Gain ( based on average of all trades).

Then, based on entering all transactions in the spreadsheet on this website (with US foreign exch. already calculated in figures) I get:

So, I come up with 2 figures for Capital Gain(loss) for 2 SELL transactions:

Mar. 28: $331.42 Cdn

Jun 13: $837.31 Cdn.

Therefore, my question is what is the reason for the big difference and can I just take the average of all proceeds – total ACB to get gain/loss? Or am I supposed to declare the 2 SELL trades separately eventhough all trades were in the same year?

Thanks very much, Rob

Rob,

That is not the correct way to calculate capital gains. Since you’re not selling all the shares in the second transaction you can’t simply subtract the total ACB from the proceeds to determine the capital gain (see http://www.adjustedcostbase.ca/blog/how-to-calculate-adjusted-cost-base-acb-and-capital-gains/).

Also, I would strongly advise against applying exchange rates to aggregate values. Although this may work out to the correct value in some specific cases, most of the time you’re required to apply the exchange rate individually to the costs and proceeds for each individual transaction.

Very interesting blogs thanks.

I have a foreign property asset in Australia rented out for income. I incur monthly AUD rental expenses and receive AUD rental income. I maintain an AUD bank account to receive and pay these transactions. My situation is complicated by the fact that the rental property has a mortgage on it AND that the bank account is what is known as a “Mortgage Offset account” which merely means that mortgage interest is calculated on the net balance of the loan and bank account balances rather than just the mortgage balance. The rental business is reported on income account but the property itself is treated on capital account (ie I do not report capital gains on fluctuations in value of the property as income).

Should I be tracking the ACB of the AUD bank account and mortgage account? Should this be done separately or jointly? Or is it not necessary because the income / expenses are on income account?

Thanks

Simon,

It sounds like your situation involves a lot of complex aspects, so I’d suggest consulting with a professional.

Hi there,

In my case, I’m deciding to use exchange rates based on the date of each transaction. Is the “date of each transaction” considered the purchase date or the settlement date?

Thanks,

Bunmi,

I can’t find any information that confirms the CRA’s stance on this, but it makes more sense to me to to use the exchange rate on the purchase/trade date as opposed to the settlement date. The share price for a transaction (with or without foreign currency involved) is of course based on the market price on the trade date, not the settlement date, so it seems logical to extend this to the foreign exchange rate. And in cases where Canadian dollars are actually converted when purchasing stocks, the actual exchange rate is based on the exchange value on the trade date.

I purchased shares at a 15% discount as part of an employee share purchase program for U.S. shares. Shares were purchased at various dates over the span of my employment, so I am using ACB to determine what the capital gain is as I sold a portion of these shares. when I calculate the adjusted cost base and enter each buy transaction, do I use the discounted purchase price or the FMV (fair market value) listed on my statements from the financial broker? I am not sure that my employer included the gain from the purchase of the shares (the 15% discount) as a taxable benefit by including it as employment income in the year I purchased shares- so I thought that perhaps if I used the purchase price in my ACB transactions, versus the FMV price (which was higher) that the capital gain will actually be higher and perhaps more favorable to CRA?

Or do I use the FMV for the ACB transactions and then claim the benefit of purchasing the shares at a 15% discount as taxable income and convert that gain in USD to Canadian dollars? Thankyou for your response in advance.

Jane,

The rules for employee stock options can get somewhat complicated as there are different rules depending on the circumstances. I’ll try to address this in a future blog post.

Generally, the ACB at the time the options are exercised is equal to the fair market value at the time of exercise. There should be a taxable employment benefit equal to the difference between the FMV and the price paid for the shares.

I don’t think it would be acceptable from the CRA’s standpoint to avoid reporting the taxable employment benefit in exchange for a reduced ACB. The employment benefit is immediately taxable whereas the increased capital gain resulting from a reduced ACB would be deferred into the future (when the shares are sold). Also, a capital gain is 50% taxable whereas a taxable employment benefit is fully taxable (although in certain cases a 50% deduction can be claimed for stock options).

Thanks for the rapid response, that makes sense and luckily in checking back to paycheques, my employer actually did report the taxable benefit of the discounted stock (purchase price versus book value) in the year the stock was purchased through the employee stock purchase plan. I didn’t realize this as it was included in Box 14 as employment income but they broke it out on the paycheques so I could ensure it was in fact declared. So now I am doing the ACB for the year I disposed of the shares to determine the capital gain which I will claim on schedule 3 of my return.

Many thanks

Hey, this is my second year of doing the T1135 and this year I understand it a bit better as my investment knowledge has grown a bit.

I am still very confused about what the ACB is that the CRA wants to know.

I am American and my parents put 1500 into a mutual fund in my birth year. So in order to report a ACB, do I need to calculate the ACB going all the way back nearly 30 years? Or, do I just need to report the ACB for 2014 transactions? For example, in 2014 in one of my mutual funds, I had two dividends that were reinvested into the fund. In another fund, I had some short term capital gains that were reinvested Is that all I report?

Also, I own a portion of a house in the US that belonged to my grandmother. The house is currently owned by a LLC that my dad and uncles established after they closed the estate. How do I report my portion of the ownership?

I am so, so, so, confused. I wish they would make this form easier for the average Joe like me. I’m just afraid of getting whacked because I’m so ignorant.

I had some stocks denominated in Euros which I received as incentive shares from my employer, and subsequently sold with the funds sent to my Canadian bank. The brokerage charged a 2.5% fee to for currency conversion from Euros to Canadian dollars. Can I include this cost as a reduction in the proceeds of disposition when I calculate my capital gain? Based on CRA T4037, it would seem so to me: “Outlays and expenses – are amounts that you incurred to sell a capital property. You can deduct outlays and expenses from your proceeds of disposition when calculating your capital gain or loss.”

Scott,

Yes, you can include the cost as a reduction in the proceeds. In most cases I don’t believe that a brokerage will break the amount down into conversion costs and gross proceeds, but rather only the net proceeds will be shown.

On APR 07 2014, I bought some shares listed on the TSX, paying for them with C$. I paid a commission on the purchase, also in C$. The shares are also listed on the NYSE. On DEC 15 2014, I had the shares journaled over to the NYSE. My understanding is that that transaction is irrelevant for ACB purposes and all that matters for those purposes is what I paid for the shares (including commission) in C$ on APR 07 2014.

Assuming that’s right, my broker sends me monthly statements. In statements after DEC 15 2014, the broker shows a book value for the shares in U$, calculated by reference to an exchange rate for DEC 15 2014.

Should I care that the broker’s book value is wrong? Will it ever give that incorrect information to the CRA?

Leslie,

As far as I know, journaling shares does not result in a deemed disposition. So there would be no immediate capital gain/loss or change in ACB.

The book values reported by brokerages are very often incorrect (see http://www.adjustedcostbase.ca/blog/can-you-rely-on-your-brokerage-for-calculating-adjusted-cost-base-and-capital-gains/) so I would hope that the CRA would not base any assessments on that information. As long as you have records of the transactions from your brokerage and have done the calculations correctly based on these records, you should be fine.

Many thanks for taking the trouble to reply.

Leslie

i feel lucky to have found this site, and I would appreciate if you could answer a few questions.

1)First, let’s say I transferred 100k from a td cnd trading account to a US trading account while the 1$cnd = 1(US). So 100k CND = 100,000 US Would it make a difference if 1$ cnd =1.03 (US), would I have to pay tax on 3,000 foreign gain when I make the transfer.

Let’s say I then buy 1000 shares of apples for 100$. when rates are 1$ cnd=.97(US). the acb in canadian dollarsfor apple would be $103,092.78 Does a purchase by itself trigger a currency gain for income tax purposes or is it only when the securities is sold

I understand if I sell 500 of the shares at 100$ while 1$cnd=.94 (US), that i would have a gain of (53,191.49- 51546.39=$1,645.10

So if I decide a few months later to transfer the 50k in cash from the sale of the 500 shares back to my canadian account when rates are 1$cnd =.90US which =55,555, Does this mean I I would have to pay tax on a currency gain of 5,555.

Now let’s say that while interest rates are 1$cnd=.1(US), I use an extra 100,000 margin from my US account to buy 1000 shares of facebook at 100$. (1$nd=.98

$US) for share purchase=102,040 Cnd.

Holdings would be

-100,000 (US) margin due (100,000 canadian)

1000 shares of Facebook at $100=$100,000 (US) or ($102,040 Cnd)

500 shares of Apple at $100=50,000 (US) or (51,546 Cnd)

So if I now sell 500 shares of apples at 200$ =100,000 plus currency

1$ Cnd=.66667(US) =$150,000 Cnd). In this scenario, I would be paying tax on capital gains of 98,454 which 50k came from capital gain and the remaining 48,454 came from currency gain.

If I take that 100k and again transfer it to my td cnd account again while 1$ cnd is worth .66667(US). Do I still have to pay tax on the 50k currency gain as it was already paid on the sale of the apple shares.

Holdings would be

-100,000 (US) margin due (100,000 canadian)

1000 shares of Facebook at $100=$100,000 (US) or ($102,040 Cnd)

Let’s say I take an extra 50k from my us margin while the rate is still 1$cnd=.6667US and transfer it to my canadian account. What would be the tax consequence in this case. Any tax consequence triggered in this instance.

holdings would be

-100,000 (US) margin (100,000 cnd)

-50,000 (US) margin (75,000 cnd)

1000 shares of Facebook at $100= $100,000 (US) or ($102,040 Cnd)

I then proceed to sell the 1,000 shares of Facebook at 150$ for $150,000 while interest rates was 1$cnd=.75 (US) =$200,000 cnd for a gain of ($200,000-$102,040=$97,960)

I then pay off the 150k(US) (175k Cnd) margin while rates are still 1$ cnd =.75$(US (so 150k=200kCnd)). Would that mean I would have to pay tax on another 25k currency gain. And the remaining 50k would be transfered to the td cnd account. Since that 50k is the result of profit, is there still another currency gain triggered when that amount is transferred into the canadian account even though I already paid tax on the currency gain during the sale and if so what would be the amount if the rates are again 1$ cnd-.75$(US) at time of transfer.

I know this is long, I am really trying to grasp this and from what I see on this site, you have been very helpful. To me, if I understand this correctly, it almost feel like I am paying taxes on currency gains twice, once when I sell the securities and once more when I transfer the money back into my canadian account

Thanks

Ronald,

“First, let’s say I transferred 100k from a td cnd trading account to a US trading account while the 1$cnd = 1(US). So 100k CND = 100,000 US Would it make a difference if 1$ cnd =1.03 (US), would I have to pay tax on 3,000 foreign gain when I make the transfer.”

There would be no immediate capital gain or loss from converting CAD into USD. This only happens when the US funds are reconverted or deemed to be sold.

“Let’s say I then buy 1000 shares of apples for 100$. when rates are 1$ cnd=.97(US). the acb in canadian dollarsfor apple would be $103,092.78 Does a purchase by itself trigger a currency gain for income tax purposes or is it only when the securities is sold”

Yes, this can trigger a gain or loss, as the US dollars are deemed to have been sold.

“So if I decide a few months later to transfer the 50k in cash from the sale of the 500 shares back to my canadian account when rates are 1$cnd =.90US which =55,555, Does this mean I I would have to pay tax on a currency gain of 5,555.”

That’s correct, assuming you held no other US$ currency from the time you sold the shares until the time you converted the cash. Any other holding of US$ would impact your ACB.

“If I take that 100k and again transfer it to my td cnd account again while 1$ cnd is worth .66667(US). Do I still have to pay tax on the 50k currency gain as it was already paid on the sale of the apple shares.”

When you sold the shares and received the proceeds in US$, and then immediately converted the US$ to C$, you may incur a gain or loss. depending on your US$ ACB. If, before selling the shares, you did not own any US$, then the gain or loss would be negligible or nil, assuming the exchange rate doesn’t move too much, since the ACB would be about the same as the price for which you sell the US$.

“Let’s say I take an extra 50k from my us margin while the rate is still 1$cnd=.6667US and transfer it to my canadian account. What would be the tax consequence in this case. Any tax consequence triggered in this instance.”

I believe this would be equivalent to shorting the US$ and would therefore be taxable on income account, not capital account.

Regarding borrowing on margin in US$ to purchase shares, please see the question by Rihana above.

The following page may also help clarify some of your questions:

http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-for-foreign-currency-cash/

For the sale of foreign real estate and determining the capital gains and the ACB, I need to base my exchange rate on sale date and purchase date. Do i use the contract date or the settlement date? Thanks.

Anthony,

I’m not certain about this, but I believe it would make sense to use the exchange rate on the settlement date, when the funds are actually received.

This is a very informative blog!

I have a question regarding US income investments that pay a monthly distribution, which includes a return of capital in each distribution. Upon disposition and in calculating the capital gain / loss, is the original ACB used (with the original exchange rate) or is the current ACB used (with the current exchange rate)? I have owned this investment for 5 years and each year the ACB has increased to account for the return of capital.

Thanks for you help!

Gordon,

Distributions that are classified as ROC in a foreign country are fully taxable to Canadians and thus foreign ROC should not reduce ACB (note that when ROC is applicable, it reduces ACB).

ACB with foreign currency transactions needs to be calculated as detailed above (tracked in Canadian dollars with the conversions done at the time of each transaction).

I have a quick question for you.

I have a margin account in which I (all on the same day, therefore same FX rate):

1) Convert C$10,000 into US$7,500 (implied FX of 1.3333)

2) Borrow US$500 from my margin account

3) Purchase for US$8,000 of shares (for the example, let’s assume this is 800 shares @ US$10)

When I deposit C$10,000 into my US$ account, the C$ ACB is C$10,000 and the US$ balance is US$7,500. When I borrow US$500, my ACB increases by US$500 * 1.333 (one can see the transaction as borrowing C$ and then depositing this into my US$ account). Then I purchase US$8,000 worth of stock, which reduces my ACB to 0. Is this the right way to think about this?

If I sell the 800 shares at a later date for US$10. How should I look at my ACB? If the FX rate is 1.5, does my Canadian ACB become C$12,000 (800 * US$10 * 1.5 C$ / US$)?

Jay,

I’ll assume that you’ve borrowed the US$500 from a Canadian dollar margin account.

In general you’ll need to calculate the ACB for both US dollars and for the shares. But since the US dollar transactions are all at the same exchange rate, there would be no gain or loss, assuming that you don’t own any other US dollars. If you do own other US dollars, then the gain or loss would depend on your ACB.

After purchasing the shares, your ACB would be USD$8,000 x 1.333 CAD$/USD$ = $10,664.

After selling the shares, the ACB is reduced to zero and you incur a capital gain of (USD$8,000 x 1.5 CAD$/USD$) – $10,664 = $1,336.

Thank you for the prompt response. You are correcting in assuming I am borrowing US$500 from a Canadian (non-registered) margin account (Canadian discount broker account).

The capital gain I am incurring here is on the shares and not on the foreign exchange, correct?

I think in general, there is a lot of confusion stemming from the fact that you need to track both shares’ ACB and foreign currency balance ACB.

Going back to my initial example, what would be my foreign exchange ACB at the end of those transactions? Would it be C$12,000 (US$8,000)?

Jay,

Yes that capital gain is on the shares. Assuming that you own no other US dollars and that the exchange rate is constant, there would be no capital gain or loss on the shares.

For further details on calculating ACB for foreign currency cash please see http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-for-foreign-currency-cash/ .

At any point where the share/unit balance is zero, the ACB must also zero.

I know you have covered some of this above, but I still do not get it.

I won’t try to use numbers but just try to get the idea first. My particular question is if there is a margin account that holds both USD and CAD denominated stocks and of course a separate cash balance for both USD and CAD. Assume the available margin credit is a composite of that available from both currencies. So when I buy US denominated stocks I do NO ACTUAL forex but just borrow the needed USD to purchase the USD stock. This results in a constant USD debit (higher or lower) in the margin account as I buy or sell more US stocks in the account. To date no actual forex has occured, just the purchase or sale of various US stocks in this account over the last several years. The account has always had a negative USD balance that has changed with these transactions.

How do I track both the ACB for the various different stock in this account and how do I track the USD ACB in this account. I presume it is one USD ACB for the entire account, not a separate USD ACB for each different stock? when are the ACB changes triggered – only with the sale of the USD denominated stocks? So if there are N different USD stocks I will have N+1 ACBs to keep track of? Are the borrowings of US dollars from the margin account akin to selling the USD short?

How many years must/can I go back to amend to fix this? which is it, must or can? In general is there a limit to how far I can amend in the past years? Is there a limit to how far back CRA can go back to reassess my returns for this sort of error? Can I just leave the past years alone and just start anew this year – now that I am starting to learn of the problems? What if it turns out I cheated myself say in the year 2003 or 2006 can I still amend those years?

Thanks for your help

One more question re the margin account. Say you start with no USD cash or stocks – all at a zero balance. You buy some USD stock for $100,000 USD which you pay for with credit from the margin available in your account. Say the stock goes down to $80,000 USD and you now sell it. Say the margin account charges me $1000 USD per month interest which it adds to the debit amount over 5 months. The $80,0000 USD sale proceeds reduce the margin debit to $25,000 USD. Some time later, after another $1000 USD of interest has been added to the outstanding debit, you pay back the debit amount of $26,000 USD to bring the debit to zero USD. How is this handled?

In reference to the above question, would your response be different if the borrowing was from the U.S Dollar Margin A/c instead of the CAD margin A/c? Will there be different Net Gain/ Loss? Thanks

Nad

Nad,

Please see the following comment above about this:

http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-foreign-currency-transactions/#comment-81348

Thanks for the link which is quite informative. But my confusion emanates from the fact that the fx rate moved from 1.33 to 1.50 in the above example. Would not that result in a loss on US $500 margin borrowing by 500*(1.33-1.50) = -$135 ? So the net cap gain of 1,336 – 135 = 1,201 ?

Thanks

Nad

Nad,

I’m referring to the comment dated March 18, 2015 at 12:07 pm (I think the comment you’re looking at is about borrowing from a CAD$ margin account).

Sorry for the confusion. My question is about your response to Jay on March 8, 2016 @ 7:24. So am I correct in my calculation ? Thanks

Nad

Nad,

In that case Jay is borrowing from a CAD$ margin account (even though the proceeds are converted into USD$ after borrowing). So there’s no offsetting gain or loss due to borrowing USD$.

While waiting for your response to my questions being moderated, I have tried to figure out how to use your ACB calculator for my questions on borroed margin for purchase of USD stocks. Please comment on my thoughts.

first I tried to enter -$1 instead of +$1 for the unit of USD borrowed but the calculator refused to accept that entry since it was negative.

Then I tried to enter the USD borrow as +$1 but as a sell transaction but this resulted in a zero ACB – it would not go negative for the borrow.

what seems to work if I understand this correctly is enter the usd borrow as a buy with +$1 and treat the “share balance” as the debit amount remaining margin balance owing in USD, BUT, treat a positive capital gain on a pay down of margin from a sale of a usd stock that goes to pay down the USD margin owing, as a capital LOSS, and vice versa.

Does this make sense to you?

Thus when I buy USD stocks on credit this will increase the ACB of the debt, increase the USD margin debt but not result in a gain or loss on the UDS debt. However when I sell some USD denominated stock with the proceeds paying down the USD balance owing on USD margin, the debt will reduce by the usd proceeds of the sale and the ACB will reduce by the CDN equivalent of the sale value on that day, and the capital gain will be the opposite sign of what the calculator shows for capital gain/loss and the remaining usd margin balance will be shown in the “share balance” column. Is this right?

Hank,

[Re: comment from March 8, 2016 at 1:13 pm]

For a discussion about US margin accounts please see this comment from above:

http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-foreign-currency-transactions/#comment-81348

Regarding tracking ACB for foreign currency cash, please see the following:

http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-for-foreign-currency-cash/

I’m not aware of the rules for going back and amending tax returns from many years ago. I’d suggest you consult with a professional about that.

Hank,

[Re: comment from March 10, 2016 at 5:12 pm]

The formulas for calculating adjusted cost base and capital gains do not work for negative balances, so you shouldn’t attempt to perform such a calculation. Borrowing or shorting is normally not considered to be on capital account, but my understanding of IT-95R is that in certain cases, the gain or loss from borrowing foreign currency to invest in capital assets can be added to the gain or loss from the underlying investment.

If you’re treating both the purchase of the shares and the gain or loss from borrowing foreign currency on capital account, then you can input the gain or loss from borrowing foreign currency by adding this cost to the commission when using AdjustedCostBase.ca.

I quote your response on 18-March 2015 to Rihana’s query as follows:

“So if you borrow US dollars for the purpose of buying stocks, and the transactions for the stocks are considered to be on capital account, then any gain or loss resulting from foreign exchange rate fluctuations on the borrowed funds would also be considered to be on capital account, and would offset or augment any gain or loss on the stocks.”

Could you please clarify where should this G/L due to FX rate fluctuation on borrowed funds be noted on the Tax returns? Should this be on Schedule-3 or somewhere else?

Many thanks,

Nad

Nad,

Yes, it should go on schedule 3. As to where specifically, I’m not entirely sure, but I suppose you could factor it into any one of the proceeds of disposition, the adjusted cost base, or the outlays and expenses columns.

So if Iliquidated all foreign holdings annually on the last day of the year and converted proceeds to Cdn $. Then in the new year convert back to foreign currency and rebuy positions could I avoid currency gains? I would just use the average annual exchange rate for all transactions. I would of course lose money on the conversion spread, commissions, and have capital gains to pay for but if the CDN $ has lost $30% I would have a lot less to lose potentially.

Thank you for this excellent discussion

Thank you for this great program to help me determine capital gains on a U.S. stock I purchased through an employee stock purchase plan. I am hoping you can answer my question. I am a Canadian who purchased the company’s U.S. shares in allotments each 3 months for the term of my employment. Each time I purchased shares they were purchased at a 15% discount from the fair market value at the time of purchase. The purchases were taken off of my pay and the U.S. purchase was converted to Canadian dollars for the deduction. The employer reported the total discount each tax year, as a taxable benefit and they converted the amount that was discounted in U.S. dollars to Canadian dollars on my T-4 slips. My question is when I use the ACB tool for foreign securities, would I state the lower discounted purchase price (in USD) or would I use the higher fair market value of the shares (in USD) at the time of purchase? I will be realizing a capital gain for sure as the shares have gone up a lot since my initial purchases but I want to ensure I use the right purchase price so that my ACB and capital gains are correct to report on my tax return.

Joel,

I’m not completely sure about the implications of that, but I would suggest avoiding that sort of scheme.

For one thing, the CRA has been contradictory about the acceptability of using annual average exchange rates: in certain parts of its web site it suggests that average annual rates can be used, but in other materials it indicates that it can’t be used (see http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-for-foreign-currency-cash/#comment-124899).

Also, currency fluctuations tend to cancel each other out in the long term, so there’s a good chance you would end up costing yourself a lot in exchange fees for nothing.

Jane,

The taxable benefit of 15% would be added to the adjusted cost base of the shares. For example if the FMV of the shares is CAD$10.00 and you acquire them for CAD$8.50, then you should have a taxable benefit of CAD$1.50 per share and the ACB becomes CAD$10.00 per share (assuming this is the initial purchase – otherwise total ACB increases by CAD10.00 x the number of shares acquired).

There are some rules that permit shares acquired through employee stock options to be pooled separately in certain cases but I’m not sure if that also applies for employee share purchase plans.

Hello, I am confused by your response to my question regarding whether to use the FMV purchase price for U.S. shares or a discounted price that I actually purchased the shares for within an employee stock option purchase plan. Your response would indicate that I should use the FMV price but then you cite an example in Canadian dollars (FMV of $10.00 CAD and acquiring them for a 15% discount at $8.50 CAD and that the ACB on an initial purchase would be the FMV or $10.00 CAD per share). I thought that when you purchase or sell foreign securities- you state the value of the transaction (and any commission associated to the transaction) in that foreign currency (in my case in USD), check off the box stating the price is in foreign currency and then you can use the Bank of Canada currency converter for the date of each purchase or sale to ensure the exchange rate is used for the day you acquire or dispose of the foreign shares. If you buy and sell U.S. shares you would use CAD$1= USD as the Canada Revenue Agency requires capital gains or losses and adjusted cost base for securities to be reported in Canadian dollars? Perhaps you just used an example in Canadian dollars for simplicity sake? Can you please confirm. Thank you very much

Jane,

The example above assumes all values have already been converted into CAD$ for simplicity. If, for example, the exchange rate was CAD$1 = USD$0.80, then for this example the FMV would be USD$8.00/share, the cost paid by you to acquire the shares would be USD$6.80/share and the benefit would be USD$1.20/share, before any of these values are converted into Canadian dollars.

Hello,

I have one quick question about the exchange rate.

Lets say I used US dollars purchased 100 shares of Apple @98. The ACB would be 9800 us dollars.

Then I sold the 100 shares directly into my Canadian account which means in Canadian dollars. As you know, the exchange rate the bank has is lower than it supposed to be, because the bank charges for that.

If Im using the exchange rate the bank offers, I could save the cost of converting US cash to CDN cash because it would be part of my capital gain or loss.

To make my statement clear, I will give u a more specific example.

May 1st Purchased 100 shares @98 with US cash. Exchange rate is 1.3222.

May 1st Sold 100 shares @100 by converting to CDN cash. Exchange rate of bank is 1.3111.

Therefore, what i”ve gained would be less if I am using the exchange rate of the bank.

Please clarify it! Thanks a lot!

Kun,

You can use the actual exchange rate used for the conversion when an actual conversion occurs, and you’re correct that it’s usually in your favour to do so due to the spread.

What happens if we modify the Rihana case above slightly. When the US shares are sold say they have gone down by 50% so that only $150,000 USD is recovered with a remaining $50,000 USD of margin debt that continues to be owed and could remain on the books for months or years until covered. Would you treat the currency loss on the remaining unpaid $50,000 at the time the stock is closed out or ignore it until it is eventually paid back and treat the currency loss on it at that time and would it still be on capital account since it began for the purchase of the stock? Thanks.

Hank,

I’m not too sure about that case. I would lean towards it not being acceptable to report that on capital account and along with the shares, since the borrowing transaction is not perfectly matched with the ownership of the shares.

I am not sure if the deemed disposition rules apply to everything. The CRA web site indicates that if you use the foreign funds to purchase a negotiable assets (such as stocks or bond), you have to calculate the FX gain/loss. However, if you use the funds for a vacation expense, I do not think this will trigger a FX gain/loss calculation.

JF,

If you have a source for that information, I’d appreciate if you could share it.

From IT-95R:

“the Department considers a transaction resulting in the application of subsection 39(2) to have taken place…at the time funds in a foreign currency are used to make a purchase or a payment”

where 39(2) refers to a section of the Income Tax Act dealing with foreign exchange capital gains and losses.

Hello I want to ensure I am using the right exchange rate for a transaction of selling U.S. shares for U.S. currency and then converting it into CAD dollars for reporting to CRA. I sold 25 U.S. shares for a total of $5691.25 in USD. I used this figure as a total amount in the ACB transaction and checked off the “Price in Foreign Currency. I used the Bank of Canada 10 year currency converter and in the transaction for exchange rate CDN$1= I used the rate of 0.7996. Can you confirm that I used the correct exchange rate in my transaction.

Thank you very much

Sorry my previous post should have included the date of the sale of my 25 U.S. shares. The date was Feb 20, 2015 (last year) and the exchange rate I used to convert the sale in USD ($5691.25) to CDN $1= was 0.7996 as posted by the Bank of Canada 10 year currency converter. Can you confirm if I used the correct exchange rate. They also list an inverted rate of (1.2506) but I assume that I don’t use the inverted rate?

Thank you

Jane,

That sounds correct. The rate you want to use is the value of one Canadian dollar in unit of foreign currency. Since the Canadian dollar was lower than the US dollar last year, the exchange rate you enter in AdjustedCostBase.ca should be less than 1.

Thankyou very much!

One other question please. I bought U.S. stocks for a discount as am employee. I had five purchases and claimed the discount (15% on each purchase) as a taxable benefit. When I sold the stock and used the share price I sold the stock for, I had a capital gain as the shares had substantially increased in price from the time they were purchased.

My question is regarding the BUY transactions. Should I have used the lower discounted price that I purchased the shares for or the actual market price that I would’ve had to buy the shares for, without the discount?

I ask because the discount was treated as a taxable benefit by my employer and I have paid tax for this. If I use the discounted price for my buy transactions instead of the actual price (which is 15% higher) my capital gain will be 15% greater.

For simplicity, if I bought 100 shares that were selling at $1.00 each at a 15% discount for$ 0.85 (100 X $1.00- 15% = $85.00) and used that discounted price as my BUY price and then SOLD those 100 shares for 2.00 each, the capital gain would be (100 X $2.00) – (100 x 0.85)= $115.00.

But if I used the actual non- discounted share price of $1.00 as my BUY price (100 shares X 1.00=$100.00) and sold the 100 shares at $2.00 each the capital gain would be less at $100.00

Can you advise on whether I use the actual market price or the discounted price I bought the shares for in my BUY transactions with a consideration that the CRA got their taxes from me as the discount was claimed as a taxable benefit.

Thank you very much, hope my question and example are clear

Jane,

As you claimed the discount as a taxable benefit already, I believe you should use the full fair market value of the shares to determine the ACB. Otherwise, you would be paying taxes on the discounted portion twice.

Thanks very much…that’s what I thought too!

How would you deal with foreign securities purchased from cash from a US refinance loan? Would you figure basis based on exchange rates as normal and claim the opposing gain/loss separately (net gain/loss=0)? Or can you use the same exchange rate for both proceeds and basis to eliminate any gain/loss from exchange rates? So far I’ve been repaying the loan from the proceeds of the loan (borrow from peter to pay peter). Do i have to report any currency gains/losses from repaying principal and interest? No actually currencies conversions occurred.

Thank you

Regarding the earlier discussion about whether to use the exchange rate on the settlement date or the trade date when calculating the ACB of equities purchased in a foreign currency the CRA released a Q&A from the fall of 2015 in which they indicate that the exchange rate on the settlement date should be used. I have not read any other official statement from the CRA other than some websites stating the same.

http://www.taxtips.ca/documents/2015-0588981C6-foreign-currency-exchange-date.pdf

http://www.taxtips.ca/personaltax/investing/taxtreatment/shares.htm

http://www.theglobeandmail.com/globe-investor/investor-education/calculating-gains-and-losses-on-us-stocks-part-2/article28747713/

FV,

It seems like it would be reasonable to use the exchange rate on the settlement date, assuming that if a cash conversion had taken place (selling a US stock in a CAD account) then the currency conversion might take place on the settlement date.

Although others have cited that roundtable document, I choose not to take it too seriously. It’s a transcription of a verbal statement made by a single CRA employee at a conference and isn’t even published on the CRA’s web site nor is it officially available in English. Much of the content either isn’t backed up by documentation on the CRA’s web site, or even contradicts the CRA’s web site.

But in any case, the exchange rate on a trade date is likely to be very similar to that on the corresponding settlement date.

So I sold a stock at the end of the year last year and now am trying to figure out the capital gains exact number. I had purchased shares of a company I was working for through an ESPP in 2014. The company sold out and the amount of shares I had almost doubled, this is where I’m unsure if I need to modify my calcualtions and the exchange rates? I had 103 shares and then received 192 shares in the sale of the company. This is a foreign investment so I do have to work out the adjuted cost basis in Canadian dollars.

What does one do with the US transaction taxes? Do include this along with the commissions as a cost to share sales?

Hi,

You (“The Author”) mentioned multiple times that you recommend to be “consistent” when choosing whether to use the Annual Average Exchange Rate or the Daily one.

How consistent? Let’s say that I have securities A and B, which I hold and occasionally buy/sell since a few years ago (and that I’ll continue to hold for long time). I also hold USD$ (that generates more than $200 in capital gain/year).

When you say that you recommend to be “consistent”, do you mean?

1. That you can choose whatever method suits you better for each security/year combination. In other words, for example, A in 2016 can use AVG, B can use DAILY. In 2017 I can use DAILY for A and AVG for B (so I reversed it).

2. Choose a method for each security and stick to it forever. A can be AVG, B can be daily (on 2016, 2017, 2018, etc).

3. Choose a method per YEAR and use it for all the securities/transactions (including foreign currency cash): 2016 can be AVG, 2017 can be DAILY, 2018 can be AVG.

4. Choose a method and stick to it for the rest of your life, ie: you either use AVG or DAILY, but when you start to use it do not change it (or think very seriously before changing it, and in any case use the same method for a given year, all transactions).

Also: I guess regardless the method that is used, the End of Year ACB balance of each security is carried forward to the next year (meaning: if I have calculated my ACB using AVG until 2015-12-31, but on 2016-01-01 I switch to DAILY I just take the balances from the 2015-12-31… I do NOT go back to the history and recalculate the ACB all over with DAILY).

Thank you.

I have some $$ in a Canadian taxable account that is in USD. I buy and sell US stocks in that account. To calculate gains/losses on those trades in that account, I understand how to convert the sale and ACB amounts to CAD using the USD/CAD exchange rates. I choose to use the individual exchange rates on the purchase date and on the sale dates. No problem so far.

HOWEVER, since the conversion of the buy and sell amounts to CAD is, in fact, a ‘simulation’ (where no actual foreign exchange takes place), I still want to use the ‘bank spread’ exchange rates, and not the nominal daily posted exchange rate. So in other words, I want to use the bank’s ‘buy USD’ exchange rate on the stock’s purchase date, and the bank’s ‘sell USD’ exchange rate on the stock’s sell date.

The bank’s buy and sell rates are typically around 2% from the nominal rate, so there is a total 4% turnaround cost on each stock round trip (purchase and sale). That 4% can really add up over time (as a cost), so why don’t we use the buy/sell USD rates instead of the nominal posted rate?

Jose,

Although I’m not aware of any specific rules that the CRA uses, the more consistent you are the better. So I would recommend you try to stick with #4 as much as possible.

Also note that some CRA documentation has advised against using the average annual rate for capital transactions, although this is contradicted elsewhere.

We have also introduced a new feature for AdjustedCostBase.ca Premium users to lookup daily exchange rates while inputting transactions, which should simplify using daily rates.

Paul,

I would not suggest that you use an exchange rate other than one posted by the Bank of Canada, unless funds were actually exchanged at that rate and you have the supporting documentation.

It sounds like in your case you would like to deduct the spread which you haven’t actually paid in order to reduce your gains. I don’t think that this would be well received by the CRA.

Thanks for your reply and thoughts. Yes, I am saying why can’t I use (deduct) the ‘spread’ to the posted rate.

True, I didn’t actually pay that spread, but I also did not actually make the trade in Canadian dollars! So the whole calculation/valuation is a shell game.

CRA requires us to ‘mimic’ the trade (in $CAD) by doing the calculation/conversion to $CAD, but we would never actually be able to execute that trade at the posted rates. A ‘true’ mimic would be to use the real costs (to buy USD upon the purchase, and to buy CAD on the sale), which of course would be at the ‘spread’ values.

This is exactly what happens if we buy US stocks from a $CAD account – the ‘exchange’ occurs at the spread values, not the posted rate. Obviously CRA has no trouble with that. I don’t understand why the exchange calculation (i.e. determination of value in $CAD) would not be the same – it is more realistic than using the (unattainable) posted rate.

Paul,

I would say the rules concerning capital gains for foreign currency stocks are in line with general rules about capital gains. The portion of capital gains arising from a foreign currency gain from selling shares isn’t really artificial as it represents an actual increase in value in Canadian dollars.

You could maybe argue at most that capital gains and losses on foreign currency should not be realized until the eventual disposition of the foreign currency (i.e., conversion into CAD or spending), however, that would only have the effect of deferring capital gains rather than reducing them.

Also note that exchange rates tend to even out in the long run (in contrast with the exponential rise in stock prices). So foreign currency fluctuations, over the long run, will help you (by reducing capital gains or increasing capital losses) about as often as they hurt you.

If you were permitted to factor in foreign currency spreads when no conversion to CAD has taken place, taxpayers could abuse this by repeatedly buying and selling foreign shares. Assuming you did this many times in a short period of time such that the share price and exchange rate remained constant, and trading commissions were negligible, you could effectively inflate the ACB of the shares as much as you please, without investing/expending any additional cash. Then you could sell the shares and claim a large capital loss even though you wound up even.

Author: thanks. BTW: I have used the Look Up feature (I have the Premium subscription). It works great.

However: I did import my transactions. One suggestion I’d like to make: the 100 transactions per Import is way too low. I suggest you increase it to ~300-500 (maybe a user setting, defaulted to 100 but with the option to increase it, should the user really want to do it).

The reason I have so many transactions is not because I am an active trader: it is because I track ACB of my USD$ and I do travel and spend money directly in USD$ (makes little or no sense to convert to take USD -> CAD -> USD -> spend).

Thanks you so much.

Jose,

Thanks for your feedback. We will look into implementing an increase in the transaction limit soon.

Re: FOREX, margin accounts, comment-80657 (Rihana / Mar. 16, 2015):

If a USD stock is bought with a combination of cash and margin, then sold later, how should the forex-adjusted cost of margin be reported?

Using the example from 2 years ago: $100K USD cash + $200K USD margin is used to purchase $300K USD in stock. After a 20% gain in the value of USD, the shares are disposed at their original purchase price, generating sales proceeds of $300K USD (or $360K CAD). However, repaying the margin would cost $200K USD ($240K USD). How should the $240K CAD cost be reported?

It doesn’t make sense to adjust the ACB of the specific transaction itself in part 3 of Schedule 3. It also doesn’t make sense to create a “cash/forex” entry in part 5, because there is no “issuer.”

Would the $240K CAD cost of repaying the margin be reported in column 4 of part 3 (“Outlays and expenses (from dispositions)”)?

I believe I found an answer to my question.

Gains on cash due to forex must be reported in part 5 of Schedule 3: “Bonds, debentures, promissory notes, and other similar properties.”

This is stated in T4037: Capital Gains:

Chapter 2 – Completing Schedule 3 -> Bonds, debentures, promissory notes, and other similar properties:

“Use this section to report capital gains or capital losses from the disposition of bonds, debentures, Treasury bills, promissory notes, and other properties. Other properties include bad debts, foreign currencies, and options, as well as discounts, premiums, and bonuses on debt obligations. Report these dispositions on lines 151 and 153 of Schedule 3.”

(Solution courtesy of a poster on the ufile.ca forums)

SRS,

I believe that section 5 of Schedule 3 is designated for debt instruments for which you are the creditor, not the debtor.

As mentioned above:

According to IT-95R (http://www.cra-arc.gc.ca/E/pub/tp/it95r/it95r-e.html): “determining the income tax status of foreign exchange gains or losses is the identification of the transactions from which they resulted, or, in the case of funds borrowed in a foreign currency, the use of the funds.”

So if you borrow US dollars for the purpose of buying stocks, and the transactions for the stocks are considered to be on capital account, then any gain or loss resulting from foreign exchange rate fluctuations on the borrowed funds would also be considered to be on capital account, and would offset or augment any gain or loss on the stocks.

The question remains how you would report such a gain on Schedule 3, not whether there is a capital gain to report.

In the example I gave, we both acknowledge that a $20K capital gain exists, and that it needs to be reported to the CRA. When selling the shares, the proceeds of sale are $300K USD, which is valued at $360K CAD. Are you suggesting that, at this point, the ACB should be reported as $340K CAD, resulting in a $20K capital gain?

I cannot believe that is correct. It is a retroactive adjusting of ACB based on the exchange rate when the investment is disposed, and the margin repaid. Furthermore, it would violate the premise behind the reporting requirement threshold for the T1135 (foreign income verification). If you bought, say, $75K USD worth of stock with a combination of cash and margin, and it is valued at more than $100K CAD at some point during the year, you would need to file a T1135. The reporting threshold is based on the ACB of the assets, which was determined when the asset was purchased. It shouldn’t be revised at a time in the future when the loan is to be repaid.

We are right back to square one: how do we report the underlying capital gain in a situation involving foreign currency and margin debt? At this point, the part 3 + part 5 method I described is cleaner, and more explicit, but I don’t actually know how the CRA would want the numbers reported.

SRS,

Capital gains need to be reported in Canadian dollars, and in general you can’t calculate the gain first in US dollars and then multiple the answer by the exchange rate. When calculating the gain each monetary value (share prices and commissions) needs to be converted into Canadian dollars at the time of each transaction.

In your example, the gain will depend on the exchange rates at the times of purchase and sale, not just the percentage gain of 20%. If the exchange rate was CAD$1.00 = USD$1 at the time of the purchase and was CAD$1.20 = USD$1 at the time of the sale of the shares and repayment of the margin debt, then the capital gain for the shares would happen to be CAD$20,000. On the other hand, if the exchange rate was CAD$1.10 = USD$1 at the time of the purchase and CAD$1.32 = USD$1 at the time of the sale then the capital gain for the shares would be CAD$22,000.

Let’s assume that the exchange rate was CAD$1.10 = USD$1 at the time of the purchase and CAD$1.32 = USD$1 at the time of the sale. I would list the proceeds of disposition as USD$300,000 x CAD$1.32/USD$1 = CAD$396,000. Assuming no margin, the ACB would be USD$300,000 x CAD$1.10/USD$1 = CAD$330,000. However, with USD$200,000 on margin in isolation, the short position in USD$ would result in a loss of ((USD$200,000 x CAD$1.32/USD$1) – (USD$200,000 x CAD$1.10/USD$1)) = CAD$44,000. I would then add this loss to the ACB of the shares.

So on Schedule 3 I would list the proceeds of disposition as CAD$396,000 and the ACB as CAD$374,000 (CAD$330,000 + CAD$44,000), resulting in a capital gain of CAD$22,000.

Note that the CRA isn’t exactly abundantly clear on how this situation should be handled, let along how it should be communicated on Schedule 3. This is just my best suggestion.

Note also that there would likely be a gain or loss due to the disposition of USD$ currency at the time of the purchase of the shares for the non-margin USD$100,000 portion, and an acquisition of USD$100,000 at the time of the sale.

I follow all your examples, and I am familiar with accounting for all of these dispositions (and subsequent capital gains) in terms of personal accounting purposes. My question isn’t how to calculate the capital gain, but how to explain (report) the effect of repaying foreign-currency margin debt.

Your method – adjusting the ACB based on the exchange rate at the time of the sale of the stock comes across like a type of backdating to me. It’s is equivalent to saying, “it’s impossible to determine the cost base of this asset until the asset is disposed” (due to fluctuations in exchange rates). I prefer an interpretation that ACB is fixed and determinate, regardless of what happens to exchange rates over time.

In all the examples we’ve presented, we have no disagreement on the calculation of bottom line, taxable capital gains. The CRA is going to gets its money. But I am still uncertain on how to report the relevant numbers on Schedule 3.

I will try to contact the CRA and see if they can give me a definitive response. At this point, I feel as though any large capital gain involving foreign currency and margin might lead to a “request for information” from the CRA, no matter how you reported your numbers.

I have an inquiry related to the CDS Tax Breakdown Service and foreign income. My securities have some international exposure held in Canadian ETFs, therefore I do not need to worry about converting from USD or other currencies to CAD. I am interested in determining what if anything needs to be done with the foreign business, foreign non-business, and foreign income tax paid for foreign business and non-business, that is reported as part of the distributions according to the CDS Tax Breakdown Service. Do these values have significance for the ACB and / or other tax reporting purposes?

Thanks,

A.S.

AS,

Foreign income should not generally affect ACB, unless it’s reinvested. Also, if you receive a distribution of any kind as cash in US dollars (or another foreign currency), this will become part of your pool or US dollars and its ACB will change.

Regarding your last comment to AS on July 10, 2017…

Great post by the way!

If you have a dividend reinvestment from a foreign security, would that create a foreign exchange gain/loss on the foreign cash (assuming cash is on capital account)?

In short, the tax consequences are the same whether it is a dividend reinvestment, or a dividend is paid, and then the funds are used purchase the same amount of stock that was reinvested?

If this is correct, do you have anything from CRA that confirms this?

Just to clarify – when buying, you would add the conversion from CAD to USD

Such as 100 shares at 20 USD each… / .80 for example

But when selling… it would be 100 shares at (say 22 each) * 1.10 for USD to CAN

I was looking over my sheet and realized I had used the “can to usd” conversion on both buy and sell but that’s not right.

Using data of today’s exchange: http://www.bankofcanada.ca/rates/exchange/daily-exchange-rates-lookup/?series%5B%5D=FXUSDCAD&lookupPage=lookup_daily_exchange_rates_2017.php&startRange=2007-10-16&rangeType=range&rangeValue=&dFrom=2017-10-16&dTo=&submit_button=Submit

Adrian,

You need to convert all US dollar amounts into Canadian dollar amounts. This means multiplying by the USD->CAD for both the purchase price in USD and the proceeds of disposition in USD in order to calculate these values in CAD.

Sorry for the late response – Thanks for the clarification.

Would the date used for the exchange rate be the date of transaction or the settlement date?

I trade with a Canadian broker but within a $US trading account. I am trying to figure out how to correctly input my buy & sell transactions into the new transaction field so that it is being calculated correctly into $CDN for the buy & sell transaction. It appears to me the way it is set up as a default on your transaction input screen that I am trading within a $CDN trading account and converting with each transaction. Please direct me in how to input my transactions correctly using your exchange rate feature. Thank you

David,

ACB and capital gains must always be calculated in Canadian dollars. Specifically, any price, proceeds of disposition and commission amounts must be converted into Canadian dollars.

On AdjustedCostBase.ca you can either:

a) Convert any foreign amounts yourself to Canadian dollars or use converted amounts reported by your brokerage and input these converted amounts when adding a transaction.

or

b) Keep the amounts in foreign currency and specify an appropriate exchange rate. AdjustedCostBase.ca Premium allows you to retrieve the exchange rate for the specified currency and date reported by the Bank of Canada.

Thank you for the reply. I have a premium account. So if I am trading within a US trading account, must I convert the buy into CDN & the sell into CDN. my understanding is it would be the sell/disposition that would be used to calculate any gains only. If I am correct how would I do this with my premium account? If I am not correct in my assumption, what is the correct input method since all my trading occurs in US$. Thank you again in advance

David,

The values (prices, proceeds of disposition and commissions) must be converted into Canadian dollars when calculating ACB. This is the case for both purchases and sales. If you have a specific example that you’re wondering about, please let me know.