AdjustedCostBase.ca now offers a streamlined method for importing phantom distribution and return of capital transactions for many exchange traded funds (ETF’s), publicly traded mutual funds, income trusts and real estate investment trusts (REITs). Learn more about this feature.

A phantom distribution (or reinvested capital gain distribution or notional distribution) occurs when an exchange-traded fund (ETF) or mutual fund makes a taxable distribution, but it’s reinvested back into the fund as opposed to being paid out in cash.

In the case of ETFs, an investor does not usually receive additional shares as a result of a reinvested distribution (hence the name, “phantom distribution”). This is because ETF providers (a) do not maintain client records, and (b) cannot issue fractional shares.

Phantom distributions usually occur when an ETF or fund incurs a capital gain, and the capital gain is reinvested instead of being paid out in cash. The capital gain will be immediately taxable and should appear on your T3 or T5 slip that you receive from your brokerage. So the capital gain will be accounted for when you compile your tax slips.

However, investors need to take additional steps to ensure that their adjusted cost base (ACB) is correctly calculated when phantom distributions occur. A phantom distributions, similar to a DRIP, results in an increase in ACB equal to the amount of the reinvested distribution. It’s in your best interest to account for phantom distributions. If you fail to do so, you’ll end up paying more capital gains tax than necessary when your shares or units are eventually sold.

The ACB resulting from a phantom distribution can be calculated as follows:

New ACB = (Previous ACB) + (Reinvested Distribution)

A phantom distribution is not usually specified on T3 or T5 tax slips, nor is it indicated on statements from your brokerage. As a result, the onus is often on the investor to determine whether a phantom distribution has occurred.

How do you determine whether a phantom distribution has occurred? One way is to consult the web site of your ETF or fund provider. For example, iShares issued a press release listing the reinvested distribution amount per unit for each of its funds for 2013. More than two dozen of iShares’ funds had a reinvested or phantom distribution in 2013, and some of the amounts were significant.

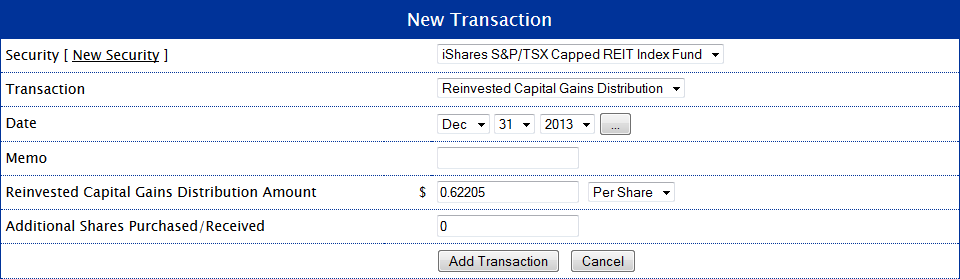

For example, we see from this press release that “iShares S&P/TSX Capped REIT Index Fund” (XRE) incurred a reinvested distribution of $0.62205 per unit in 2013, with a record date of December 31, 2013. This amount is reinvested into the fund, but investors did not receive any additional units.

![]()

AdjustedCostBase.ca is a web application that can be used to assist investors in calculating ACB including when phantom distributions occur. A phantom distribution can be specified by adding a “Reinvested Capital Gains Distribution” transaction. For the case of XRE in 2013, this would be done as follows:

Note that for this case you should enter “0” for the “Additional Shares Purchased/Received” because this is a phantom distribution where no additional shares are received.

In this case, the reinvested distribution has a corresponding capital gain associated with it. When using the “Reinvested Capital Gains Distribution” transaction type, the capital gain will be displayed automatically:

If a reinvested distribution were to occur without a corresponding capital gain, then you could use a “Buy” transaction instead, again setting the “Shares” amount to zero.

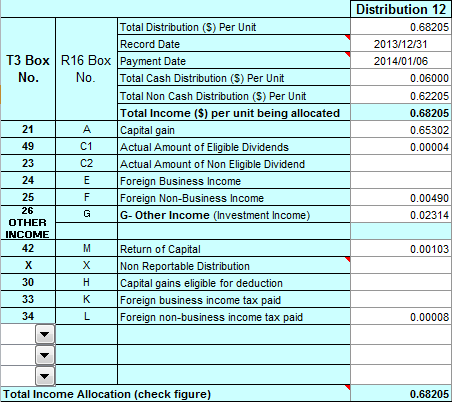

Another way to check if a fund you own incurred a phantom distribution is to consult the CDSInnovations.ca web site. Steps on how to find this information can be found here. Here is a snapshop of the year’s final distribution that includes the $0.62205 per unit phantom distribution:

The “Total Non Cash Distribution ($) Per Unit” row indicates that a phantom distribution of $0.62205 per unit has occurred. With this information, you can then add the “Reinvested Capital Gains Distribution” transaction on AdjustedCostBase.ca as shown above.

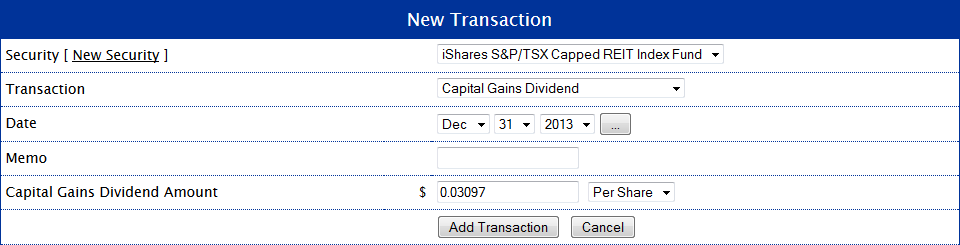

Note that there is a capital gain in this column equal to $0.65302 per unit. Since this capital gain is greater than the phantom distribution, there’s a residual capital gains distribution equal to ($0.65302 — $0.62205 = $0.03097) per unit. This would be entered into AdjustedCostBase.ca as a “Capital Gains Dividend” transaction as follows:

In some cases, the reinvested distribution, or a portion of it, is not in the form of a capital gain (for example, interest income). In these cases, you can enter the distribution using AdjustedCostBase.ca as a “Buy” transaction (and setting the number of shares to zero if no additional shares are received). A special case occurs when a reinvested distribution is in the form of return of capital. The reinvested distribution and the return of capital effectively cancel each other out: the ACB gets decreased by the return of capital amount, and then increased by the reinvested distribution amount. On AdjustedCostBase.ca, this can be entered as 2 separate transactions: a “Return of Capital” transaction and a “Buy” transactions.

Very useful post. I’ve noticed in the past that not all reinvested (or “phantom”) distributions are capital gains. BMO in particular seems to like doing this with their ETFs. I’ve seen reinvested interest (ZRR) and even reinvested return of capital (!) with ZCN.

Thanks, Tyler. I’ve added a note above to address these cases.

When a reinvested distribution is in the form of return of capital, it’s a particularly interesting case. When investors are completely ignorant about the effects on ACB of both return of capital and reinvested distributions, two wrongs will make a right, since they cancel each other out.

However, in the case where an investor notices the return of capital amount on their T3 slip and decreases ACB accordingly, but fails to increase ACB because the reinvested distribution isn’t listed on the T3, they’ll end up overpaying capital gains taxes when the shares are sold.

In discussion with CRA about interest paid to purchase mutual funds, the interest may or may not be eligible to claim as carrying costs, based on the premise that the mutual fund typically generates capital gains, not income. They said in that case, the borrowing cost could instead be included in the ACB.

How would that be done in the adjustedcostbase interface? I’m thinking maybe a ‘buy’ transaction with an amount but zero shares?

I’m not aware of any rule that allows you to add carrying costs to ACB for investments that generate capital gains (in fact page 188 of http://www.johnmott.com/files/pdf/chapter_15.pdf specifically advises against this). I would suggest speaking to a professional about this.

But in general, a “Buy” transaction for zero shares is a good way to increase total ACB by an arbitrary amount.

I may have been mis-remembering an article I’d seen where one of the newer tax software applications did something like this, although perhaps not this exactly. Then when the CRA agent suggested it, that helped me convince myself it was real. I’ll see if I can find a better reference 🙂

After going back through everything, it seems it was only the CRA agent who said to do this.

I think the article I’d seen was actually talking about adding superficial loss to the ACB, not adding carrying charges to the ACB.

A very helpful post. Thanks. Just to clarify, if on CDS Innovations, there is just a capital gain listed (with no non cash distribution), that amount should be recorded as a capital dividend?

Grant,

I’m going to assume you mean Capital Gains Dividend/Distribution as “Capital Dividend” has a another special meaning.

Yes, this should be recorded as a capital gains dividend. Assuming that there is no non-cash distribution, the amount should appear on CDS Innovations as a cash distribution.

Thanks, yes, I meant Capital Gains Dividend. In the instance I was looking at CDS Innovations (Dec 31, 2013 ishares MSCI emerging market IMI ETF), there is a capital gain of 0.00017 with no none cash distribution. There is a cash distribution of 0.17717, which I had assumed was all dividend, but I guess includes the capital gains dividend?

Grant,

In that case, yes, you would record a capital gains dividend of $0.00017 per share. Note that there is also return of capital in the amount of $0.01665 per share. Aside from that, nothing else will affect ACB assuming the cash distribution is not reinvested.

Yes, I noticed that adding the Capital Gains Dividend did not change the ACB. So why bother adding it and why do you have that choice in the new transaction menu?

Grant,

You’re correct that a capital gains dividend should not affect ACB. This transaction type is there for completeness (so that all capital gains can be compiled in one place), but it’s not necessary to track it on AdjustedCostBase.ca as long as your T slips are accurate and you include them when completing your tax return.

Thanks, that’s very helpful. So, from the point of items that appear on the CDS Innovation spreadsheet that will change the ACB, one only needs to record return of capital and total non cash distributions (recorded as reinvested capital gains). Would that be correct?

Grant,

That’s almost correct. There are some cases where a non-cash distribution is not coupled with a capital gain (and some cases where it is only partially coupled). In those cases you would use a reinvested distribution transaction.

OK am I understanding correctly? There are basically 5 scenarios when looking at the CDS sheets and phantom distributions:

– a non-cash distribution with blank capital gain box

– a non-cash distribution equal to capital gain box

– a non-cash distribution with a greater amount capital gain box

– a non-cash distribution with a lesser amount capital gain box

– a non-cash distribution with an percentage (e.g. BMO ETFs) in the capital gain box

Sean,

I believe that a non-cash distribution could be allocated in any way among the various categories (capital gains, return of capital, etc.). It is typically coupled with a capital gain of a equal amount, but the capital gain could be less than the non-cash distribution amount with the difference being allocated to other categories. I don’t think that the capital gain could be greater than the non-cash distribution amount, unless there’s an additional cash distribution amount combined into the same entry (typically the non-cash distribution is a separate entry at the end of the year, distinct from a cash component). The entries can be completed either with a dollar amount or a percentage of the total distribution.

I am considering signing up for the paid version of this website but I am unclear if adjustedcostbase.ca automatically handles phantom distributions. Above their are instructions for using the CDSInnovations website for getting the data and entering a transaction into adjustedcostbase.ca. If I have entered all of my transactions into this website then why aren’t the phantom distributions calculated automatically? Can’t you just automatically download all of this info from CDS and apply it to my holdings, which you already know?

Wayne,

The streamlined import feature for importing phantom distributions and return of capital transactions for ETF’s and other funds is described here:

https://www.adjustedcostbase.ca/blog/streamlined-import-of-return-of-capital-and-phantom-distributions-and-for-exchange-traded-funds-etfs-publicly-traded-mutual-funds-and-trusts/

With this feature you do not need to go through the process described above for phantom distributions (in addition to return of capital and capital gains distributions). You’ll still need to initiate the import process for each ETF each year, but the process is much less tedious and error-prone compared to the manual alternative.

Pingback: Easier than ACB – Canadian Portfolio Manager Blog

Can all funds be found on the CDS website? I have searched multiple times for RBF448 and just can’t seem to find it. I’m trying to double check whether they made any phantom distributions.

Also, on the RBC website they list for example, that 0.17 of the total 0.51 distributed was RoC. When I use that number to calculate RoC I get $1666.40 while the T3 says $1699.60 . Is there an obvious reason for this discrepancy?

Heather,

Only data for publicly traded funds (ETF’s, REITs, and other exchange traded trusts) is available. Non-publicly traded mutual funds (such as the one you mentioned) are not available.

A possible explanation of the discrepancy you’re seeing is that the number of shares owned throughout the year changed. If that’s the case then multiplying the total distribution by the number of shares owned at the end of the year will not be accurate.

Thanks very much for the guide – looks like many BlackRock ETFs just did this (phantom distributions, for example XUU (https://www.blackrock.com/ca/investors/en/products/272104/#distributionsDialog) for the 2021 year-end distribution (mix of both cash & reinvested phantom distributions).

Just to confirm, is my understanding accurate (that the case above for XUU is the scenario being described by this post and that I should be accounting for these reinvested distributions into the ACB calculation)? Really appreciate it and happy new year!

Henry,

Yes, the “Reinvested” amount listed for the Dec. 30, 2021 distribution for XUU is a phantom distribution and your ACB would increase by this amount. Note that the full tax breakdown for 2021 hasn’t been made available yet, so we can’t say whether this amount corresponds to a capital gain or some other type of distribution.

If the Phantom amount represents real money earned by the ETF from Capital Gains and the ETF decides to Reinvest instead of paying out to the unit holders or issuing new units then what confuses me is how the money is reinvested? Where does it go? I have the nagging feeling that the money is being taken away by the portfolio managers. Bigger bonus or something. New units are not created so where is this cash being invested? We all seem to accept the term invested in the ETF but what does this really mean? The ETF should represent the total number of units + cash. As no units are created where is the money going. I want to follow the money. Any insights?

Alex,

Phantom distributions typically arise from when an ETF sells some of its holdings and doesn’t distribute the capital gains to unitholders. A common scenario is when an ETF rebalances its holdings or shifts around its holdings (for example, if the constituents of an index being tracked changes). If the holdings have risen in value then the unitholders will be taxed based on the resulting capital gain. It’s often not desirable for the ETF to distribute the gain in cash in these scenarios, especially if the holdings have risen by a large amount, since it could result in an unusually large distribution. Often in these scenarios the proceeds are used to purchase other holdings. It’s possible the proceeds could be used for other purposes, such as paying the fund’s expenses, funding redemptions or increasing the fund’s cash balance, however.

You are not getting ripped off with phantom distributions. Think about when Tesla was added to the S&P500. Tesla was a pretty big stock to be added to the index. Let’s say you are a $100B index fund and Tesla is being added with a 2% weight in the index. The PM has to buy $2B on Tesla, but to do so he has to sell the other 499 stocks, plus the stock that is being dropped. So he has to sell a bunch of Apple because it is the largest stock – Apple is about 7% of the index so he has to sell 7%x$2B or $140M of Apple. Apple has been up over the last several years so when he sells Apple the ETF has a capital gain. But the proceeds of the sale are not distributed to unit holders, they are used to buy Tesla shares. You aren’t getting screwed by that.

This would be even worse with actively managed ETFs that have lots of transactions, not just additions, deletions and rebalancings.

I own the Harvest Clean Energy ETF Class A units (HCLN.TO) in both, a tax free account, and a taxable account.

A ROC Notional Distribution was received and a T3 was issued which caused a 2021 tax liability in my open account.

I did not receive the distributionin in cash and the number of shares remained the same for both accounts

My question is how and when does this distribution benefits the owner for the two accounts???

Do phantom distributions apply to US ETFs or only CAD ETFs? If they do apply to US ETFs, where would one find out the distribution details necessary to make the ACB adjustments? Thx.

Kudos,

Distributions from US-domiciled stocks and funds are generally taxable as foreign income for Canadians and therefore the distributions should not impact your ACB. This is the case even if the distribution is considered to be the equivalent of return of capital or capital gains in the US. The following article explains this well:

http://www.moneysense.ca/etfs/adjusted-cost-base-with-us-listed-etfs/

Besides the T3 slips, do I need to provide my accountant with any other information relating to ACB? I have not sold any ETFs and I am using the premium service to import the tax information. Would I only need to provide ACB information when I sell?

Should I export ACB calculations to a spreadsheet and provide these spreadsheets to the accountant?

Please advise on what information I should be supplying from this site to the accountant to ensure they report everything correctly as the prepare my taxes. To be clear, I have not sold any EFT. I just want make sure phantom distributions are being recored correctly.

Cameron,

Your T-slips combined with a capital gains report should be sufficient for your accountant. The latter can be generated as described here:

https://www.adjustedcostbase.ca/blog/annual-capital-gains-pdf-reports/

Hi, for phantom distributions that included an income tax paid component (case in point, BMO US Banks ETF ZBK for the year 2022), should the income tax paid component be included in the Adjusted Cost Base calculation or on tax filing anyhow? Even though there was no cash paid out, I assume this should at least be part of the tax filing given that it was a phantom tax withholding – simply want to reconfirm. Thanks!

Henry,

There is no further impact on your ACB beyond the increase in ACB for the reinvested amount. Any income allocation associated with the phantom distribution will be included in your T3 slip (and should be reported accurately).

Thank you for the response. Another question please if you don’t mind, for phantom distributions that are not 100% cap gains but partially ROC (I’m referring to TD Global Technology Leaders ETF TEC), will I need to recapture the ROC as a buy transaction? In this case, 99.8218% of the phantom distr is cap gains but 0.17819% is ROC. I have recorded the reinvested cap gains and ROC in ACB, which matches the T3 figures. However, based on the post above, it seems like I will now need to add another buy transaction following the ROC to offset the ACB reduction?

Thanks and hope the description was clear!

Henry,

A “Reinvested Capital Gains Distribution” transaction should only be used for the portion of a phantom distribution that is allocated as capital gains.

The remaining portion should be inputted using a “Reinvested Dividend” or “Buy” transaction. In addition, any portion that is allocated as return of capital should be accounted for with a “Return of Capital” transaction.

Thank you – the first part (reinvested cap gains distr) is clear. What I still want to reconfirm is whether the remaining portion (in this case, 0.17819% of the phantom distribution – which is allocated as return of capital) should be recaptured using a Buy transaction following the return of capital to offset the change in ACB (for context, this change is showing on the T3 in $ amount).

Essentially – am I correct to infer that a phantom distribution that is allocated as return of capital will make no difference to the ACB (since it is reinvested into the ETF)?

Thank you so much!

Henry,

Yes, a non-cash distribution component of return of capital should be represented as 2 transactions: a) a “Buy” or “Reinvested Dividend” transaction for the amount and b) a “Return of Capital” transaction for the same amount. However, these will offset each other such that there is no net change in ACB from the 2 transactions.

i held 372 units of Cominar reit in my TFSA at approx $11.25 and an offer was made to take it private at $11.75, i decided that i would move this to my margin account to create room for 2023 and just pay the tax on the cap gain, it was moved at a “deregistration cost ” of $ 11.72 and held in my margin for 3 months so i made a cap gain of $0.03 per unit so less than $12 cap gain, i just got a tax slip from TD for a cap gain of $2065 + a return of capital for $603, i appealed to CRA and they tell me nothing they can do talk to TD, i call TD and they tell me nothing they can do as it is online investing so hire a tax expert, the rep did say however y it was affected by a “notional distribution” and money was reinvested for me in extra units but this can’t be as it no longer exists, i looked online for “notional distributions” and they are for ETF’s and mutual funds this was a stock, i feel this is unfair that i have to hire a tax expert when i made less than $12 profit but don’t want to pay tax on $2650 i did not receive

Rick,

If you are referring to the T5008 slip issued by your brokerage, there is no need to appeal anything. There is no expectation for the cost value reported by a brokerage on a T5008 slip to be accurate.

T5008 slips can be useful to make sure you’ve accounted for all dispositions, but there are many reasons they can be inaccurate (and there is no obligation for your brokerage to correct any errors):

https://www.adjustedcostbase.ca/blog/can-you-rely-on-your-brokerage-for-calculating-adjusted-cost-base-and-capital-gains/

I would suggest reporting the gain based on your own calculations. You should not rely on automatically importing T5008 into your tax software (or if you do, carefully review the results and make the appropriate changes).

Hi, for phantom distributions that are attributable to eligible dividends, foreign non-business income, and foreign non-business income tax paid (case in point, Evolve Innovation Index ETF EDGE for the year 2023), how should this transaction be recorded? In this case, I see from the CDS form that there was a phantom distribution of 0.03132 per unit (0.00802 attributable to dividends, 0.03884 to foreign non-business income, and -0.01554 to tax paid). Thanks!

Henry,

The phantom distribution for Evolve Innovation Index Fund (EDGE) on December 29, 2023 can be inputted into AdjustedCostBase.ca as a “Reinvested Dividend” transaction with a total amount equal to $0.03132 multiplied by the number of units owned.

Hi, TDB2915 is a money market USD fund. I don’t understand how such a fund can have a phantom distribution because it has a constant NAV. It would create a capital loss because the fund price cannot change. The shareholder has to sell his shares and claim a capital loss. Does CRA allow a unitholder to declare a capital loss on a security with a constant NAV? It doesn’t make sense to me, but then again this is my first experience with a phantom distribution (TD gives it the glossier name of Special Distribution or Notional Distribution).

Tom,

Please see the following article from the Globe and Mail:

https://www.theglobeandmail.com/investing/education/article-cracking-the-mystery-of-the-money-losing-money-market-fund/

It describes the reason behind the non-cash capital gains distribution as “capital gains on foreign exchange resulting from the conversion of U.S. dollars to Canadian dollars for tax reporting purposes”.

Hi AdjustedCostBase.ca,

I own 1,000 units of the USD denominated Global X – UBIL.U. In 2024, the ETF had monthly distributions and issued a Non-Cash Distribution of $0.70807 USD per unit at year-end. Although I have a US currency Non-Registered account, my brokerage firm (one of the big Six Banks) issued my T3 using the average annual exchange rate of 1.3689 to convert the 2024 transactions to CAD.

• The Non-Cash Distribution included in box 21 of my T3 slip was ($0.70807 USD x 1.3689) x 1,000 = $969.28 CAD.

My ACB will increase by this same amount, therefore, my future gain or loss will also vary accordingly.

My question is with respect to the Exchange rate used. The Bank of Canada rate for December 31, 2024 was 1.4389. Is it best to use the values reported on my T3 to avoid creating a discrepancy between what is reported to the CRA and what I would have calculated using the BofC rate? I know the CRA allows for the use of the annual exchange rate if multiple transactions occurred over the course of the year…

• Based on the Capital Gain value of $0.72699 USD reported in Box A for the record date of December 31, 2024, the difference between this and the Non-Cash Distribution of $0.70807 would amount to a Capital Gains Dividend of $0.01892 USD? (no impact on the ACB calculation, but can be input to track overall Capital Gains, correct?)

Thank you for sharing your wealth of knowledge with the rest of us.

These Phantom Distributions rip you off if they are in a TFSA

They increase your Securities Cost Base which reduces your Capital Gain which in a TFSA is not Taxed so you lose

I cannot find iShares Core MSCI Emerging Markets ETF (IEMG) to import. I assume because IEMG trades on U.S. stock exchange?

Sean,

Yes that’s correct – the data is not available for IEMG because data is only available for Canadian-domiciled funds.

Distributions from US-domiciled funds are generally considered to be foreign income, which does not impact your ACB (even if the distributions are classified as return of capital according to US tax laws):

https://www.moneysense.ca/columns/adjusted-cost-base-with-us-listed-etfs/

Note that it may be technically possible to claim that income from a US-domiciled fund is return of capital (or capital gains), however, from a practical standpoint it is very difficult to back this up with evidence. If a distribution is deemed to be return of capital under US tax law, it does not necessarily imply the same consideration under Canadian tax law. It’s unlikely that US funds will provide the necessary documentation to support this, so it is difficult to make this determination.

William,

Phantom/non-cash distributions typically arise from a fund selling it’s underlying holdings at a gain. In a non-registered account this would be taxable even when the gain isn’t distributed to unit holders. In a TFSA account you avoid the tax liability from this gain.

In a non-registered account you should increase your ACB in order to avoid double taxation from a non-cash distribution. But increasing your ACB does not wipe out the gain entirely – you’re still on the hook for the capital gains with a non-registered account.